India: Coal supply surging ahead of demand, Mar'26 dispatch lag builds up inventory pressure

...

- Supply exceed demand, pushing coal stocks above 151 mnt

- CIL holds most inventory on high output and slower offtake

The Ministry of Coal's provisional data for March 2026 indicates a robust finish to the fiscal year, with production surpassing monthly targets and dispatch holding steady. Total production for the month reached 113.67 million tonnes (mnt) , while dispatches (offtake) stood at 96.78 mnt.

Monthly production

Total coal production in March was 113.67 mnt, achieving 113.07% of the monthly target of 100.53 mnt. However, this represents a marginal decline of 4.09% compared to March 2025 production levels.

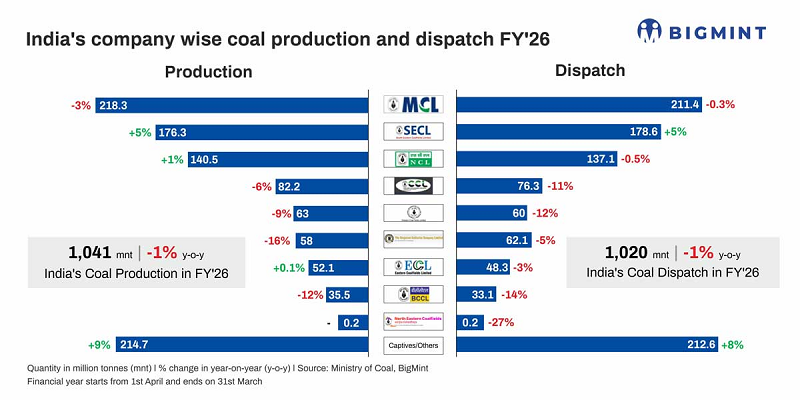

Company-wise performance:

- CIL (Coal India Ltd): Produced 84.46 mnt, achieving 90.34% of its monthly target.

- SCCL (Singareni Collieries): Produced 5.17 mnt.

- Captives/Others: Contributed 24.05 mnt, showing a slight year-on-year growth of 0.96%.

For the full fiscal year 2025-26, total coal production reached1,040.83 mnt, a marginal decline of 0.64% compared to FY 2024-25 (1,047.52 mnt).

Monthly dispatches (offtake)

Total coal dispatches in March was 96.78 mnt, achieving 108.83% of the monthly target of 88.93 mnt. Dispatch showed a y-o-y growth of 1.47% compared to March 2025 (95.38 mnt).

Company-wise dispatches:

- CIL: Dispatched 69.39 mnt (100.51% of target).

- SCCL: Dispatched 6.55 mnt (92.89% of target).

- Captives/Others: Dispatched 20.84 mnt.

For the full fiscal year 2025-26, total dispatches reached 1,019.50 mnt, marginally lower (0.57%) than FY 2024-25 (1,025.33 mnt).

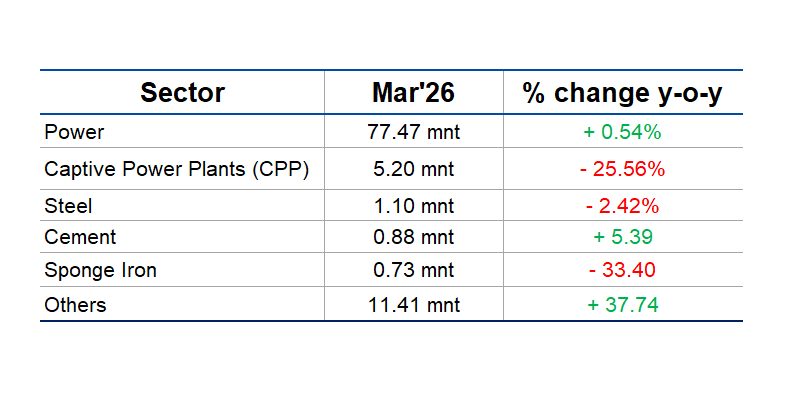

Dispatches to end-use industries

Dispatches to key consumer sectors during March showed mixed trends compared to the same month last year. The power sector remained the dominant consumer, accounting for approximately 80% of total dispatch.

For the full fiscal year, dispatches to the power sector stood at 807.50 mnt ( -2.92% vs FY 2024-25), while dispatches to the steel sector declined by 14.86% to 15.84 mnt.

Rail rake loading performance

The average daily loading of railway rakes (for all sectors) during March showed a slight decline compared to the same month last year.

- Actual daily avg. loading (March 2026): 338.38 rakes per day

- Achievement vs monthly target:81.73%

- Growth vs March 2025: -0.41%

Among major subsidiaries:

- SECL recorded the highest growth in daily rake loading (-15.31% vs March 2025), averaging 59.5 rakes per day.

- NCL showed strong growth (-11.52%), averaging 48.4 rakes per day.

- BCCL saw a significant decline (-29.97%), averaging 20.1 rakes per day.

For the power sector alone, the average daily rake loading in March was 294.7 rakes per day, a decline of 2.71% compared to March 2025.

Based on the opening stock as of 30 September 2025 (as reported in the Quarterly Booklet) and the cumulative net change-calculated as production minus despatch-from October 2025 to March 2026, the estimated pit-head closing stock of coal in India as of 31 March, 2026 stands at 151.18 mnt.

A significant majority of this inventory is held by Coal India Limited (CIL), which accounts for 130.76 mnt. This underscores CIL's dominant position in the country's coal sector and highlights the extent of inventory accumulation driven by strong production levels relative to offtake.

SCCL (Singareni Collieries Company Limited) holds a comparatively smaller stock of 4.93 mnt, while captive and other producers together account for 15.49 mnt of coal stock.

What this means for the market

March data points to a clear and important shift in the coal market balance:

1. Supply is running ahead of demand

Production growth remains strong, but dispatch has not kept pace, leading to inventory accumulation. With total pithead stocks exceeding 150 mnt, the market is entering a phase of comfortable to surplus supply conditions.

2. CIL is carrying the stock burden

Nearly the entire stock build is concentrated with CIL (130.76 mnt out of 151.18 mnt total), reflecting:

Aggressive production targets

Slower-than-expected offtake from key consumers

Limited evacuation capacity in certain mining regions

3. Power demand is steady, not surging

While the power sector continues to absorb the majority of coal (over 80% of total dispatch), demand growth is not strong enough to clear rising supply. Power sector dispatches grew only 0.54% in March, while production grew at a faster pace.

4. Logistics constraints are becoming visible

Rake loading levels (338 rakes per day, below the target of 414) suggest the rail network is operating near capacity, limiting faster evacuation. The power sector saw even lower achievement at 85.9% of its rake loading target, indicating potential bottlenecks in coal transportation to thermal power plants.

Inventory overhang to shape near-term market

With pithead stocks now estimated at over 150 mnt, the market is entering a phase of comfortable supply conditions. For context, this represents approximately 1.5 months of dispatch at current run rates.

In the near term, this inventory overhang could translate into:

- Reduced urgency for imports - Domestic buyers may rely more on accumulated stockpiles

- Softer domestic spot market conditions - Oversupply typically exerts downward pressure on e-auction premiums

- Increased pressure on miners - Particularly CIL, to align production growth with actual demand offtake

Unless dispatch accelerates sharply in April and May with rising summer power demand (typically a peak consumption period), the coal sector is likely to remain in a supply-heavy phase, with inventories acting as a buffer against any short-term demand spikes.

Market participants will be closely watching:

- Summer power demand trends (April-June 2026)

- Rake availability and logistics performance

- Any production adjustments by CIL in response to stock levels

*Note: All figures are provisional as per the Ministry of Coal's Monthly Coal Statistics for March 2026. The pit-head stock calculation is based on the opening stock reported in the Quarterly Booklet (2nd Quarter 2025-26) and cumulative monthly production and dispatch figures from October 2025 to March 2026 as reported in the respective monthly statistical statements.*