India: BigMint's scrap index declines by INR 200/t -24 Jan

...

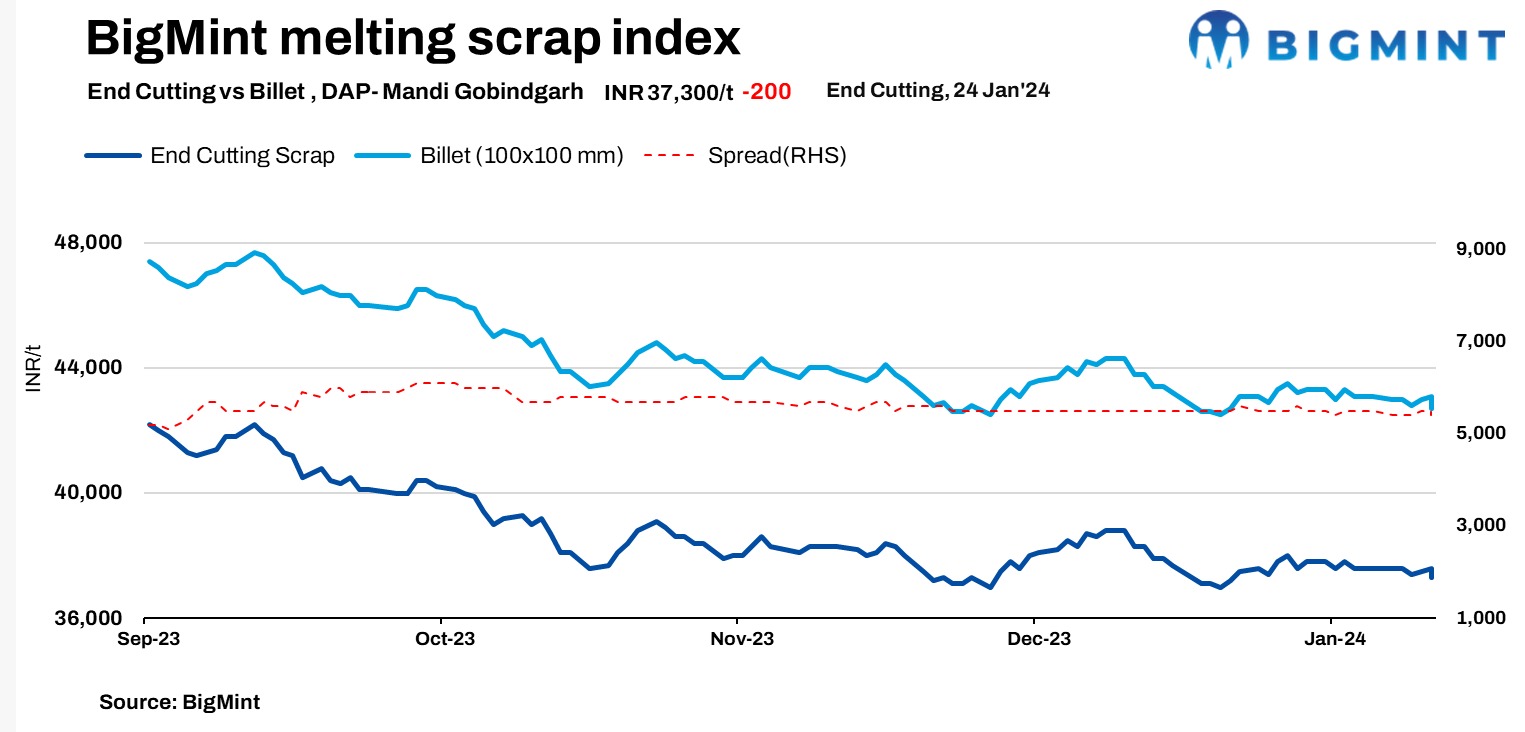

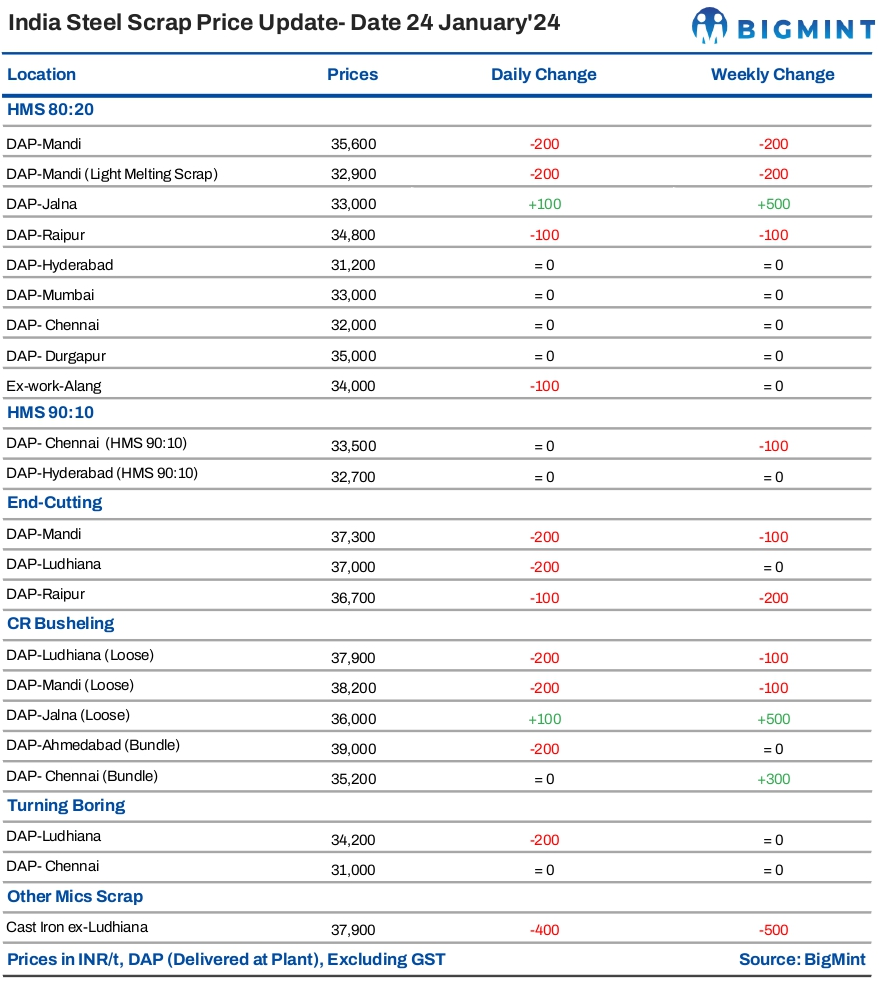

On 24 January, 2024, BigMint's domestic steel scrap (end-cutting) index recorded a decrease of INR 200/t, settling at INR 37,300/t on a delivered-at-plant (DAP) basis in Mandi Gobindgarh. In Mandi, there has been a decent arrival of scrap witnessed in the region, but due to slow trade activity, mills were procuring scrap in average volumes. Additionally, imported scrap remained impractical at the moment. A noteworthy trend was observed, with the majority of mills incorporating sponge iron into their steel-making processes. Furthermore, the winter and cold weather conditions are currently causing disruptions in daily routine work.

A scrap supplier has conveyed that, owing to the sluggish market conditions, suppliers are encountering challenges with so many of mills extending their payment cycles to 10 to 15 days, leading to an increased credit gap. Additionally, the winter and foggy weather are causing disruptions in transportation in certain areas.

Semis' market

In Mandi, steel ingot prices experienced a decline of INR 200/tonne (t), settling at INR 42,700/t at the time of reporting and price normalisation. Concurrently, prices of steel ingots in other significant markets witnessed a decrease within the range of INR 100 to INR 200/t.

"The market is undergoing a challenging phase, with the Mandi steel market experiencing minimal trade activity in both semi-finished and finished steel. As a consequence, prices have seen a decline," a mill owner informed BigMint.

Raw materials price update

In Mandi, the prices for sponge iron (CDRI) underwent a decrease of INR 100/t, settling at INR 31,300/t. Similarly, pig iron (steel grade) prices also saw a decline of INR 100/t, reaching INR 39,500/t on a DAP basis.

Overview of other markets

Gujarat's Alang market saw a marginal dip of INR 100/t d-o-d in ship-breaking melting scrap prices on 24 January, 2024. BigMint's assessment reported the commencement prices of HMS (80:20) at INR 34,000/t ex-yard. Limited activity in the trade of semi-finished and finished steel during the trading session on the previous day, along with moderate buying inquiries for scrap, prompted suppliers to adjust their offers downward today.

In the Chennai market, based in South India, semi-finished steel prices experienced a decline of INR 300/t, settling at INR 42,500/t, while rebar and HMS 80:20 prices held steady at INR 47,500/t and INR 32,000/t, respectively. The market is witnessing limited demand for both semi-finished and finished steel. According to reliable sources, due to the constrained demand in finished steel, some mill owners are offering rebar at INR 46,000/t for various projects.

Price highlights

End-cutting and billets spread: In Mandi, the end-cutting scrap and billets spread was at INR 5,000-5,500/t.

Domestic Vs imported scrap: Imported melting scrap prices at Nhava Sheva Port were at around $394-$397/t, which equates to approximately INR 35,210/t(including freight),while local scrap-HMS (80:20)-prices in Mumbai stood at INR 33,000/t stable d-o-d.

In India, the demand for imported scrap continued to be subdued due to the disparity between offers and bids, resulting in the absence of any firm offers or bids today. Indicative offers for shredded scrap from Europe were appraised at $410-$415/t CFR Nhava Sheva.

Raipur sponge iron-billet spread: The current conversion spread (margin) from pellet-based DRI (P-DRI) to steel billets in Raipur stood at INR 13,150/t.

To see SteelMint's melting scrap assessment, pricing methodology and specification documents, Click here

To provide feedback on this index or if you would like to contribute by becoming a data partner, please contact - info@steelmint.com.