India: Govt projects net-zero policies could cut steel industry CO2 emissions intensity by over 70% by 2050

...

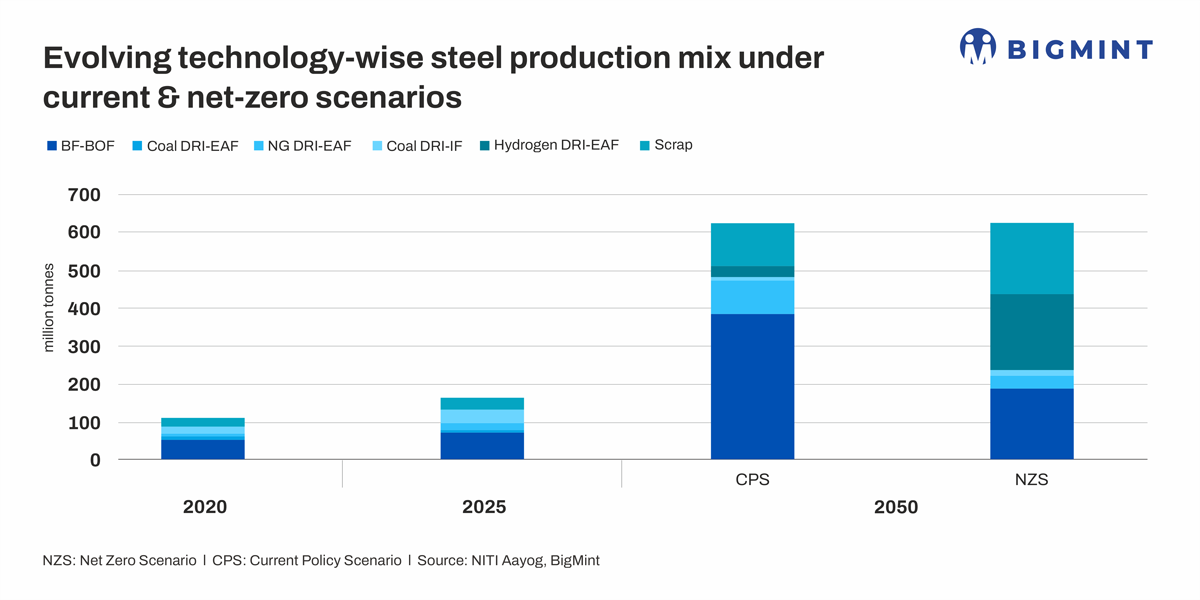

- NITI Aayog projects steel output to reach 624 mnt by 2050

- Share of BF-BOF under net-zero scenario to reduce sharply by 2050

- 30% of crude steel production to be based on scrap by mid-century

Morning Brief: The Indian steel industry's carbon emissions intensity is expected to drop by 44% by 2050 from current levels under a business-as-usual scenario, while emissions reductions are expected to be much sharper, around 74% compared with current levels, under a net-zero scenario (NZS), according to NITI Aayog, the government's premier think-tank.

While C02 intensity may reach around 1.3-1.4 tCO2/t of steel by 2050 under the business-as-usual scenario, emissions may drop to around 0.6-0.7 tCO2/t under the net-zero scenario. Current CO2 intensity is around 2.5 tCO2/t, as per Ministry of Steel.

NITI Aayog's steel sector modelling focuses on two scenarios - the 'current policy scenario' (CPS) or business-as-usual and the net-zero scenario. The two scenarios are based on a set of assumptions:

- BF-BOF dominates in CPS till 2050 but in the NZS BF-BOF dominates till 2040, with no new additions after 2060

- Coal-DRI-IF is phased out after 2030 under both scenarios

- Natural gas (NG)-DRI to be transition technology under both scenarios but no new capacity additions happen after 2040 in the NZS

- H2-DR-EAF commercialisation starts from 2035 and attains scale after 2045 under CPS but under NPS this technology starts in 2030 with significant scale emerging in the 2040s

Energy use & fuel mix

NITI Aayog projects crude steel production to reach 624 million tonnes (mnt) by 2050 using a 'saturation-growth model'. As India industrialises, steel demand is expected to increase rapidly by mid-century, after which the growth is expected to slow down. This mirrors the pattern seen in other industrialised nations. Per capita consumption is expected to reach around 450/kg after which it is expected to plateau.

Notably, the steel sector's specific energy consumption (SEC) is expected to drop by 24% under the NZS, with the domestic mills reaching the level of global best practices as opposed to just 12% under CPS. Indian BF-BOF mills' SEC currently averages around 26-27 gigajoules per tonne (Gt) versus the global best of 20-22 Gt.

Also, another ambitious assumption made by NITI Aayog is the decline in coal's share in captive generation to just 20% by 2050 from 93% in 2023-24 due to the rapid shift to renewables and nuclear power, tightening of taxonomies under CCTS, and development of storage capacities. Reliance on a clean and stable grid is projected to increase vis--vis captive power.

Importantly, despite the positive policy framework created to boost domestic scrap generation, under the current policy scenario scrap consumption in steel industry will remain at the same level of 20% in 2050 as in 2024. In the NZS, however, scrap use in steelmaking is projected to increase to 30% by mid-century through strong EPR policies, minimum recycled content norms and a formalised value chain.

Technology transformation

Therefore, ambitious targets and policies are required to drive net-zero goals broadly in alignment with the IEAs NZS 2050. While reduction in SEC and steel sector emissions will continue, albeit at a very slow pace, under the CPS, net-zero policies are needed to drive faster and deeper decarbonisation.

Importantly, the share of BF-BOF under net-zero by 2050 should be well below 200 mnt, according to NITI Aayog model, whereas in the CPS that share is close to 400 mnt. This is a key challenge for India.

Another key challenge is to quicken the pace of H2-based DRI production and steel production via EAF technology which has the potential to replace a large share of BF-BOF steel production in India. While the shift from NG-based ironmaking to H2 is quite marked in the NZS, the share of green DRI-based steel is quite low in CPS (see figure above).

Additionally, if 180-200 mnt of crude steel output in 2050 is projected to be based on scrap under the NZS then fast-tracking of policy measures and strict implementation are required to raise the share of domestic scrap generation.

According to NITI Aayog, scaling up EAF technology requires a dedicated and robust framework for scrap policy that goes beyond vehicle scrappage policy and includes segregation networks, formal scrap collection targets, digital information of the scraps used, and a certification mechanism for quality assurance.