India: CIL coal auction premiums moderate in Q1FY'27 amid improved supply availability

...

- Comfortable supply reduced auction dependency, softening premiums

- Bids rose 44% over notified price in Q1 FY'27, largely stable y-o-y

Coal India Limited (CIL) continued to witness moderation in price premiums under its Single Window Mode Agnostic (SWMA) e-auction platform during June 2026, as market conditions remained balanced due to improved coal availability, sufficient consumer inventories, and enhanced supply through regular linkages.

The average premium over notified prices stood at 42% in June 2026, higher than 36% recorded in May 2026, reflecting improved realisations amid steady demand for assured and grade-specific coal supplies. On a broader comparison, premiums during Apr-Jun 2026 averaged 44%, remaining largely stable compared with 45% during Apr-May 2026, indicating a gradual moderation in auction realisations as supply availability improved and buyers adopted a more selective procurement approach.

Auction volumes increase, but buyer participation remains selective

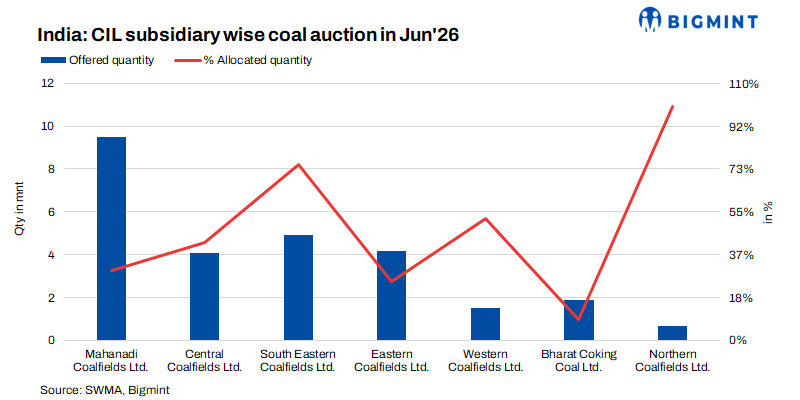

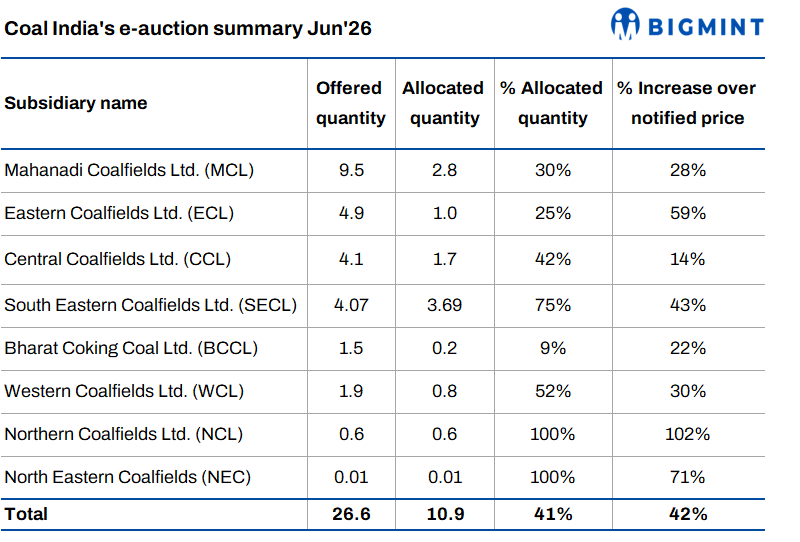

During June 2026, CIL offered 26.62 million tonnes (mnt) of coal through the SWMA platform, marginally higher compared with 25.71 mnt in May 2026, reflecting continued availability from domestic producers. However, only 10.88 mnt was allocated, translating into an allocation rate of 41%. For the cumulative Apr-Jun 2026 period, CIL offered 82.91 mnt, against which 31.07 mnt was allocated, resulting in an overall allocation rate of 37%.

The relatively moderate allocation ratio highlights a cautious procurement approach among consumers, as buyers remained focused on immediate requirements rather than aggressive stock accumulation amid comfortable supply conditions.

Premiums ease as supply fundamentals improve

The decline in auction premiums during June 2026 was primarily driven by improved domestic coal availability and reduced dependence on spot purchases. Adequate inventory levels with power utilities and industrial consumers, along with better availability through long-term linkage mechanisms, reduced urgency in e-auction participation.

As a result, overall bidding intensity moderated, leading to softer premium realisations. However, premiums remained positive, indicating continued demand for reliable supply, specific coal grades, and operational flexibility offered through the SWMA platform.

NCL, SECL and NEC continue to demonstrate strong demand strength

Among CIL subsidiaries, South Eastern Coalfields Ltd (SECL) emerged as one of the strongest performers, achieving an allocation rate of 75% in June 2026. SECL secured a premium of 43% over notified prices, reflecting stable demand from power and industrial consumers despite a marginal decline from previous levels.

Northern Coalfields Ltd (NCL) continued to witness robust demand momentum, achieving 100% allocation of offered quantities during June 2026. The company recorded the highest premium realisation among subsidiaries at 102% over notified prices, supported by strong regional demand, proximity advantage, and tight availability of preferred coal grades.

Similarly, North Eastern Coalfields Ltd (NEC) recorded 100% allocation in June 2026, with premium realisation of 71% over notified prices, reflecting firm demand conditions in its operating region.

MCL leads auction volumes but faces moderate absorption levels

Mahanadi Coalfields Ltd (MCL) remained the largest contributor to auction volumes, offering 9.5 mnt during June 2026. However, allocation remained moderate at 30%, indicating comparatively softer absorption due to higher availability and sufficient alternative supply options. Premium realisation for MCL declined to 28% during June 2026, compared with 33% during the previous period, reflecting a more balanced demand-supply environment.

Outlook

Going forward, CIL's SWMA auction premiums are expected to remain stable with a moderate bias, as domestic coal availability is likely to remain comfortable and consumers continue to rely on a mix of linkage supplies and auction purchases. The absence of supply constraints may limit aggressive bidding and keep overall premiums below earlier highs.

However, demand for specific grades, strategic locations, and assured supply channels is expected to support stronger premiums for subsidiaries such as NCL, SECL, and NEC. Seasonal power demand, changes in utility inventory levels, and any disruption in domestic production or logistics will remain key factors influencing auction participation and premium realisations in the coming months.