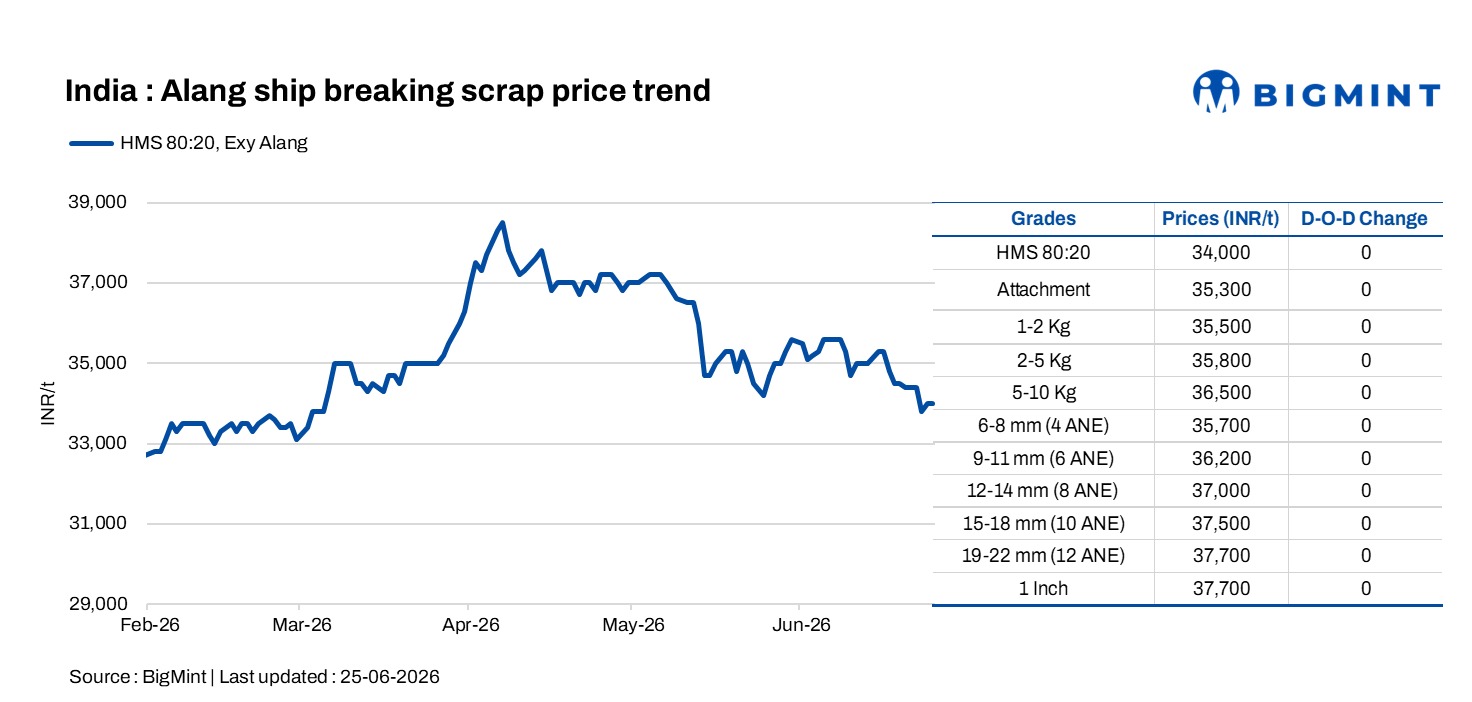

India: Alang ship-breaking scrap prices remain stable d-o-d

...

- Alang HMS (80:20) prices assessed at INR 34,000/t ex-yard

- North Indian steel markets witness billet, rebar, scrap price gains

Ship-breaking scrap sentiment in Alang remained stable on 25 June, with HMS (80:20) prices holding at INR 34,000/t ex-yard. While the broader ferrous value chain in western India continued to face downward pressure, improving trends in northern steel markets helped support overall market sentiment.

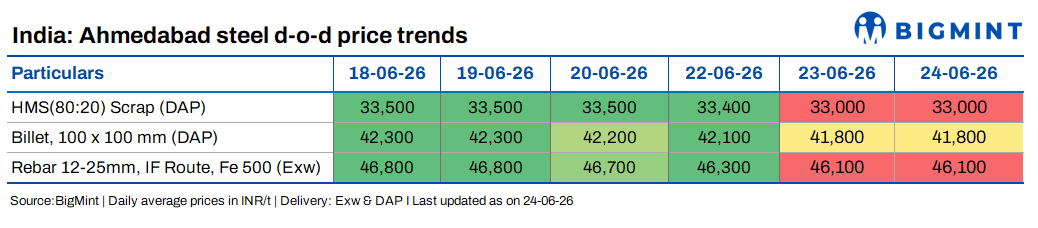

In Gujarat's Bhavnagar, billet prices declined by INR 200/t day-on-day (d-o-d) to INR 41,300/t DAP, reflecting subdued demand from downstream buyers. Ahmedabad rebar prices were unchanged at INR 46,100/t ex-works, indicating limited momentum in the regional finished steel market.

However, market conditions were comparatively stronger in northern India. Billet prices in Mandi Gobindgarh increased by INR 300/t d-o-d to INR 42,950/t DAP, while rebar prices rose by INR 100/t to INR 47,500/t ex-works. Supporting this trend, HMS scrap prices in Mandi Gobindgarh increased by INR 300/t to INR 35,100/t DAP.

The rise in scrap prices was attributed to improved buying activity across both semi-finished and finished steel segments. Stronger procurement interest prompted scrap suppliers to revise offers upward, reflecting a recovery in sentiment across the secondary steel value chain. Nevertheless, market participants noted that end-user demand remains inconsistent, keeping buyers cautious despite recent price gains.

In Alang, procurement activity from the induction furnace mills largely remained need-based, with most consumers continuing hand-to-mouth purchasing strategies amid uncertain steel demand fundamentals. As a result, local scrap prices remained stable despite the positive cues emerging from northern markets.

Bangladesh market overview

Chattogram's ship recycling market remained firm this week, supported by stable steel plate prices of around BDT 65,000/t ($529/t) and healthy underlying demand. Although monsoon conditions in the Bay of Bengal continued to disrupt beaching activity and restrict vessel arrivals, strong plot occupancy levels and an active letter of credit (LC) pipeline sustained positive market sentiment.

Additionally, the reopening of the Strait of Hormuz and easing freight rates improved expectations regarding vessel availability, potentially supporting higher recycling activity in the coming months.

Outlook

The divergence between western and northern Indian steel markets highlights differing demand conditions across regions. While Alang recyclers continue to face cautious buying from local mills, improving billet, rebar and scrap prices in northern markets could provide support to ship-breaking scrap sentiment if secondary steel demand remains firm through early July.