India-bound ferrous scrap container freights remain under pressure amid weakening import demand

...

- Weak scrap demand, bid-offer disparities keep import activity muted

- Reduced import activity diverts container flows to neighboring markets

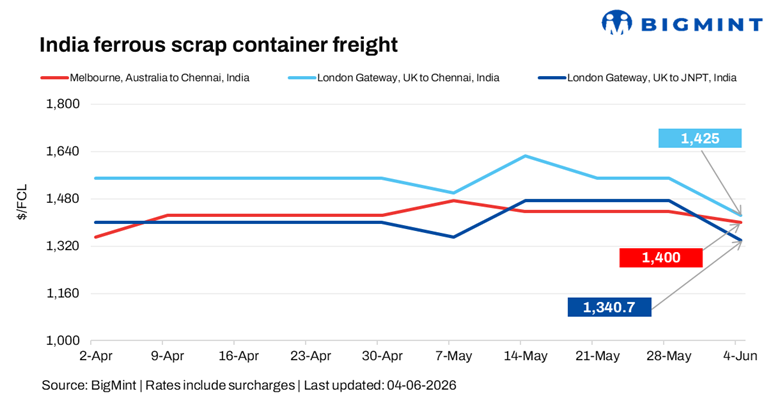

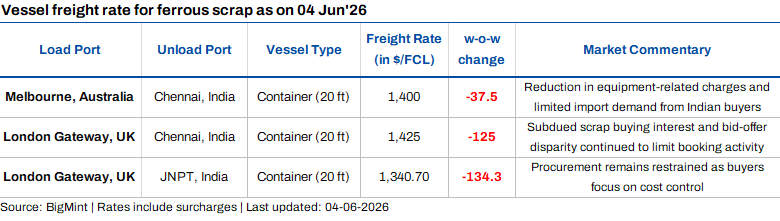

India-bound ferrous scrap container freights remained under pressure in the week ended 4 June across regions. A wide gap between offer and bids continued to restrict trade, while buyers largely adopted a wait-and-watch approach in anticipation of further price corrections, keeping import demand muted.

Container freight sentiment remained soft across both Pacific and Atlantic basins, reflecting cautious procurement, weak steel market fundamentals, and a persistent focus on cost optimization.

The Australia route saw slight downward pressure following lower equipment-related charges despite steady cargo availability. An Australian shipbroker noted, "Sentiment remains mildly softer as Equipment Fee (EF)have been revised down, putting slight pressure on freight levels."

A UK-based shipbroker stated, "Ferrous scrap trade activity from the United Kingdom to Chennai remains subdued, as we are exporting non-ferrous scrap of around 20-25 TEUs per month in 40 ft containers. Meanwhile, the bulk of ferrous scrap cargo continues to move to Pakistan via 20 ft containers, accounting for the majority of shipment volumes."

Another source stated, "Current market rates remain largely competitive, with some carriers offering lower pricing while others continue to maintain a premium. A few operators are providing the most cost-effective options, though with relatively longer transit times."

Route-wise update

Market highlights

- CFI gains amid early peak-season demand: The Containerized Freight Index (CFI) gained by 354 points w-o-w to 2,572 points on 29 May, driven by rising freight rates on key East-West trade lanes, supported by early peak-season demand, carrier rate restoration initiatives, and tighter vessel capacity management.

- Bunker prices firm on rising fuel costs: Bunker prices increased by $50/tonne (t) w-o-w to $816/t on 4 June, reflecting strengthening fuel market sentiment. It will increase voyage costs for shipowners and may lend support to freight rates.

Outlook

Ferrous scrap container freight is expected to remain stable to soft in the near term, as cautious buying by South Asian importers and weak steel demand continue to limit cargo volumes. While carriers may attempt to maintain rate levels through capacity management, muted procurement activity and strong focus on cost optimization are likely to cap any significant freight upside.