India: How global energy shocks filter through steel into wholesale manufacturing inflation

...

- WPI inflation surges to 42-month high of 8.3% in Apr'26

- WPI, BigMint data show steel prices recovering from late-2025

- Strong industrial activity allows mills to pass through rising input costs

India's wholesale price inflation surged to 8.3% in April 2026, its highest level in 42 months, as rising energy and commodity costs pushed through industrial supply chains and lifted manufacturing prices across the economy. While the headline inflation spike was driven primarily by fuel and crude oil, the data suggest that steel became one of the clearest channels through which those cost pressures entered the manufacturing sector.

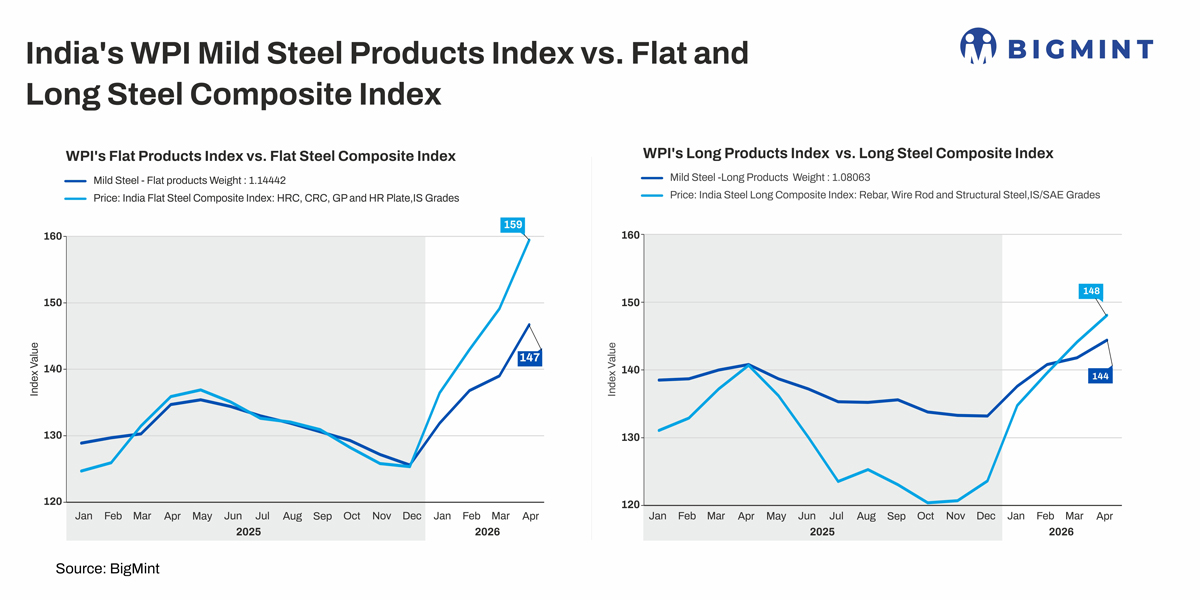

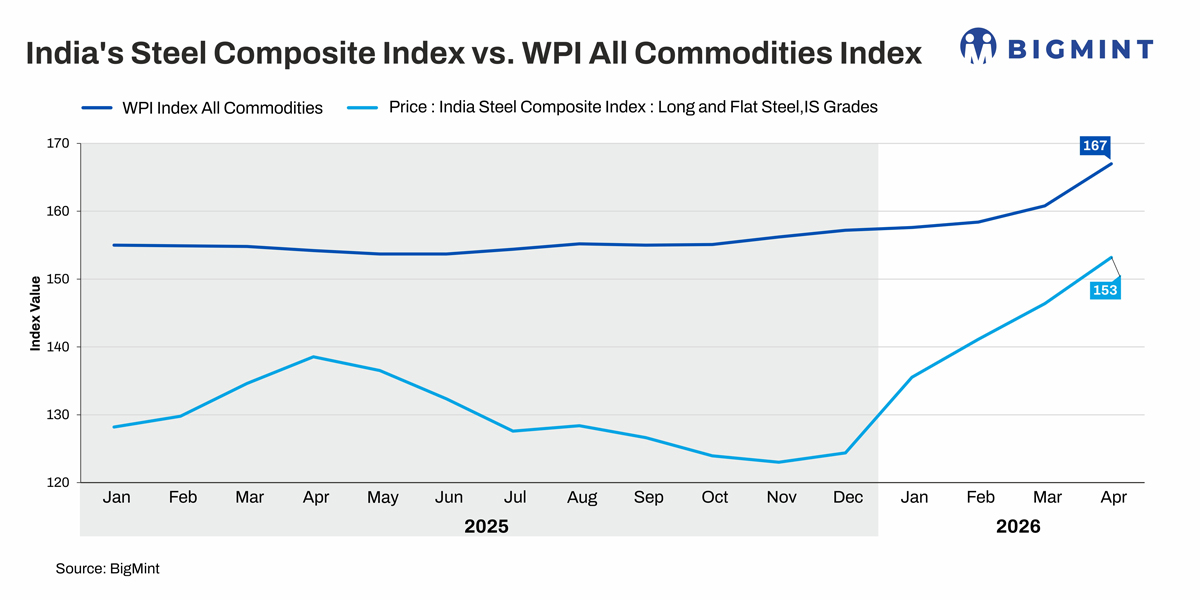

A comparison of Government Wholesale Price Index (WPI) data and BigMint's steel index reveals a consistent pattern. Both datasets show steel prices remaining under pressure for much of 2025 before recovering sharply from late-2025 onwards. Both also show flat steel products outperforming long products during the recovery phase.

The significance of that recovery extends beyond steel itself. As one of the largest components within India's manufacturing basket, steel sits at the intersection of raw materials, industrial production, infrastructure, and end-use manufacturing. Within the WPI framework, the Manufacture of Basic Metals category carries a weight of 9.65%, while mild steel long and flat products account for 1.08% and 1.14%, respectively. The latest data suggest that as energy costs accelerated, steel prices strengthened, basic metals inflation rose, and manufacturing inflation followed, amplifying the impact of rising input costs across the broader economy.

Steel subdued through most of 2025

WPI data show that steel prices remained weak for much of 2025 despite relatively stable economic activity. The WPI index for mild steel long products declined from 138.5 in January 2025 to 133.2 by December, while flat products fell from 128.9 to 125.6 over the same period. The Manufacture of Basic Metals index was largely unchanged, edging up only marginally from 137.2 to 137.6.

The same trend is visible in BigMint's market data. The composite steel index declined from 136.9 in March 2025 to 123.1 by November, reflecting weak pricing power and subdued market sentiment across the sector.

As a result, steel contributed little inflationary pressure to the manufacturing basket through most of the year. Even as broader economic activity remained resilient, steel prices and basic metals remained subdued amid elevated imports, particularly low-priced flat steel imports, which weighed on domestic pricing and limited mills' ability to pass through costs. Consequently, steel's contribution to wholesale inflation remained muted through much of 2025.

Industrial activity strengthens as costs rise

BigMint's weekly steel indices stabilised in November before moving higher through December and into early 2026. Government data subsequently reflected a similar trend, with the Manufacture of Basic Metals index rising from 137.6 in December to 141.6 in January before continuing higher through April. The recovery coincided with easing import pressure, improving market sentiment, and expectations surrounding trade protection measures, culminating in the implementation of a safeguard duty in April that helped strengthen domestic pricing conditions.

BigMint's higher-frequency, market-based steel indices captured the recovery in steel prices several weeks before the same trend became visible in the official WPI steel and basic metals series.

The recovery coincided with an improving industrial backdrop. Manufacturing PMI remained in expansion territory at 54.7 in April 2026, indicating continued growth in factory activity. Industrial production also strengthened, with the Index of Industrial Production (IIP) rising to 173 in March from 159 in January. Infrastructure-linked indicators remained supportive, with cement production reaching 49 million tonnes in March.

At the same time, broader economic indicators suggested that activity remained resilient despite rising costs. GST collections reached a record INR 2.43 trillion in April, while the Reserve Bank of India had reduced policy rates from 6.5% in January 2025 to 5.25% by February 2026, helping maintain supportive financial conditions for industrial activity.

Together, these indicators suggest that steel prices were recovering in an environment characterised by both strengthening industrial activity and mounting cost pressures.

Flat steel provides clearest signal

According to WPI data, the flat steel index rose from 125.6 in December 2025 to 146.7 by April 2026, a gain of 16.8%, compared with an increase in long products from 133.2 to 144.4, a gain of 8.4%. BigMint's indices show an even stronger recovery, with flat products rising from 128.7 to 160.4 over the same period, a gain of 24.7%, compared with an increase in long products from 125.4 to 149.6, a gain of 19.2%.

The divergence is significant because it provides clues about the nature of the recovery. Had construction activity been the sole driver, long products would likely have outperformed flats. Instead, the stronger performance of flat steel points towards improving industrial and manufacturing activity, where flat products are heavily consumed by automobiles, engineering goods, machinery, consumer durables, fabrication, and other downstream sectors.

The consistency of this trend across both datasets strengthens the interpretation that the recovery was broader than a purely construction-led rebound.

This interpretation is consistent with the broader macro data. Manufacturing PMI remained comfortably above the expansion threshold, industrial output strengthened, and industrial power demand increased during the period. The stronger performance of flats, therefore, suggests that the recovery was not confined to construction and infrastructure alone but was also supported by improving activity across manufacturing supply chains.

At the same time, flat steel producers tend to be more exposed to energy-intensive downstream processing activities such as cold rolling and coating. As fuel, electricity, freight, and other industrial costs increased, flat steel prices became sensitive to those pressures.

Energy costs filter through steel into manufacturing inflation

The relationship between steel and wholesale inflation became most visible in March and April. WPI inflation accelerated from 2.13% in February to 3.88% in March and 8.3% in April. The surge was driven primarily by energy-related inflation. Fuel and power inflation jumped to 24.71% in April, while crude petroleum and natural gas inflation exceeded 67%.

Mineral oil prices increased 29.37% m-o-m in April alone, while petrol and diesel WPI indices rose to 193.7 and 200.3 respectively. The scale of the energy shock was therefore not confined to crude oil but extended across multiple industrial fuel and transport inputs.

Higher fuel, freight, electricity, and raw material costs increased production expenses across industrial supply chains. Steel, given its exposure to both commodity inputs and industrial demand, was particularly sensitive to these pressures.

Flat steel producers were especially exposed through energy-intensive downstream processes such as cold rolling and coating, helping explain the stronger recovery in flat steel prices relative to long products.

As steel prices strengthened, the Manufacture of Basic Metals index rose from 137.6 in December to 149.9 by April. Basic metals subsequently became one of the largest contributors to manufacturing inflation, while the Manufactured Products basket recorded inflation of 4.62% in April.

The data therefore suggest that the energy shock did not move directly into headline wholesale inflation. Instead, it filtered through upstream industrial sectors such as steel and basic metals before becoming visible across the wider manufacturing basket.

Outlook

The recent inflation cycle highlights the close relationship between energy costs, steel pricing, and manufacturing inflation. While the sharp rise in WPI during March and April was primarily driven by fuel and commodity costs, the sustainability of steel prices from here will depend increasingly on underlying demand conditions.

Current indicators remain broadly supportive. Manufacturing PMI continues to signal expansion, industrial production remains firm, infrastructure activity remains healthy, and steel consumption was still 8% higher y-o-y in April despite moderating from the fiscal year-end surge recorded in March.

At the same time, wholesale inflation remains highly sensitive to developments in global energy and commodity markets. Any sustained increase in fuel, freight, or raw material costs would continue supporting basic metals inflation and steel pricing.