India: BF-grade coke prices steady w-o-w; import parity and stable steel output support market

...

- Domestic BF-grade coke prices remain stable

- Australian coking coal prices ease w-o-w

India's blast furnace (BF)-grade metallurgical coke prices remained stable week-on-week (w-o-w) as of 16 April 2026, reflecting balanced market fundamentals.

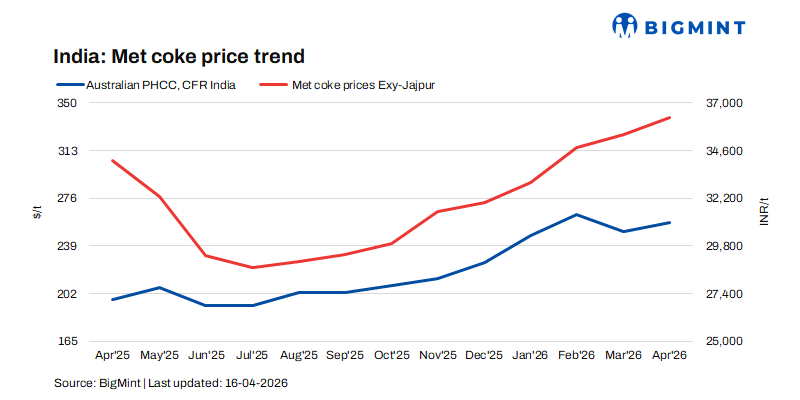

According to assessments by BigMint, BF-grade coke (25-90 mm) prices in eastern India held steady at INR 36,400/t ex-Jajpur, while western India prices remained unchanged at INR 33,500/t ex-Gandhidham. In the foundry segment, +90 mm foundry-grade coke prices also remained stable at INR 36,400/t ex-Rajkot, indicating limited volatility across key consuming regions.

Import parity supports domestic price floor

Import parity continues to underpin domestic coke prices. Indonesian-origin BF coke (65/63 CSR) was assessed at $288/t CFR India, up marginally by $1/t w-o-w. Despite the slight correction, import prices remain sufficiently elevated to maintain a firm floor for domestic coke values, limiting the possibility of a sharp price decline in the Indian market.

Australian coking coal prices drop w-o-w

On the raw material front, Australian premium hard coking coal (PHCC) prices eased marginally by $5/t w-o-w to $231/t FOB, providing only limited cost relief to coke producers. The earlier rally in coking coal prices continues to influence coke production costs, thereby supporting the current price stability in the domestic coke market.

Meanwhile, China's domestic coking coal market remained largely stable during the week. Coal mine supply stayed normal, while spot prices showed minor corrections amid cautious procurement and limited new orders from downstream coke and steel producers. Despite this, coking plants maintained high operating rates and healthy margins, supported by strong steel production and elevated blast furnace utilisation. As a result, inventories at coking plants remained relatively low.

At Chinese ports, spot coking coal prices strengthened slightly, while freight rates remained weak. Additionally, Chinese coke producers have proposed a second round of price increases, though steel mills have yet to respond, keeping the market in a negotiation phase.

Downstream pig iron prices soften

In the downstream segment, steel-grade pig iron prices in Durgapur declined by INR 450/t w-o-w to INR 40,600/t ex-works, indicating a slight moderation in demand. Supporting this trend, Steel Authority of India Limited Bokaro Steel Plant auctioned 3,500 t of steel-grade pig iron on 8 April 2026, with the entire quantity booked at an average price of INR 38,900/t.

Similarly, NMDC Limited's Nagarnar Steel Plant auctioned 7,000 t of steel-grade pig iron on 15 April, with the full quantity sold at the base price of INR 38,000/t. Bids declined by INR 200/t compared to the 9 April auction, reflecting slightly subdued demand conditions and a mild price correction in the pig iron segment.

Outlook

In the near term, India's BF-grade coke prices are expected to remain stable with a slight firm bias. Elevated import parity levels and relatively firm coking coal costs are likely to support domestic prices, while steady blast furnace operations at steel mills will continue to sustain demand. However, softness in pig iron prices and cautious downstream buying may restrict sharp upward movements, keeping the market largely range-bound in the short term.