India: Chennai ferrous scrap prices rise by INR 800/t w-o-w on improved steel prices - 9 Apr

...

- Tight availability drives Chennai scrap higher

- Ceasefire sentiment hints at near-term correction

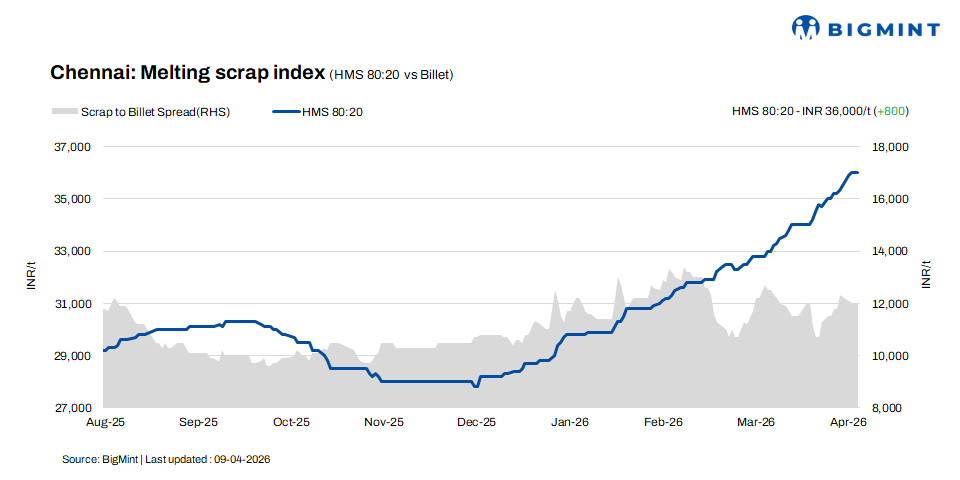

In the Chennai market, HMS (80:20) scrap prices increased by INR 800/t w-o-w to INR 36,000/t on 9 April 2026, while remaining stable on a daily basis, as per BigMints assessment. Billet prices also moved up by INR 500/t w-o-w to INR 48,000/t, with no change observed in daily trading. Similarly, rebar prices rose by INR 200/t w-o-w to INR 53,200/t, holding steady on a d-o-d basis. The overall trend indicates firm market sentiment, supported by steady demand and stable trading activity across both semi-finished and finished steel segments.

Imported and domestic price trends

Market participants reported that Australia-origin shredded scrap was offered at $405-410/t CFR Chennai, while HMS (80:20) was quoted at $385-390/t CFR. However, buyers were bidding $5-10/t lower than the prevailing offer levels. Buying interest remained subdued, as domestic scrap offers are currently more cost-effective compared to imported material, thereby limiting fresh bookings.

In the domestic market, HMS (80:20) scrap prices were quoted at INR 35,500-36,500/t for spot deals with immediate payment, while transactions on extended credit terms were concluded at INR 36,500-37,000/t. Market activity remained largely confined to the INR 35,500-37,000/t range, highlighting stable demand-supply dynamics, with premiums observed for extended payment terms.

Buyer-supplier sentiments

The market is witnessing increased demand for sponge iron, primarily due to its cost advantage over scrap. Ongoing commercial gas supply constraints and lower imported scrap inflows in recent months have resulted in a continued shortage of scrap, supporting its pricing environment.

Meanwhile, active demand for billets and rebar is supporting current price levels. Improved trading activity has been observed in both the project and retail segments over the past few weeks, sustaining overall market sentiment. The current inventory level of rebar at mills is around 10-15 days, indicating balanced supply and steady demand conditions.

A scrap supplier indicated that HMS (80:20) prices are currently hovering in the range of INR 35,500-37,000/t, with variations largely dependent on payment terms and mill-specific volume requirements. The ongoing commercial gas shortage continues to disrupt scrap cutting and processing activities, limiting effective supply in the market.

Additionally, lower arrivals and reduced bookings of imported scrap have further tightened availability, creating upward pressure on domestic prices. With both processing constraints and limited imports, the market is experiencing supply-side stress, supporting firm pricing trends in the near term.

Regional comparison

In the western India based Jalna market, billet and HMS (80:20) scrap prices remained stable at INR 47,000/t and INR 34,000/t, respectively. Meanwhile rebar prices drop by INR 100/t to INR 54,200/t. However, the recent US-Iran ceasefire announcement has triggered a notable shift in market sentiment. Scrap suppliers, who were earlier holding material in anticipation of further price increases, have now entered panic selling mode, releasing inventory into the market.

This has led to improved scrap availability and increased transaction volumes, easing earlier supply tightness. As a result, despite current stability in prices, the market is witnessing downward pressure, with indications of a correction in scrap prices during recent trading sessions.

Outlook

The Chennai market is expected to remain stable to firm, supported by tight scrap availability and gas-related supply constraints. Demand for billet and rebar continues to provide support to prices. However, post the US-Iran ceasefire, improved sentiment and easing cost pressures may trigger some downward correction in scrap prices.