India: Auto sector surges in 5MCY'26; passenger vehicle sales jump 18% y-o-y

...

- Rural income recovery supports two-wheeler demand

- Passenger vehicles lead industry surge amid robust rural demand

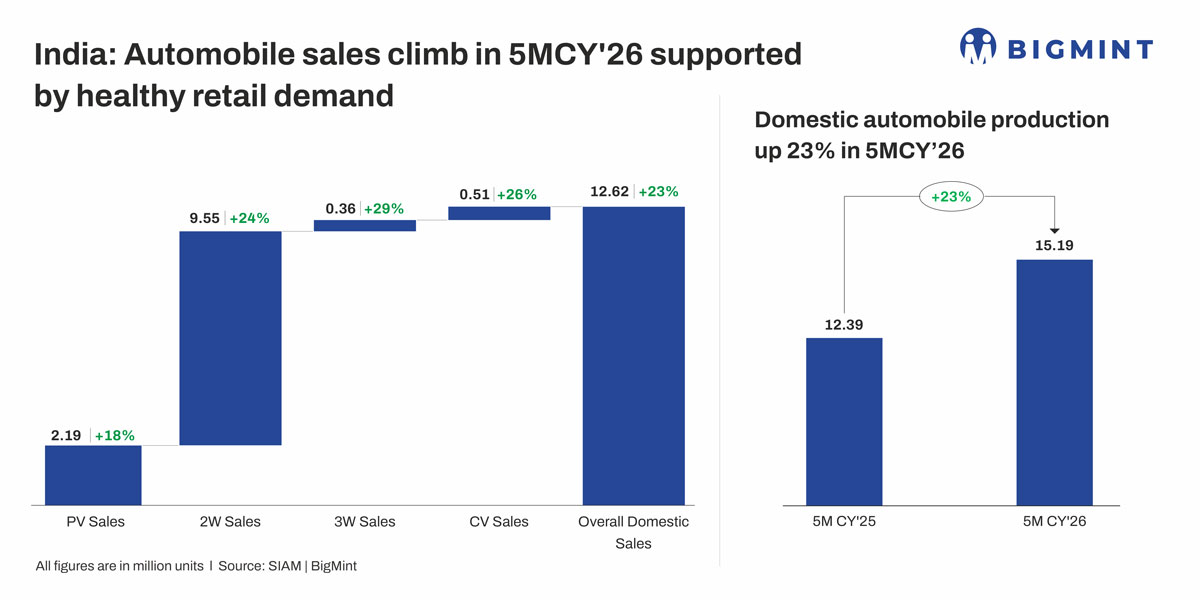

India's automobile sector recorded strong growth in 5MCY'26, according to SIAM data, supported by healthy performance across all major segments. Passenger vehicle sales increased 18% y-o-y to 2.19 million units from 1.86 million units in 5MCY'25, while two-wheeler sales rose 24% to 9.55 million units from 7.68 million units. Three-wheeler sales also grew 29% to 0.36 million units from 0.28 million units.

Commercial vehicle sales increased 26% y-o-y to 0.51 million units from 0.41 million units. Overall domestic automobile sales rose 23% to 12.62 million units from 10.23 million units, while total automobile production also increased 23% to 15.19 million units from 12.39 million units in 5MCY'25.

Retail automobile sales rise 17% y-o-y in 5MCY'26

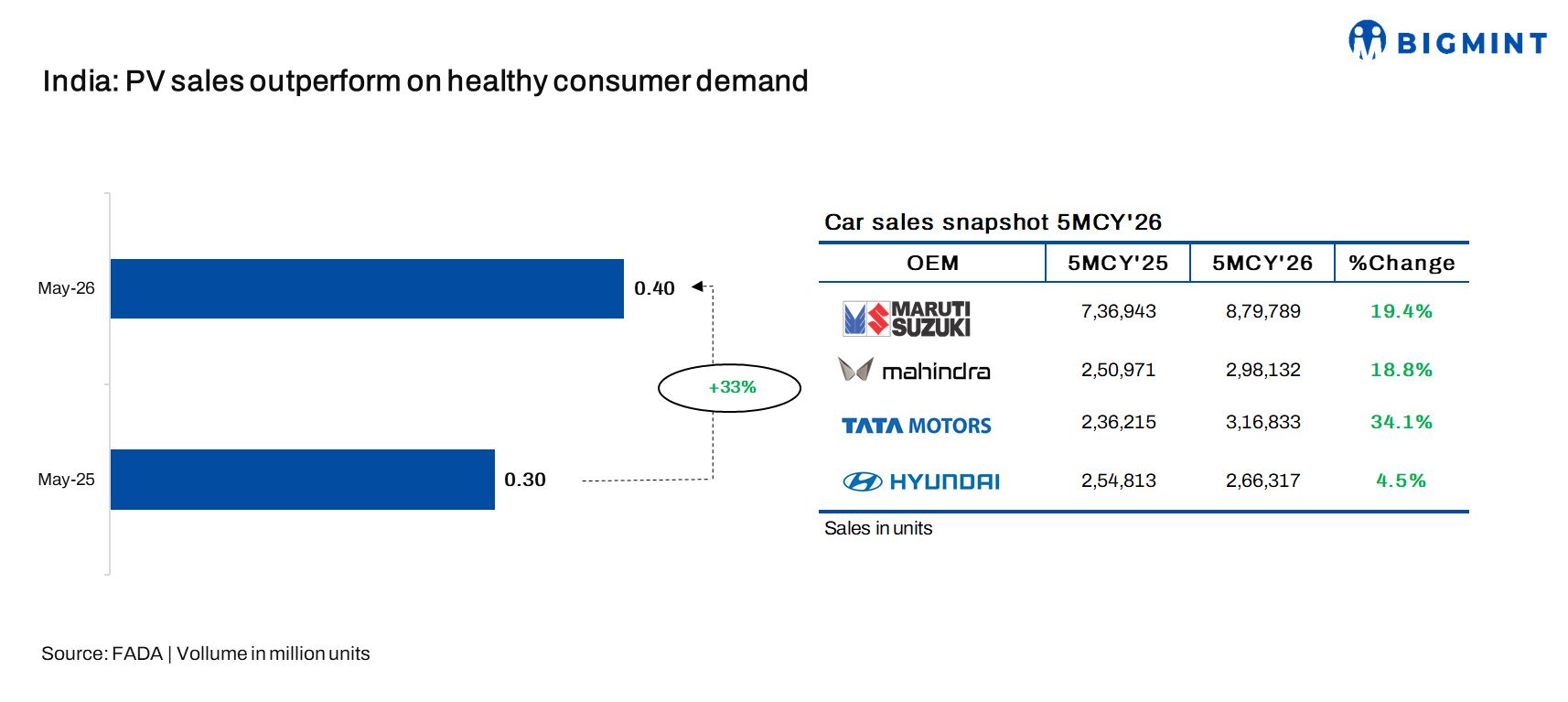

Meanwhile, FADA's retail data for 5MCY'26 reflected healthy y-o-y growth across all vehicle segments. Passenger vehicle sales increased 22% to 2.16 million units from 1.77 million units in 5MCY'25, while two-wheeler sales rose 20% to 9.27 million units from 7.73 million units. Three-wheeler sales also grew 13% to 0.57 million units from 0.50 million units.

Commercial vehicle (CV) sales increased 11% to 0.50 million units from 0.45 million units, while tractor sales rose 21% to 0.44 million units from 0.37 million units. Overall retail sales increased 17% to 12.94 million units from 11.05 million units, indicating broad-based growth across segments.

Indian auto retail market remains resilient amid seasonal challenges

Commenting on the May retail performance, FADA President C S Vigneshwar said that despite challenges, including above-normal heatwave conditions, higher fuel prices, and geopolitical tensions in West Asia, India's automobile retail market maintained a strong growth trajectory, recording the best-ever May registrations across passenger vehicles, three-wheelers, tractors, and overall vehicle sales. He noted that the industry's resilience reflects healthy underlying demand, although m-o-m sales moderated due to the usual post-April seasonal slowdown and the delayed southwest monsoon, which kept much of the country in the pre-sowing phase.

In the two-wheeler segment, retail demand was supported by marriage-season purchases, steady commuter demand, and continued affordability, particularly in rural markets. However, extreme summer temperatures reduced showroom footfall in several regions, while selective supply constraints limited sales momentum. Dealers also reported rising consumer interest in fuel-efficient and alternative powertrain vehicles following the May fuel-price revision, resulting in a notable increase in electric two-wheeler adoption.

Commercial vehicle sales remained supported by healthy freight movement, e-commerce logistics, and replacement demand, with rural markets outperforming urban regions. Growth was led by light commercial vehicles, reflecting robust last-mile transportation demand. However, dealers highlighted longer financing approval timelines, rising freight and insurance costs linked to geopolitical developments in West Asia, and cautious buyer sentiment as key challenges.

Passenger vehicles emerged as the strongest-performing segment, driven by robust rural demand, a revival in entry-level car sales, sustained SUV demand, healthy booking pipelines, and new model launches. Demand for CNG and electric vehicles also strengthened, lifting the share of alternative fuel vehicles above 38% during the month. However, Vigneshwar cautioned that passenger vehicle inventory levels increased to 31-33 days by the end of May, exceeding FADA's recommended 21-day benchmark. He urged OEMs to maintain disciplined wholesale dispatches during the seasonally weaker June period to ensure inventory remains aligned with retail demand.

Impact on aluminium ADC12 alloy

India's ADC12 aluminium alloy market remained supported by steady demand from the automobile sector, driven by its extensive use in automotive die-casting applications and sustained production across passenger vehicles, two-wheelers, and commercial vehicles.

However, in June 2026, prices declined as strong buyer resistance to elevated domestic offers coincided with a shift toward more competitively priced imports from Malaysia and Thailand under FTA advantages, which were lower by around INR 20,000-30,000/t. Sentiment was further weighed down by a downward revision in settlement prices by a leading automaker, prompting softer offers across regions.

While suppliers in southern India quoted INR 370,000-373,000/t and Delhi-Pune levels were at INR 365,000-367,000/t, aggressive negotiations and cautious buying kept transaction levels subdued, with bids ranging between INR 360,000-370,000/t, sustaining pressure on spot prices.

Outlook

Looking ahead to June, FADA expects India's automobile retail market to remain resilient, supported by the timely progress of the southwest monsoon, early Kharif sowing activities, improving rural cash flows, and the tail-end of the marriage season. Dealer sentiment remains positive, with over half of dealers expecting sales growth, while nearly 40% anticipate stable market conditions. The Reserve Bank of India's decision to maintain the repo rate at 5.25% is also expected to support financing conditions and consumer demand.

The two-wheeler segment is likely to benefit from improving rural incomes and rising consumer preference for fuel-efficient and electric vehicles. However, persistent heatwave conditions and elevated fuel prices could continue to impact showroom footfall in some regions. Passenger vehicle sales are expected to remain supported by healthy booking pipelines, strong demand for electric vehicles, and new model launches, despite the typical seasonal moderation witnessed during June. Meanwhile, commercial vehicle demand is projected to remain stable, underpinned by steady freight movement and infrastructure-led activities. However, higher logistics costs arising from geopolitical tensions in West Asia, along with fuel price movements, remain key risks for the sector.

With reference to the June-August period, dealer confidence strengthens further, with nearly 60% of dealers expecting market growth as monsoon activity gathers pace and agricultural operations accelerate. Improving rural sentiment, stronger farm incomes, and continued adoption of fuel-efficient and alternative powertrain vehicles are expected to support two-wheeler demand. Passenger vehicles are likely to maintain healthy momentum ahead of the festive season, aided by new product launches and expanding demand from rural and semi-urban markets. Commercial vehicles are also expected to benefit from sustained economic activity, goods transportation, and infrastructure spending, although financing turnaround times and geopolitical uncertainties remain key factors to monitor.

Overall, FADA maintains a cautiously optimistic outlook for the coming quarter, supported by favourable monsoon progress, healthy rural fundamentals, a strong 7.7% GDP growth in FY'26, and continued policy stability. While seasonal softness may persist in the near term, the industry is expected to transition towards stronger demand during the second quarter as rural incomes improve and economic activity gathers momentum.