India: HZL raises zinc prices by INR 3,800/t, lead by INR 2,500/t

...

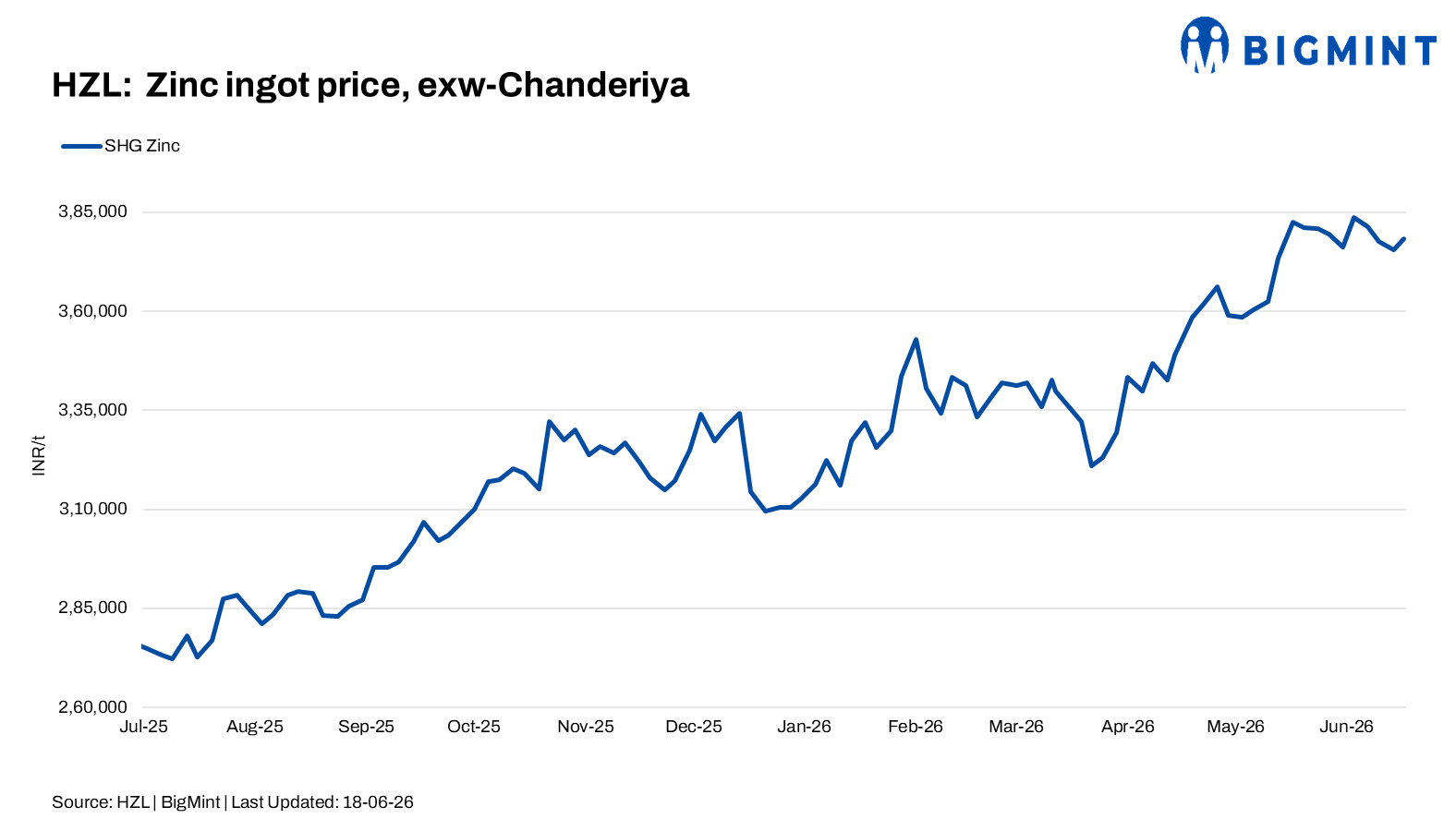

- HZL SHG zinc prices maintain premium over domestic spot market levels

- Need-based buying persists despite tighter global zinc supply outlook

Hindustan Zinc Ltd (HZL) on 18 June 2026 increased zinc ingot prices by INR 3,800/t ($44/t) and lead ingot prices by INR 2,500/t ($29/t) compared with its previous revision announced on 15 June.

Following the revision, HZL's benchmark Special High Grade (SHG) zinc ingot prices were increased to INR 378,300/t ($4,416/t), while lead ingot prices rose to INR 220,500/t ($2,577/t).

Other revised zinc grades were:

Special High Grade-Continuous Galvanising Grade (SHG-CGG): INR 379,800/t ($4,433/t)

Special High Grade Jumbo (SHG-Jumbo): INR 378,800/t ($4,422/t)

High Grade (HG): INR 377,800/t ($4,410/t)

Prime Western (PW): INR 376,300/t ($4,393/t)

On the London Metal Exchange (LME), zinc prices were trading at $3,582/t, down 0.8%, while lead prices declined by 0.78% to $1,971/t as of 3:30 PM IST. Market sentiment weakened after fresh economic data from China raised concerns over demand prospects. Retail sales contracted by 0.6% in May, marking the first decline in more than three years, while fixed-asset investment fell 4.1% during January-May, reflecting softer industrial and construction activity in the world's largest metals-consuming nation.

Despite the latest increase, HZL's SHG zinc prices remained above domestic spot market levels. According to BigMint's assessment on 18 June, zinc ingot prices stood at around INR 375,500/t ex-Delhi, placing HZL's benchmark SHG prices at a premium of approximately INR 2,800/t. Market participants indicated that procurement activity continued on a need-based basis, with buyers remaining cautious amid fluctuating international prices and uncertainty surrounding downstream demand recovery.

The broader zinc market continues to receive support from tightening supply conditions despite concerns over Chinese demand. Nexa Resources recently suspended operations at its Cajamarquilla smelter in Peru following a fire, while Glencore-owned Kazzinc has continued operating at reduced capacity after an explosion impacted its zinc and lead facilities in Kazakhstan. These disruptions have reinforced expectations of a refined zinc market deficit this year, as projected by the International Lead and Zinc Study Group (ILZSG).

Additional support has come from low exchange inventories and ongoing mine supply challenges. However, market participants are also monitoring the return of production from several producers. Sweden's Boliden is expected to resume operations at its Garpenberg mine during the second quarter, while Japan's Mitsui Mining and Smelting has projected a 3.2% increase in refined zinc output during the first half of FY2026-27. The global zinc market surplus also narrowed considerably in March, indicating improving market balance.

Overall, while weaker Chinese economic indicators may continue to weigh on sentiment in the near term, supply-side disruptions, low inventories and expectations of a refined zinc deficit are expected to provide underlying support to global zinc prices. In the domestic market, procurement activity is likely to remain measured, with buyers closely tracking international price trends and downstream demand conditions.