India: Economy faces steep inflationary pressures as consumption, industrial activity diverge

...

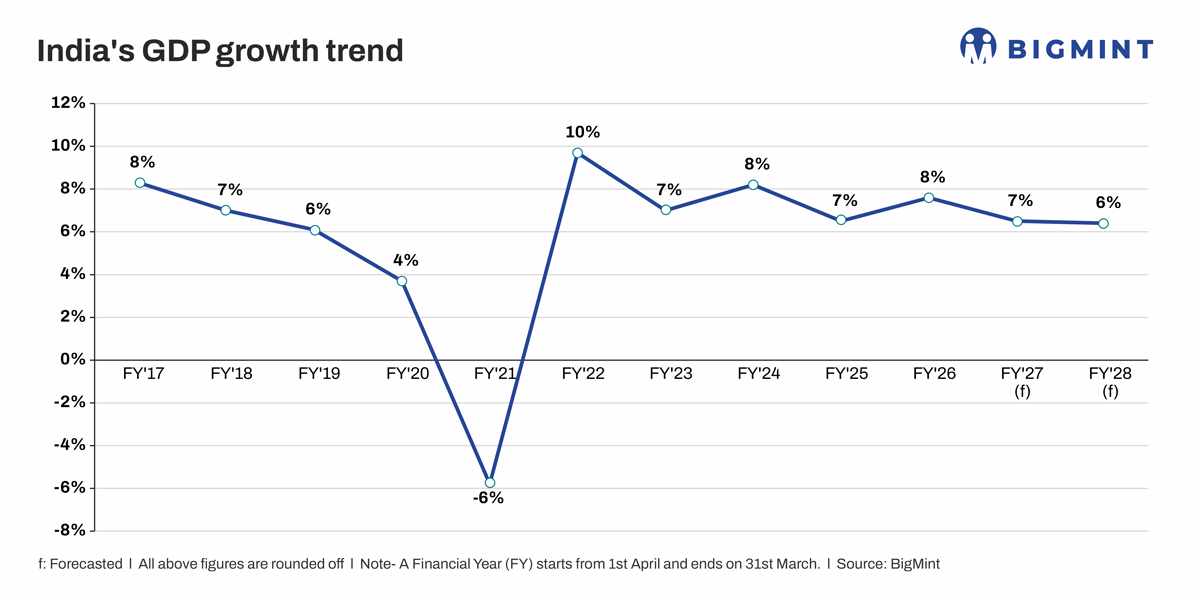

- OECD expects India's GDP growth to slow to 6.3% in FY27 from 7.6% in FY26

- Industrial activity, infrastructure spending, steel demand remain resilient

Data Deep Dive: Rising crude oil prices, monsoon uncertainty are emerging as the key risks to inflation

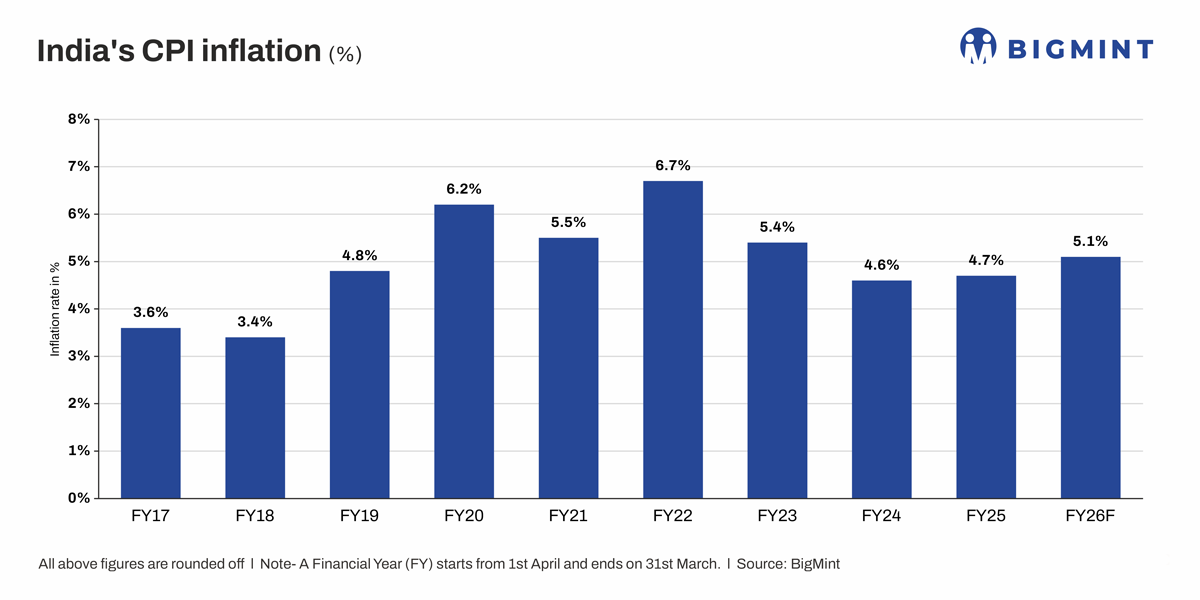

India's economy enters FY27 facing a growing disconnect between household consumption and industrial activity, as rising inflation threatens purchasing power while investment and manufacturing demand remain resilient. The Organisation for Economic Co-operation and Development (OECD) expects GDP growth to slow to 6.3% in FY27 from an estimated 7.6% in FY26, citing higher food and energy prices, weaker purchasing power and slower consumption growth. At the same time, inflation is projected to accelerate to 4.8%, reflecting rising fuel, fertiliser and import costs alongside a weaker currency.

While the headline growth forecast points to moderation, the broader economy continues to exhibit considerable strength. Industrial production remains firm, infrastructure activity has reached record levels and demand for steel and manufactured goods continues to expand. The result is an economy that is not facing an immediate growth crisis but is increasingly vulnerable to inflation. The key question for FY27 is whether rising prices become severe enough to undermine consumption before investment and industrial activity can continue carrying growth.

The answer will have important implications for commodity markets. A consumption-led slowdown would weigh on sectors tied to household spending, while continued resilience in investment would support demand for steel, industrial metals and construction materials. Current indicators suggest the latter remains the more likely outcome, although the balance could shift if inflation accelerates further during the second half of FY27.

Inflation returns as the primary macroeconomic risk

The OECD expects higher food and energy prices to erode household purchasing power, weaken private consumption and increase pressure on businesses facing rising operating costs. India remains particularly exposed to global energy markets given its dependence on imported crude oil and natural gas, leaving the economy vulnerable to disruptions in the Middle East and sustained strength in international energy prices.

Inflationary pressures are already beginning to emerge across the economy. Wholesale price inflation accelerated to 9.68% in May from 8.26% in April, reaching its highest level in more than three years. Fuel and power inflation rose above 30%, while manufactured product inflation also strengthened. The largest increases were recorded in crude petroleum, natural gas, petroleum products, chemicals and basic metals, suggesting higher energy costs are increasingly moving through industrial supply chains. The sharp acceleration in wholesale inflation indicates that cost pressures are building across the production chain even before they are fully reflected in consumer prices.

Consumer inflation remains considerably lower than wholesale inflation, but the gap may prove difficult to sustain if producer costs continue rising. Higher energy prices affect far more than fuel consumption. They influence freight rates, fertiliser costs, manufacturing inputs and food distribution networks, allowing inflationary pressures to spread gradually through the broader economy.

Monsoon conditions represent an additional source of uncertainty. Rainfall during the opening phase of the southwest monsoon has remained below normal, while meteorologists continue to monitor evolving El Nio conditions. A weaker monsoon would not necessarily derail economic growth, but it could place further upward pressure on food prices at a time when energy-driven inflation is already building. Together, higher fuel costs and weather-related food inflation represent the most significant upside risks to India's inflation outlook during FY27.

If these pressures persist, policymakers may face a more difficult trade-off between supporting growth and containing inflation. Higher interest rates or tighter financial conditions would likely be felt first through consumption and smaller businesses, while large infrastructure and industrial projects are generally less sensitive to short-term financing costs.

Industrial activity continues to provide support

Despite concerns surrounding inflation and consumption, industrial indicators continue to paint a more constructive picture of the economy. Industrial production strengthened through April, with the overall index reaching its highest level in the available series. More importantly, the strongest growth continues to occur in sectors linked to investment rather than discretionary consumption.

Infrastructure and construction goods output climbed to a record 240.45 in April, while capital goods production rose to 164.01. Both indicators suggest businesses continue to invest and that construction activity remains healthy despite a more challenging macroeconomic backdrop. These sectors tend to be highly sensitive to economic confidence and investment expectations, making their continued strength particularly significant.

Manufacturing activity also remains expansionary. Purchasing Managers' Index readings continue to indicate growth, while GST collections remain strong. Business sentiment has generally held up better than consumer sentiment, reinforcing the view that industrial activity remains more resilient than household demand.

This distinction is increasingly important because it suggests the economy is not slowing uniformly. Instead, weakness is emerging primarily through the consumption channel, while industrial and investment activity continue to provide support. Such divergence often characterises periods when inflation rises but capital expenditure cycles remain intact.

The implication for FY27 is that growth could become increasingly dependent on investment rather than consumption. If infrastructure spending, manufacturing expansion and project execution continue at current rates, they could offset part of the drag from weaker household demand and prevent a sharper slowdown in overall economic activity.

Steel demand highlights the strength of investment-led growth

Few indicators illustrate the resilience of India's investment cycle more clearly than steel consumption. BigMint data indicate finished steel consumption is projected to rise from 161.14 million tonnes in FY26 to 174.85 million tonnes in FY27, extending a growth trend that has remained intact despite repeated concerns over slowing economic activity.

Recent monthly data point in the same direction. Finished steel consumption increased 9% y-o-y in May to 14.33 million tonnes, supported by infrastructure construction, manufacturing activity and project execution. Consumption growth also continued to outpace production growth, highlighting the strength of underlying demand.

Steel consumption matters because it provides a direct link to economic activity. Infrastructure projects, construction work, manufacturing facilities, logistics networks and industrial expansion all require steel. Sustained growth in steel demand therefore suggests investment activity remains healthy even as headline GDP forecasts are revised lower.

The same trend is visible in other industrial indicators. Passenger vehicle sales remain close to record levels, while construction activity continues to support demand for cement, engineering products and industrial metals. Together, these indicators point to an economy where investment remains a meaningful source of growth despite rising macroeconomic headwinds.

Looking ahead, this suggests that demand for steel and other investment-linked commodities may continue to grow faster than headline GDP. Large infrastructure projects, manufacturing investments and capacity additions typically have long execution timelines, making them less vulnerable to short-term swings in consumer confidence or inflation.

Consumption is becoming the battleground

While industrial activity remains supportive, the outlook for consumption is becoming more uncertain. The OECD expects private consumption growth to slow from 8.2% in FY26 to 6.8% in FY27 as inflation reduces household purchasing power.

The mechanism is relatively straightforward. Higher fuel costs increase transportation expenses and household expenditure. Rising food prices reduce discretionary spending. Elevated inflation ultimately erodes real income growth, limiting consumers' ability to maintain previous spending patterns. The impact is often most visible in rural areas, where agricultural incomes remain closely linked to weather conditions and food prices.

The emerging risk is therefore not a collapse in demand but a gradual moderation in consumption growth. This distinction matters because consumption has been one of the most important drivers of India's post-pandemic recovery. If household spending slows materially while inflation remains elevated, overall growth could weaken even if investment activity remains resilient.

At present, however, there is limited evidence of a broad-based deterioration in demand. Consumer-facing sectors continue to perform reasonably well, while vehicle sales and formal-sector indicators remain healthy. The challenge for policymakers will be preventing inflation from becoming sufficiently entrenched to materially alter spending behaviour.

The next few months are therefore likely to be critical. If energy prices moderate and monsoon conditions improve, consumption could stabilise and support a more balanced growth profile. However, sustained inflation would increase the risk that slower household spending becomes a more significant drag on economic activity during the latter part of FY27.

Outlook

India enters FY27 facing a more challenging macroeconomic environment than it did a year ago. Higher crude oil prices, monsoon uncertainty and rising inflation are likely to place increasing pressure on household purchasing power and consumption growth. These risks explain why institutions such as the OECD expect economic growth to moderate over the coming year.

However, the broader economy continues to display considerable resilience. Infrastructure activity remains strong, manufacturing output continues to expand and steel consumption points to a healthy investment cycle. The available evidence therefore suggests that India faces an inflation challenge rather than a growth crisis.

For commodity markets, this distinction is critical. Demand growth may moderate as consumption slows, but industrial activity and infrastructure spending continue to provide support for steel, industrial metals and construction-linked commodities. Unless inflation accelerates significantly beyond current expectations, investment-led sectors are likely to remain the primary drivers of economic activity through FY27.

As a result, FY27 is likely to be defined less by the pace of economic growth and more by the economy's ability to absorb higher inflation without disrupting the investment cycle. Current indicators suggest industrial activity remains strong enough to support growth even as consumption moderates, but the trajectory of energy prices, food inflation and the monsoon will ultimately determine whether resilience remains the dominant theme through the year.