India: ERW patra pipe prices show mixed trends w-o-w across key regions

...

- Monsoon-led slowdown likely to pressure prices in near term

- Supply constraints provide downside support to Mandi Gobindgarh prices

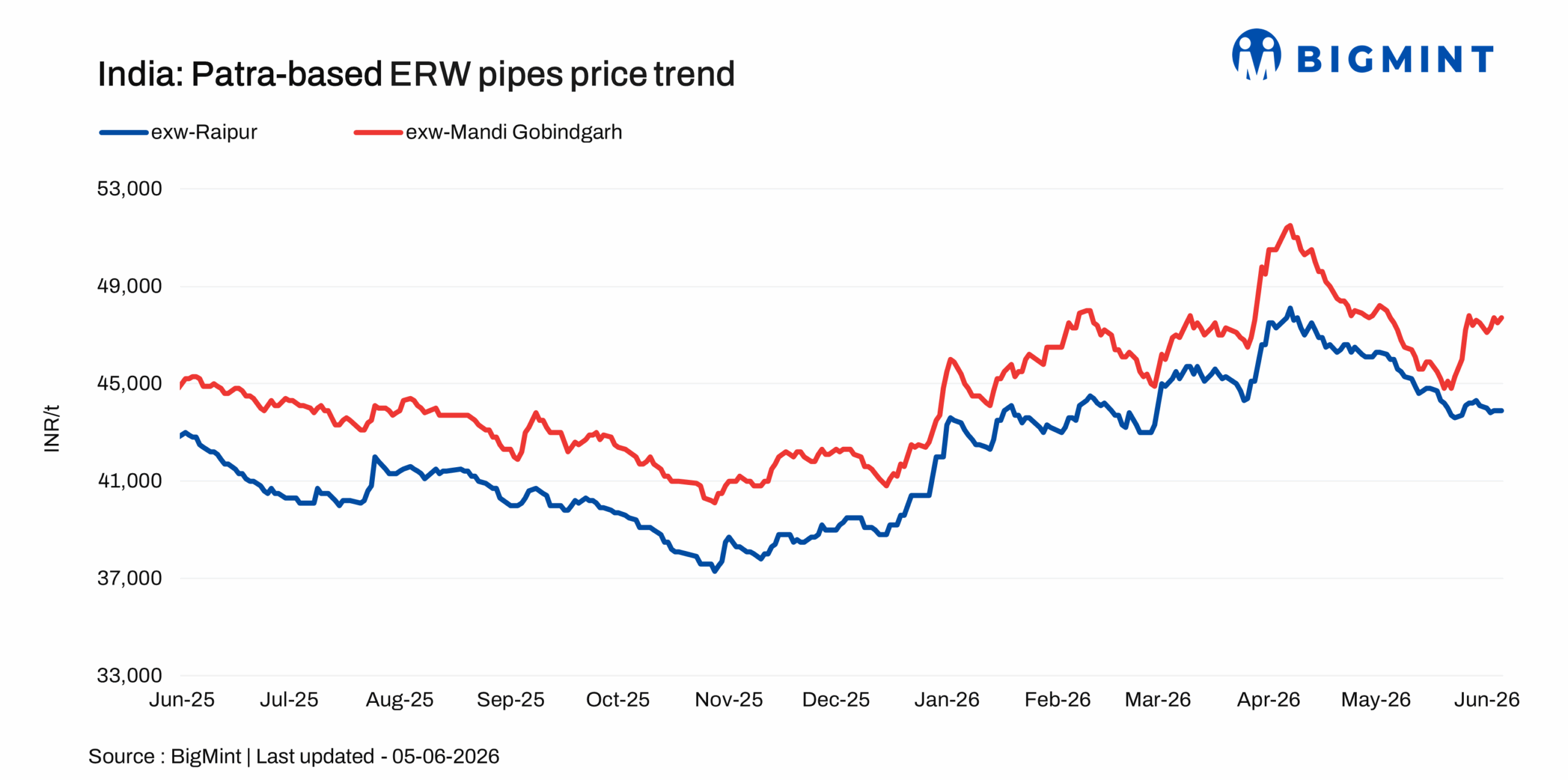

ERW patra pipe prices (41-60 mm OD) showed mixed trends across key regions in the week ended 5 June 2026. While prices in Raipur declined w-o-w, those in Mandi Gobindgarh moved higher.

A similar trend was observed on a d-o-d basis. In Raipur, prices remained stable d-o-d at INR 43,900/t ex-works (exw) on 5 June. In contrast, prices in Mandi Gobindgarh edged up by INR 100/t d-o-d to INR 47,700/t exw on 5 June from INR 47,600/t a day earlier. Listed prices are ex-works and exclude 18% GST.

Weekly price trends

Raipur: ERW patra pipe prices in Raipur declined by INR 400/t w-o-w to INR 43,900/t exw on 5 June, down from INR 44,300/t on 29 May 2026. Demand conditions continued to remain subdued throughout the week, with trading activity largely restricted to need-based purchases as buyers adopted a cautious approach amid uncertain market direction.

A Raipur-based source indicated that, "the onset of the monsoon season is expected to further dampen consumption, as construction and infrastructure activities typically slow during this period. Consequently, overall market activity is likely to remain subdued, limiting trading volumes and exerting continued downward pressure on prices."

Mandi Gobindgarh: ERW patra pipe prices in Mandi Gobindgarh rose marginally by INR 100/t w-o-w to INR 47,700/t exw on 5 June, up from INR 47,600/t a week earlier. However, prices remained volatile throughout the week, before stabilising towards the end of the period.

A Mandi Gobindgarh-based source stated that, "Market conditions still remain sluggish, with demand yet to show sustained signs of recovery. Meanwhile, tight labour availability and limited scrap supply continue to constrain production levels, resulting in tight supplies of billet and HR strip and causing delays in order deliveries across the value chain. In addition, higher production costs and reduced raw material availability have increased the conversion parity from billet to HR strip by around INR 1,000/t to INR 2,500-3,000/t from INR 1,500-2,000/t earlier. As a result, supply-side constraints continue to provide downside support to prices despite sluggish demand conditions."

Overall, market participants hold mixed views on the near-term price direction. While some expect prices to remain firm in the coming days amid ongoing supply-side constraints, others anticipate limited upside, with prices likely to remain largely stable amid weak demand conditions.

Raw material prices

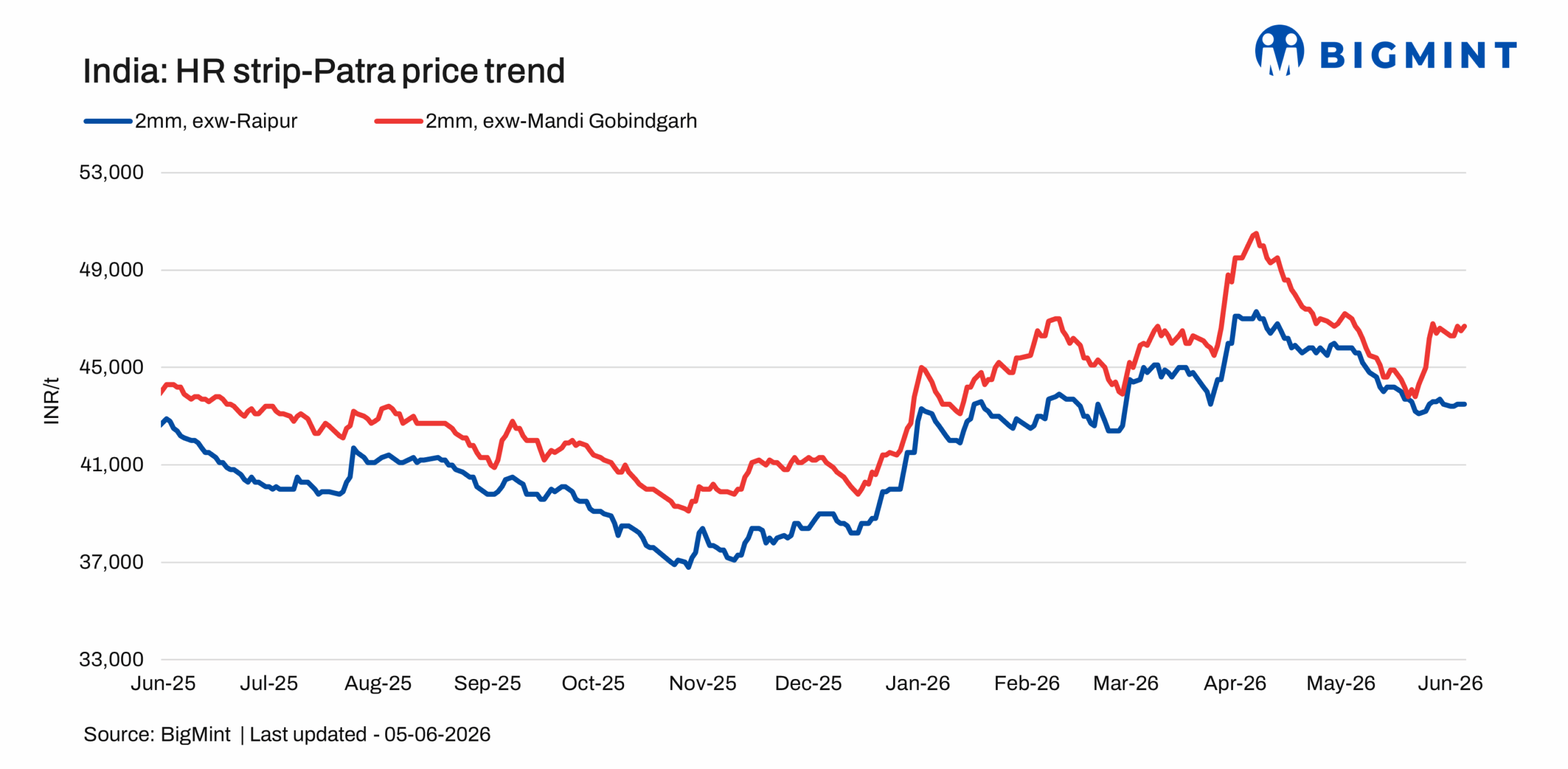

HR strip (patra): HR strip (patra) prices in Raipur declined by INR 200/t w-o-w to INR 43,500/t exw on 5 June from INR 43,700/t exw on 29 May. Meanwhile, patra prices in Mandi Gobindgarh inched up by INR 100/t w-o-w to INR 46,700/t exw from INR 46,600/t a week earlier.

Billet: Billet prices in Raipur dropped by INR 500/t w-o-w to INR 38,800/t exw on 5 June from INR 39,300/t a week earlier. Meanwhile, billet prices in Mandi Gobindgarh stood at around INR 43,200/t DAP on 5 June, down by INR 300/t w-o-w from INR 43,500/t on 29 May.

Although HR strip (patra) and ERW pipe prices edged higher in Mandi Gobindgarh, billet prices declined w-o-w as weak downstream demand and subdued buying interest continued to weigh on billet market sentiment.

Outlook

ERW patra pipe prices are likely to remain under pressure in the coming days, as weak demand and subdued buying activity continue to weigh on the market prices. The onset of the monsoon season may further dampen market activity in the coming weeks and keep demand muted across key regions. However, ongoing supply-side constraints in Mandi Gobindgarh, including tight labour availability and limited scrap supply, are likely to provide some downside support and limit the extent of any price decline. Overall, market direction will largely depend on the pace of demand recovery and movements in raw material prices.