How will Jakarta's new nickel ore policy reshape global stainless steel markets?

...

- Indonesia raises nickel ore pricing benchmark

- Nickel supply tightened by lower mining quotas

Indonesia implemented a new Mineral Benchmark Price (Harga Patokan Mineral, or HPM) pricing formula for nickel ore on 15 April. The policy, part of Jakarta's long-term strategy to control nickel supply, raise prices, and boost state revenue from the mineral sector, is set to fundamentally reshape the global stainless steel industry, Mysteel Global notes. The change will drive up production costs, accelerate capacity concentration in Southeast Asia, and force structural adjustments in China's stainless steel sector.

Policy background

Under Ministerial Decree No. 144.K/MB.01/MEM.B/2026, Indonesia's Ministry of Energy and Mineral Resources (ESDM) has raised the correction factor (CF) for 1.6% grade nickel ore from 17% to 30%. For every 0.1% increase or decrease in nickel grade, the CF will decrease or increase by 1%, respectively, as Mysteel Global has reported.

The revised HPM also incorporates values for associated minerals including cobalt, iron and chrome for the first time. Cobalt content of 0.05% or above will be included with a CF of 30% and subject to a 2% tax. The CF for iron content is also set at 30%, and 10% for chrome content. The pricing unit has also been standardized to US dollars per wet metric tonne. The HPM serves as the mandatory floor price for domestic nickel ore sales and the base for royalty calculations.

Notably, on February 10 ESDM unveiled its Nickel Work Plan and Budget (RKAB) for the year, setting the approved nickel ore production quota for 2026 at between 260-270 million wmt, further tightening supply expectations even before the HPM revision took effect.

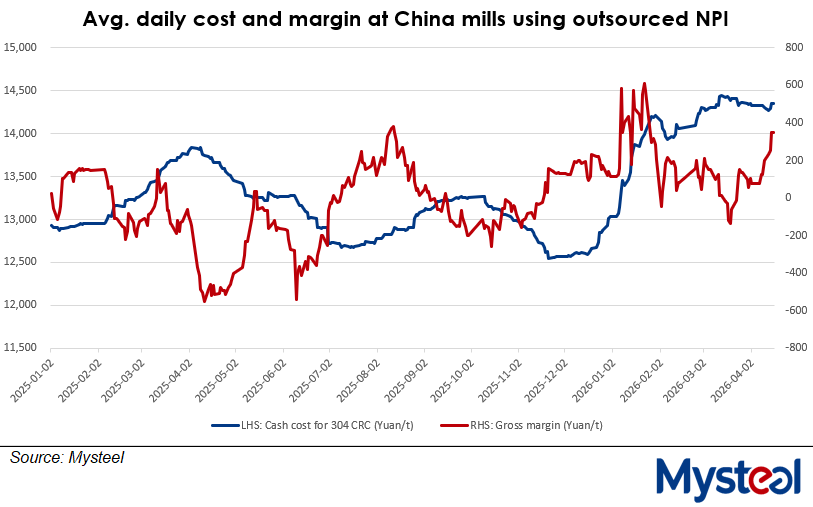

Higher mill costs and squeezed trader margins

As of April 16, the most-traded nickel contract on the Shanghai Futures Exchange closed at Yuan 142,270/tonne ($20,856/t), up 6.7% from a week earlier, signaling broad market anticipation of tighter nickel supply after the new HPM policy took effect.

The new HPM for nickel ore will push Indonesian spot ore prices higher, a factor that will raise global pricing floors in turn, Mysteel Global suggests. Global stainless steel mills that rely on smelted nickel products made from imported Indonesian ore, particularly small- and medium-scale producers, will bear the brunt with costs seen increasing 5-8%, according to a Mysteel analyst.

The mills will endeavor to pass along their higher input costs to customers. Consequently, trading companies worldwide will face higher procurement costs for stainless steel but will struggle to pass them on quickly to end-users, squeezing their profits in turn.

Capacity concentration and trade flow realignment

As higher Indonesian ore prices become the new normal, prices for nickel feeds such as nickel pig iron (preferred by Chinese stainless makers), ferronickel or nickel matte will also move higher. In response, global prices for 300-series stainless steel are expected to rise 8-12% over the next 12 to 18 months, the analyst predicts.

In this scenario, profit margins among integrated stainless mills in Indonesia will expand due to their cost advantage, and this will translate to accelerated capacity expansion in the country.

In contrast, margins of mills based in China and India that rely heavily on smelted nickel products made from imported Indonesian ore will weaken. In response, these mills are expected to reduce 300-series production that requires higher nickel content input, and shift to produce more 200-series and 400-series products.

Global stainless demand is expected to grow at a slower pace. Higher end-product prices resulting from cost increases will dampen demand from sectors such as home appliances and architectural decoration. In particular, low-end products may be substituted by aluminum alloy and carbon steel products. However, high-end products such as food-grade and medical-grade stainless steel will remain relatively resilient due to lower price sensitivity.

Large-scale traders with regular mill clients will expand market share, while smaller traders lacking supply security and risk management ability will be forced out of the market. Trade flows will gradually realign toward Indonesia and Southeast Asia, as higher concentration boosts trading activities in these regions, the analyst explains.

End of low-cost era as Indonesia becomes new stainless production hub long-term

Over the long run, Jakarta's new policy will permanently lift global nickel ore pricing. As such, the global stainless steel industry's costs are expected to rise 10-15% on average, and mills will seek high-quality and high-value-added products to find a way out.

As Indonesia gradually becomes the world's primary stainless steel production hub, global trading companies will accelerate localization efforts in Southeast Asia. Meanwhile, demand growth in China and the EU will slow and pivot toward premium grades. In this context, a secondary stainless steel trade is expected to emerge as a new growth area, pushing trading companies toward greener supply chains.

Outlook for China

Looking ahead, the global stainless industry is bracing for higher costs while exploring higher quality and higher value-added products. Chinese mills will be persuaded to accelerate overseas nickel investments, expand high-end and secondary stainless production, and strengthen upstream-downstream collaboration. These measures will help manage cost volatility and market competition to ensure sustainable industry development.

This article is published as part of a content-exchange agreement between Mysteel and BigMint.