India: Cement prices likely to remain under pressure in Jul'26 as monsoon slows construction activity

...

- Prices slide in Jun'26 amid weak retail demand, aggressive competition

- Pet coke, crude oil, packaging prices ease, reducing cost support

Indian trade-level cement prices are expected to remain under pressure in July 2026 as widespread monsoon rains slow construction activity across the country, reducing seasonal demand.

Although infrastructure and real estate projects continue, execution has moderated due to weather-related disruptions, resulting in weaker dealer offtake, need-based procurement, and comfortable inventory levels. Market participants expect prices to remain largely stable with a slight downside in some markets.

"Dealers are purchasing only against immediate requirements. Most markets are adequately supplied, leaving limited scope for price hikes," a market participant said.

Why Jun'26 price hikes failed to sustain

Cement manufacturers attempted price increases across major markets during June 2026 to improve realisations. However, weak retail demand, aggressive market competition, and pressure to achieve sales targets prevented these hikes from holding.

A delayed onset of the monsoon helped support prices during the first half of June. However, as rainfall intensified towards the month-end, construction activity slowed significantly, reducing fresh buying and putting pressure on cement prices heading into July.

Regional price movements in trade segment in Jun'26

West: Western India recorded the strongest price retention, supported by healthy infrastructure demand and a delayed monsoon. Mumbai trade prices increased by up to INR 20/bag in early June and remained stable thereafter. Tight availability in Ahmedabad and delivery lead times of 3-4 days supported price realisations.

North & central: Prices remained largely stable as weak retail demand and cautious buying limited mills' pricing power. In Delhi, procurement remained need-based, while Raipur witnessed stable prices amid slow demand and adequate material availability.

East: The eastern region witnessed mixed price realisation as weak demand and competitive pricing weighed on the market. Kolkata prices declined by around INR 10/bag due to slow buying and delays in awarding and executing projecting tenders, which affected construction activity.

South: The southern region recorded the weakest price retention. Prices remained stable in Bengaluru and Chennai, while Hyderabad declined by INR 5-10/bag amid slow demand and oversupply. Competitive pricing continued to pressure realisations.

Non-trade segment remains under pressure

The non-trade segment also weakened during June. Prices declined by up to INR 10/bag m-o-m across several regions, although some bulk contracts were concluded at May levels.

Demand remained subdued as monsoon-related disruptions, slower infrastructure execution, delayed project funding, labour shortages, and transportation challenges affected procurement activity. Most infrastructure contractors and institutional buyers continued to procure cement only against immediate project requirements rather than building inventories.

Easing input costs improve industry outlook

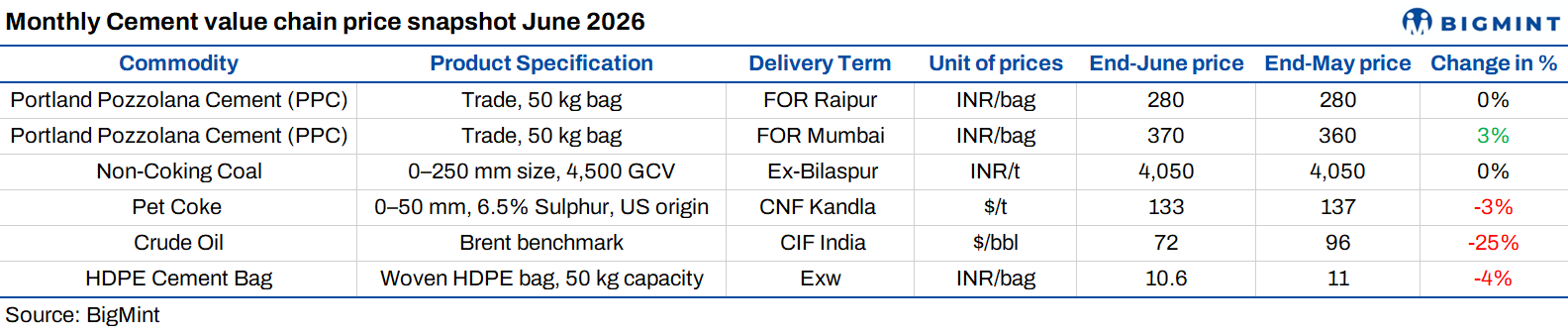

Input cost pressures eased further in June 2026, offering some relief to cement manufacturers and reducing cost support. Brent crude oil prices declined 25% m-o-m to $72/bbl, reducing freight and logistics cost pressures, while US-origin pet coke prices fell 3% to $133/t CNF Kandla and HDPE cement bag prices declined 4% m-o-m. Domestic non-coking coal prices remained stable, supporting fuel cost predictability.

Despite the improvement in production costs, the benefit has yet to translate into cement price realisations. Weak monsoon-led demand, comfortable supply, and cautious dealer procurement continued to weigh on market, keeping trade-level cement prices under pressure across most regions.

Outlook

Trade and non-trade cement prices are expected to remain under pressure throughout July 2026 as monsoon rains continue to affect construction activity across most parts of the country. Ample supplies and cautious buying is likely to keep prices weak. Although cement mills may announce price hikes, these are mainly aimed at preventing further price declines and are unlikely to be sustained.