India: ECL auctions witness selective participation amid weak industrial demand

...

- G4 coal dominates allocations

- Buyers avoid aggressive stock-building

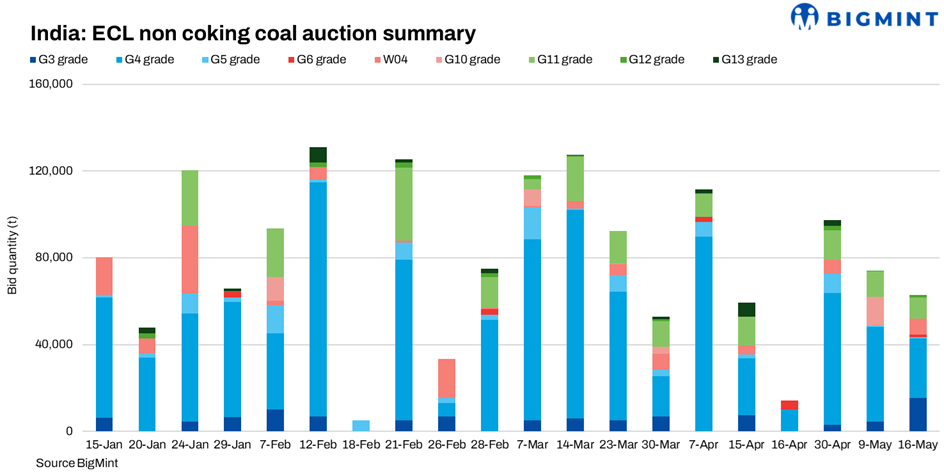

Eastern Coalfields Limited (ECL) conducted non-coking coal auctions on 9th May and 16th May 2026, offering around 981,250 t and 895,350 t, respectively. However, actual allocations remained limited at around 74,250 t on 9th May and 62,950 t on 16th May, reflecting cautious buyer participation despite sizeable offered volumes. Weak sponge iron and steel demand, comfortable domestic coal availability limiting aggressive procurement activity. Compared with the April auctions, buyers largely remained focused on selective quality grades and requirement-based purchases rather than broad-based stock-building.

G4, G3 grades dominate auction activity

G4 coal remained the most actively traded grade across both May auctions, continuing the trend seen in April . In the 9 May auction, G4 allocations stood at 43,750 t at an average bid price of INR 4,674/t. Meanwhile, higher-grade G3 coal fetched one of the strongest premiums at INR 7,492/t for 4,500 t from Jambad UG, reflecting niche industrial demand and limited availability.

The 16 May auction witnessed firmer G4 participation, with allocations of 27,350 t at an average bid price of INR 5,418/t. G3 participation also improved sharply, with 15,500 t allocated around INR 5,346/t. Market participants stated that buyers continued preferring better-quality coal suitable for sponge iron operations despite subdued overall industrial sentiment.

Lower-grade G9 and G11 coal continued witnessing comparatively weaker premiums around INR 1,776/t and INR 2,154/t, respectively, reflecting cautious buying interest in lower-grade material amid comfortable domestic coal availability.

Compared with the 30 APRIL auction, G4 coal premiums improved further in the MAY auctions despite cautious market sentiment. G4 prices increased from around INR 4,934/t on 30 APRIL to INR 5,418/t in the 16 MAY auction, reflecting continued demand for better-quality coal suitable for sponge iron operations.

Meanwhile, G11 coal prices largely remained stable around INR 2,154/t across the 30 APRIL, 9 MAY and 16 MAY auctions, indicating subdued interest in lower-grade coal amid comfortable domestic availability and weak downstream industrial demand.

Underground mines continue attracting premiums

Mine-wise participation remained concentrated at selective underground and premium-quality mines rather than broad-based procurement. In the 9 May auction, Begunia OC accounted for the largest allocation at 13,250 t of G9 coal, while Jhanjra UG witnessed strong G4 premiums around INR 5,054/t for 10,000 t.

Underground mines continued fetching stronger realisations due to limited availability and operational suitability. Jambad UG recorded one of the highest premiums at INR 7,492/t for G3 coal, while Narsamuda UG fetched around INR 5,890/t for G4 material.

Similarly, in the 16 May auction, Chitra OC emerged as the highest allocated mine with 10,000 t of G3 coal at INR 5,445/t. Premium underground mines such as Parbelia UG, Nimcha UG and Patmohona UG continued attracting aggressive bids above INR 6,000/t, indicating continued demand for niche-quality coal despite weak downstream market conditions.

Sponge iron-linked buyers stay active

Buyer participation remained concentrated among sponge iron producers, industrial consumers and traders. In the 9 May auction, MB Sponge & Power emerged as the largest buyer, securing 9,650 t of G4 coal at INR 4,907/t. Compact Weighing also participated actively, procuring 8,000 t of G9 coal around INR 1,776/t.

Other active participants included Calstar Sponge, Bhagwati Enterprises and Greenosphere Renewable Energy, indicating continued selective procurement from industrial consumers despite subdued finished steel demand.

Participants stated that most buyers continued maintaining requirement-based procurement strategies instead of aggressive stock-building, as comfortable domestic coal supply and weak sponge iron margins continued pressuring broader market sentiment.

Outlook

ECL auction participation is expected to remain selective in the near term amid comfortable domestic coal availability, weak sponge iron margins and subdued industrial demand. However, premium underground grades are likely to continue attracting firm bids due to limited supply and operational suitability for sponge iron and industrial consumers. Increasing auction volumes by coal companies may continue limiting sharp premium increases unless downstream steel demand improves meaningfully.