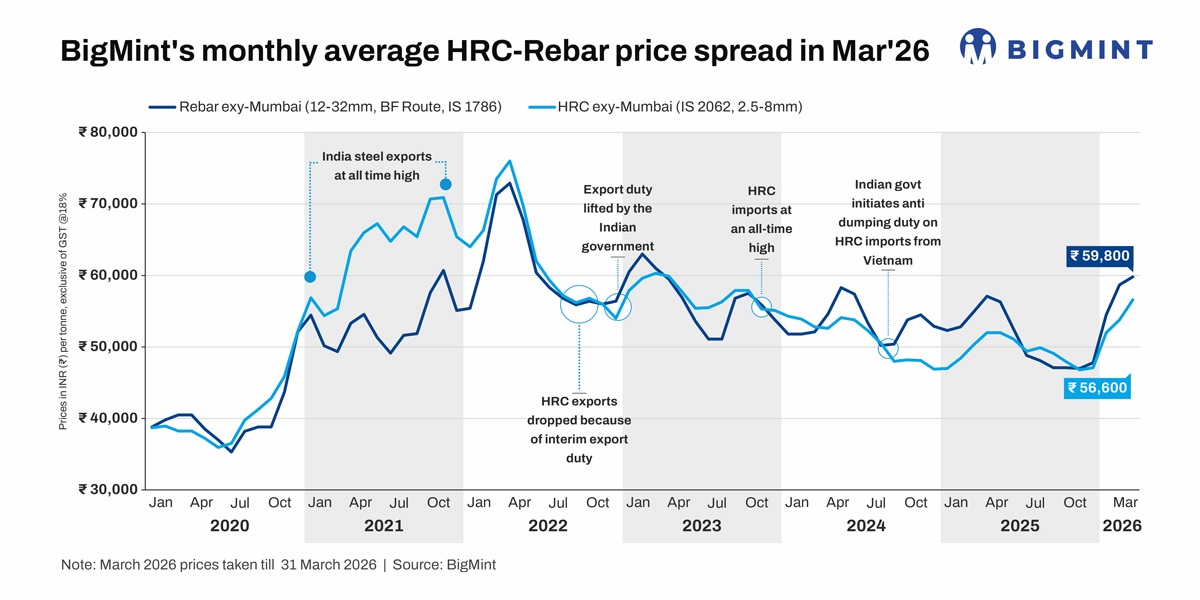

India: HRC-rebar negative spread narrows in Mar'26 as flats prices rise at a faster pace

...

- HRC prices rise by over 5% m-o-m, rebar rises 1.9% in March

- HRC-rebar negative spread decreases by INR 1,700/t in March

- Mills may hike HRC list prices, negative spread may narrow in April

Morning Brief: The reverse or negative spread between domestic hot-rolled steel coil (HRC, IS 2062, 2.5-8mm) and blast furnace-origin reinforcement bar (12-32mm, IS 1786) prices in the domestic market narrowed to - INR 3,200/t from -INR 4,900/t in February, as per BigMint assessment.

The reverse spread narrowed m-o-m in March because the rate of increase of domestic HRC prices was higher than BF rebar: while HRC prices rose by over 5% m-o-m to an average of INR 56,600/t exy-Mumbai, BF rebar prices increased by less than 2% to INR 59,800/t, as per BigMint assessment.

Rebar prices rose slowly as buyers turned cautious due to a sustained rally and the widening differential with IF rebar prices. In the HRC segment, however, prices were supported by geopolitical tensions in the Middle East and panic restocking in the market, shortage of natural gas due to the Iran crisis and impact on downstream production, as well as tight supplies in many regions which supported prices.

Mills raised HRC, CRC prices on policy support in the form of safeguard duty, sharply declining flat steel imports, and due to domestic prices remaining lower than imports.

Under normal circumstances, the spread between HRC-rebar stands at around INR 4,500-5,000/t.

Price movements in Mar'26

HRC market movements: Steel prices softened a bit due to weak trade sentiments ahead of Holi festival. However, escalating tensions in the Middle East provided a boost to prices following the surge in energy and freight costs.

After Holi, the leading mills raised HRC prices for mid-March. Trade sentiment remained bullish, underpinned by geopolitical uncertainty and supply constraints which injected volatility into global commodity markets, prompting traders and distributors to build inventories in apprehension of potential supply disruptions. This, coupled with tight availability, particularly in north India, resulted in a sharp w-o-w increase in prices.

Trade-level prices again increased towards the end of March, with HRC holding at a nearly 29-month high amid tightening supply conditions due to reduced imports and input constraints. Coated and galvanised steel prices shot up sharply amid maintenance announcements and tight supplies due to unavailability of gas. In addition, surge in exports and lower imports supported prices.

BF rebar prices edge up: In the beginning of March, trade-level BF rebar prices remained largely stable after the primary mills increased list prices for March. Steady demand and offtake from the projects segment kept prices supported, as the major mills were booked till the end of March and were operating at low stock levels.

The primary mills again raised prices after mid-March on healthy order bookings, especially healthy project segment offtake ahead of the financial year-end. In addition, limited availability of some sizes lent support to prices.

The primary steelmakers increased rebar prices further by up to INR 1,000/t ($11/t) in the week ended 27 March on rising raw material prices and input costs and falling inventories. Rebar inventories at primary mills dropped further by 8-9% in end-March as against the beginning of the month. However, buyer caution at high prices and the widening spread with IF rebar weighed on prices.

Outlook

In the event of the West Asia conflict continuing, steel prices are likely to remain supported on input shortages and spike in prices. Downstream mill maintenances in April due to fuel shortages may keep supplies tight and prices firm. The tier-1 mills are already looking to take a hike in list prices with the beginning of next week. BigMint expects the rebar-HRC negative spread to contract further in April.