India: Imported met coke prices climb on tight coal supply; domestic market finds strong floor

...

- Imported met coke stays firm on tight supply and strong Chinese buying

- Domestic met coke remains stable amid adequate availability and supportive import costs

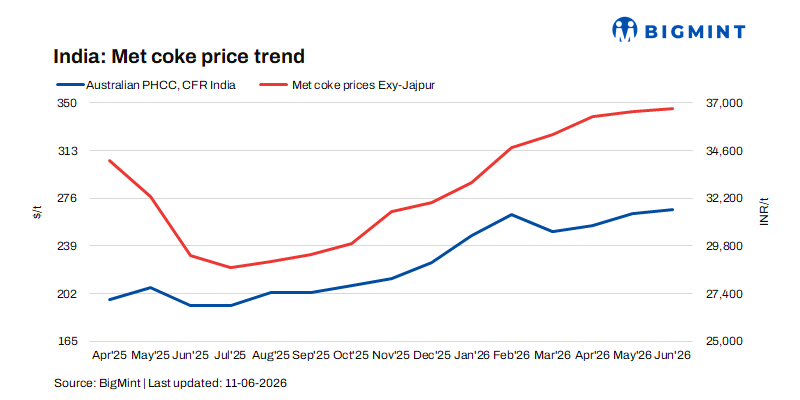

India's imported met coke market witnessed a notable upswing during the week ended 11 June 2026, supported by strengthening international coke prices and rising raw material costs. BigMint's assessment for Indonesian-origin BF-grade coke (65/63 CSR) increased by $2/t week-on-week to around $315/t CFR India.

The rally was primarily driven by firmer FOB offers from Indonesian suppliers, aggressive buying interest from Chinese consumers following mine-related supply disruptions, and improving sentiment across the global coking coal and coke value chain.

Market participants indicated that Indonesian suppliers have become increasingly reluctant to release cargoes amid expectations of further price gains. FOB offers, which were previously heard at $288-290/t, are now expected to move closer to $300/t as producers attempt to recover higher coking coal costs and account for tightening supply conditions stemming from the recent mine accident in China and delays in Australian coal shipments.

Chinese demand and coal supply disruptions fuel global sentiment

A key driver behind the recent market strength has been China's heightened procurement activity. Tight coking coal availability, caused by mine shutdowns and stringent safety inspections, continues to support domestic coke prices in China. The sixth round of coke price increases has already been implemented, raising prices by Yuan 55/t across major regions.

Strong steel production rates, active raw material restocking, and low coke inventories have further tightened market fundamentals, with expectations building for a potential seventh round of coke price hikes. This has provided significant cost support to coke producers globally and reinforced bullish sentiment across export markets.

Indian domestic coke market remains stable amid comfortable availability

In contrast to the volatility seen in imported markets, India's domestic BF-grade metallurgical coke market remained largely stable during the week. Adequate material availability, balanced supply-demand conditions, and comfortable inventory levels across key steelmaking regions prevented any major price escalation despite rising import parity costs.

Eastern India prices remained unchanged at INR 36,700/t ex-Jajpur, while western India witnessed a marginal increase of INR 500/t to INR 34,000/t ex-Gandhidham, supported by localized demand and replacement cost pressures. Foundry-grade coke prices also remained stable at INR 36,400/t ex-Rajkot, reflecting steady consumption from foundry units and sufficient market supply.

Market participants believe "Domestic coke prices will remain supported by elevated international prices and higher landed costs. Additionally, the weakness of the Indian rupee is increasing import costs further, discouraging aggressive overseas purchases. Rising coke prices are also expected to enhance demand for PCI coal as a blending alternative, lending additional support to PCI coal prices."

Coking coal market provides strong cost support

The coking coal market continued to strengthen during the week, providing a firm cost base for coke producers. Australian Premium Hard Coking Coal (PHCC) prices increased by $3/t w-o-w to $245/t FOB Australia. Combined with ongoing supply concerns in China and logistical challenges affecting Australian exports, the upward trend in coking coal prices is expected to keep production costs elevated and support coke prices globally.

Pig iron market signals demand caution

While steel production levels remain healthy, downstream purchasing activity in the pig iron market showed signs of moderation. Steel-grade pig iron prices in Durgapur declined by INR 200/t w-o-w to INR 37,800/t ex-works, reflecting cautious buying behaviour among steelmakers.

Recent auction results from NMDC Steel's Nagarnar plant further highlighted the softer demand environment. Of the 12,000 t of steel-grade pig iron offered on 10 June, only 3,100 t was booked at the base price of INR 36,000/t ex-works. This contrasts sharply with the previous auction on 2 June, where the entire offered quantity was sold. The lower offtake suggests buyers are adopting a wait-and-watch approach amid uncertain steel market conditions and subdued downstream demand.

Outlook

The near-term outlook for the met coke market remains cautiously bullish. Imported coke prices are expected to stay elevated, supported by rising coking coal costs, continued Chinese buying interest, supply constraints in key coal-producing regions, and higher Indonesian FOB offers. Any further increase in Chinese domestic coke prices or disruption to coking coal supply could push international coke prices higher.

However, the Indian domestic market is likely to remain relatively range-bound in the short term. Comfortable inventories, adequate domestic supply, and subdued pig iron demand may limit sharp price increases despite higher import parity levels. Nevertheless, continued anti-dumping duties, a weaker rupee, and rising replacement costs are expected to provide a strong price floor, keeping domestic coke values well supported in the coming weeks.