India: Coking coal imports fall 24% m-o-m in Oct'25 amid lacklustre steel market

...

- Australian, Russian shipments drop sharply

- JSW Steel, Tata Steel cut intake; SAIL steady

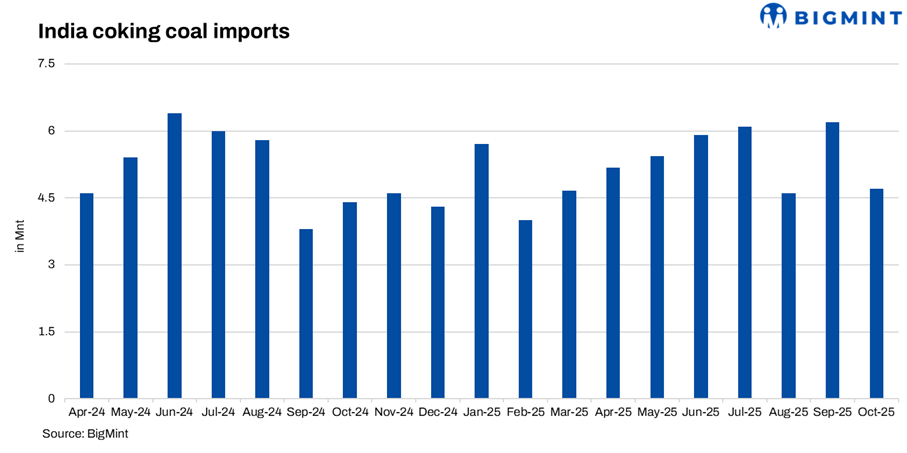

India's coking coal imports dropped 24% m-o-m to 4.7 mnt in October 2025 from 6.2 mnt in September, as shipments from key suppliers Australia and Russia declined. Imports, however, remained 9% higher than the 4.3 mnt recorded in October 2024.

Australia, Russia drive decline

Australia's exports to India fell to 2.9 mnt from 3.5 mnt, while Russian volumes dropped sharply to 0.5 mnt from 1.5 mnt. The US also shipped lower volumes of 0.5 mnt versus 0.7 mnt previously. Imports from Mozambique remained steady at 0.4 mnt, whereas Indonesia and Canada supplied 0.2 mnt each.

Steel majors reduce intake

JSW Steel's imports dipped to 1.1 mnt from 1.8 mnt in September, while Tata Steel's fell to 0.8 mnt from 1.4 mnt. SAIL maintained steady procurement at 1.3 mnt, whereas RINL's intake rose marginally to 0.3 mnt. Jindal Steel and Power also imported slightly less at 0.3 mnt compared with 0.4 mnt last month.

Reason for lower imports in Oct'25

Indian primary mills cut rebar, HRC prices: At the start of the month, the primary mills increased rebar prices by up to INR 1,000/t ($11/t) for early-October deliveries as against levels prevailing in end-September. However, trade-level blast furnace (BF) rebar tags declined in mid-October, and consequently, major primary mills either offered discounts or reduced list prices due to subdued sentiment ahead of Diwali.

Similarly, in the HRC market, the leading steel manufacturers reduced prices of hot-rolled coils (HRCs) and cold-rolled coils (CRCs) by INR 750-1,500/t ($8-17/t) for October sales as compared to early-September in the first week. The market remained sluggish as slow demand, oversupply, and high inventories pressured prices. Buyers limited purchases to immediate needs, avoiding bulk bookings.

Input costs rise amid coking coal price hike in Oct: BigMint's CFR India index for premium hard coking coal showed a marginal uptick of 5% m-o-m in August due to the hike in offers from Australia following higher prices fetched in the Chinese market. The Chinese market for met coke witnessed its second straight round of price hike recently in response to tight supply and resilient demand. Therefore, Indian buyers were obliged to accept higher coal tags, which led to an increase in input costs despite low steel prices.

Latest price trends

In the east, BF-grade (25-90 mm) met coke prices were assessed at INR 31,000/t ex-Jajpur, a rise of INR 500/t w-o-w. Notably, met coke prices in eastern India climbed to nearly a 6-month high, levels last seen at the end of May 2025. In contrast, western India's prices stayed firm at INR 30,000/t ex-works Gandhidham, while foundry-grade met coke was stable at INR 35,500/t ex-Rajkot.

Outlook

Imports are expected to recover in November as Indian steel mills replenish inventories following the festive season and ahead of winter demand, though buying may remain selective amid stable seaborne prices and adequate stock levels at plants.