India: Domestic aluminium prices decline w-o-w following sharp LME correction

...

- LME prices fall 6% amid concerns over global industrial demand

- Strong demand, lower imports may support near-term domestic prices

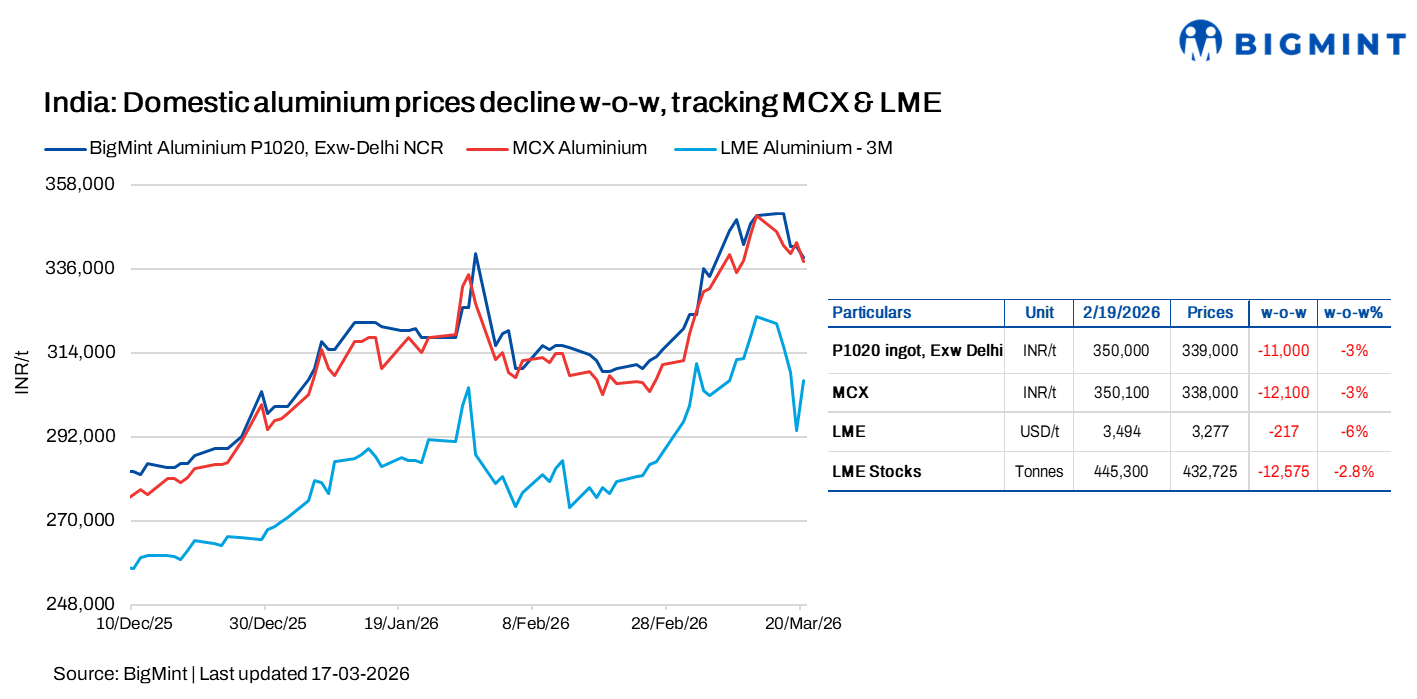

Domestic aluminium prices in India declined w-o-w on 19 March 2026, tracking weakness in aluminium futures on the London Metal Exchange (LME) and Multi Commodity Exchange of India (MCX), amid easing global supply concerns and volatile sentiment due to ongoing geopolitical tensions.

As per BigMint's assessment, domestic aluminium P1020 ingot prices in Delhi NCR fell by INR 11,000/t, or around 3%, w-o-w to INR 339,000/t, compared to INR 350,000/t in the previous week. Similarly, Mumbai prices declined by INR 12,000/t, or about 3.4%, w-o-w to INR 340,000/t, from INR 352,000/t last week.

How did Indian and global exchanges perform?

Domestic aluminium futures on the MCX declined by INR 12,100/t, or around 3%, w-o-w to INR 338,000/t, indicating weaker market sentiment.

In the global market, 3-month aluminium prices on the LME also fell by $217/t, or 6%, w-o-w to $3,277/t. Meanwhile, stocks at LME-registered warehouses declined by 12,575 t, or 2.8%, w-o-w, with total inventories standing at 432,725 t.

LME aluminium prices declined by around 6% w-o-w to $3,277/t after a sharp correction during the week, including a drop of over 8%, the biggest since 2018, to near $3,115/t, which erased earlier gains driven by Middle East supply concerns. While prices had rallied to around $3,500/t on fears of disruptions to supply chains and key shipping routes, sentiment shifted as markets began pricing in the broader economic impact of the Iran conflict, raising concerns over global growth and industrial demand.

The fall was further driven by profit booking and liquidation of speculative long positions amid heightened volatility and risk off sentiment. Despite a 2.8% w-o-w decline in LME inventories indicating continued tight supply, macroeconomic uncertainty dominated, leading to the overall w-o-w price decline.

Market insights

Reflecting the recent market correction, NALCO reduced its primary aluminium ingot (P1020, 99.7%) prices by INR 12,000/t to INR 360,000/t on 19 March 2026 from INR 372,000/t on 14 March.

BALCO also decreased its P1020 ingot prices by INR 31,000/t from INR 389,250/t on 14 March to INR 358,250/t on 20 March. Similarly, Hindalco lowered prices by INR 7,000/t from INR 387,250/t on 14 March to INR 380,250/t on 17 March.

Primary aluminium producers in India are expected to face limited direct impact from the US Iran conflict, as most smelters rely on domestic power sources and procure key raw materials from outside the GCC region. Strong domestic demand and the possibility of reduced imports from the Middle East, which accounts for nearly 30% of Indias aluminium ingot imports, could further support local producers.

However, indirect cost pressures may arise due to potential disruptions in industrial gas supply, rising coal prices amid freight constraints, and possible tightening of pet coke availability, which could impact overall production costs.

At the same time, Indian gas suppliers have signalled potential curbs on industrial gas availability, with aluminium processors dependent on LNG currently receiving only around 80% of their contracted volumes. This shortfall is prompting some producers to shift to alternative fuels such as furnace oil, leading to higher operating costs.

Industry participants estimate that the change in fuel mix could raise finished product costs by nearly 20-25%.

Additionally, export operations are facing challenges due to the closure of a key UAE port, disrupting shipments to the Middle East, a crucial market, where some producers ship close to 70% of their exports.

Outlook

Domestic aluminium prices are likely to see minor corrections following the sharp fall in LME levels, though the market is expected to remain volatile. Trends will continue to track movements in LME and MCX amid ongoing geopolitical tensions and macroeconomic uncertainty. While tight global inventories and steady domestic demand may offer some support, weak sentiment, rising input costs, fuel switching, and export disruptions could pressure margins, making it important to closely monitor global developments.