India: Coal freight rates soften across key routes on thin enquiries, limited fixtures

...

- Ample Pacific tonnage weighs on Panamax sentiment

- Holiday-led slowdown pressures Supramax market

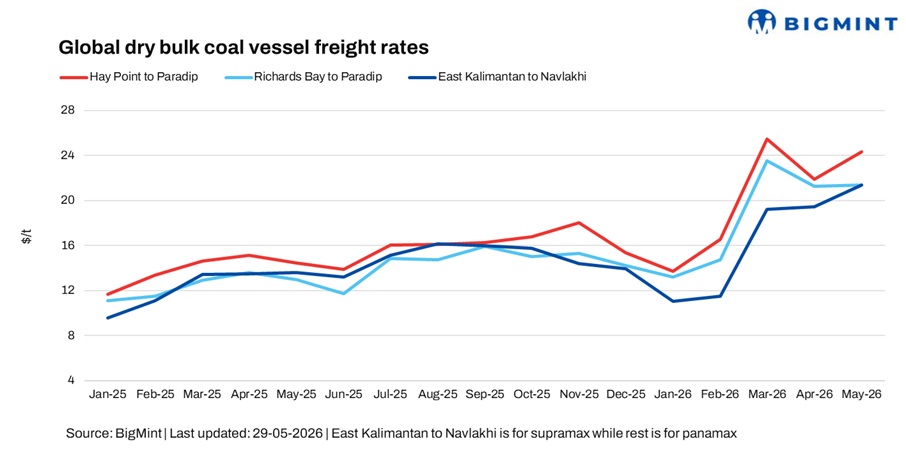

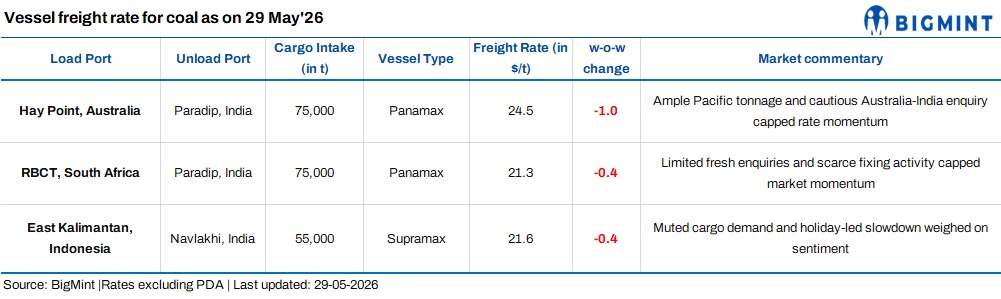

Dry bulk coal freights to India softened across key routes in the week ended 29 May, as subdued cargo enquiries and limited fixture activity weighed on sentiment. While Pacific Panamax routes faced pressure from ample vessel availability, the Supramax segment was impacted by muted demand and holiday-related disruptions across Asia and the Middle East.

Market participants remained on the sidelines amid a lack of fresh enquiries. A shipbroker said, "There is not much expected this week, though market sentiment remains steady."

Another shipbroker said, "Market activity is very slow at the moment." When asked whether fixtures were taking place, he replied, "Enquiries are on the lower side, with limited activity being observed in the market."

Route-wise update

In the Pacific, the Australia-India Panamax route remained under pressure as ample vessel availability and cautious chartering interest capped rate momentum. While Panamax sentiment has shown signs of stabilisation, cargo volumes remain insufficient to tighten vessel supply.

On the South Africa-India route, limited fresh enquiries and scarce fixing activity kept sentiment subdued amid balanced vessel availability.

Meanwhile, the Supramax segment faced pressure from muted cargo demand and holiday-related slowdown, with limited Indonesian trading interest and few fresh fixtures reported.

Market highlights

- Baltic Dry Index extends gains w-o-w: The Baltic Dry Index (BDI) rose by 262 points w-o-w to 3,226 on 28 May, supported by stronger earnings in the larger vessel segments. The Panamax index increased by 55 points to 2,331, reflecting improving sentiment in the Pacific market, while the Supramax index eased by 2 points to 1,569 amid subdued regional cargo activity and balanced vessel availability across key trade routes.

- Bunker prices edge down w-o-w: Bunker prices declined by $41/tonne (t) w-o-w to $762/t as of 29 May, from $803/t a week earlier, tracking weaker crude oil prices and subdued buying interest across major bunkering hubs.

- Brent crude futures ease w-o-w: Brent crude oil (July 2026 contract) was last assessed at $92.10/barrel (bbl) on 29 May, down by $13.40/bbl from $105.50/bbl a week earlier, amid weaker global energy market sentiment and concerns over demand growth.

- DCE coke futures firm: Coke futures on the Dalian Commodity Exchange were assessed at RMB 1,901/t ($280.39/t) for the September 2026 contract as of 29 May, reflecting market expectations and sentiment surrounding China's coke and steel sectors.

Outlook

Coal freights to India are expected to remain range-bound. Panamax sentiment may find support if cargo enquiries improve and absorb available tonnage, while the Supramax market is likely to remain influenced by regional cargo activity and post-holiday participation levels.