How will EU's reduced steel import quotas affect India and global steel trade - BigMint report

...

- India's flat steel export quota to EU cut sharply by 41%

- Higher EU steel production may lead to sharp drop in scrap exports

Data Deep Dive: In what has been described as a historic moment in trade and industrial policy, the European Union (EU) has announced new steel safeguard quotas, and country-specific steel import quotas, that are expected to reshape global steel trade.

Under its new Steel Regulation, the EU has reduced total tariff-rate quotas by around 47% from the previous safeguard regime while increasing the duty on out-of-quota imports to 50% from 25% for 26 steel products.

The EU has run a steel "safeguard measure" (tariff-rate quotas) since 2018, originally a response to US Section 232 tariffs diverting steel into the EU market. The recently adopted Steel Regulation is part of the EU's response to persistent global overcapacity in the steel sector, which remains a serious global problem and continues to distort international markets.

What is TRQ?

A tariff rate quota (TRQ) sets the volume of a product that can enter at a low/zero duty; anything above that volume faces a much higher "out-of-quota" tariff (often prohibitive, 50%).

A TRQ is often distinguished from an absolute quota (hard cap, no imports allowed beyond it), TRQs still allow imports beyond the cap, just at a punitive price.

Country-specific quotas

The EU allocates quotas partly by product category (25+ steel product categories: hot-rolled coil, cold-rolled, plates, rebar, wire rod, etc.) and partly by country-specific historical trade share, with a residual "other countries" pool for smaller suppliers.

Country-specific caps prevent any single large exporter (historically Turkiye, India, South Korea, pre-sanctions Russia and Vietnam) from dominating a category's quota. It is to be noted that some countries have lost country-specific allocations already (Russia's quota was reallocated/zeroed post-2022 sanctions in several categories).

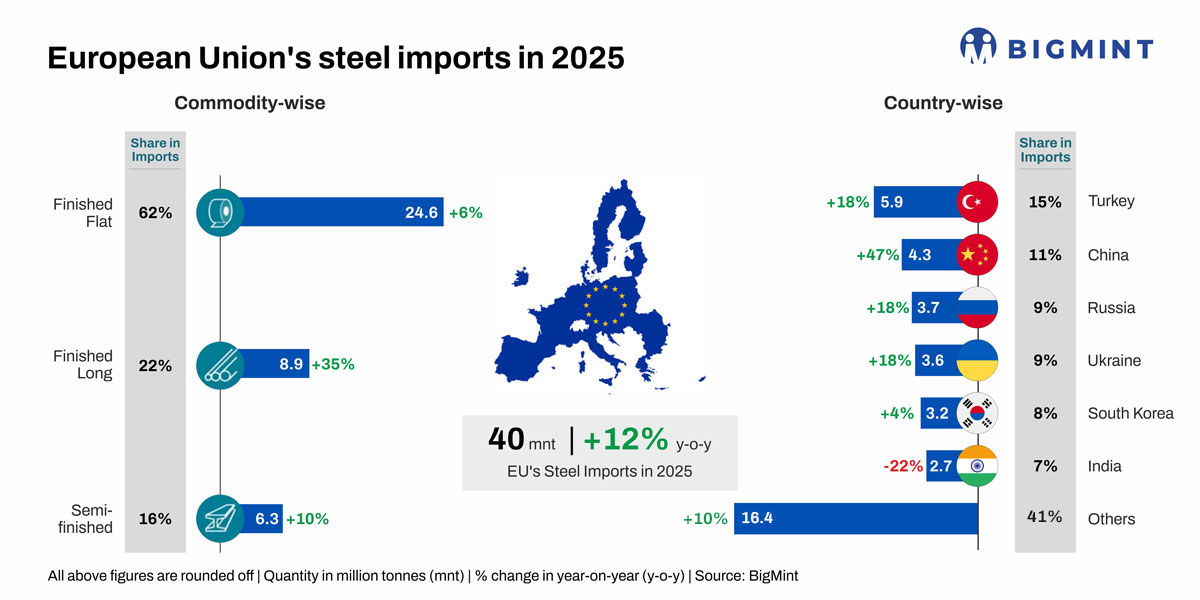

Around 80% of EU imports of steel come from FTA partners. Half of the EU's annual import quota, set at 18.3 million tonnes (mnt) by the Steel Regulation, has been reserved exclusively for preferential trading partners, with the remaining half available to all trading partners without discrimination, including FTA partners.

The EU has struck deals with countries with which it already has an FTA, allowing them to sell between 66% and 67% of their historic trade on average. The allocations can be adjusted if necessary if there are shortages in supply in particular types of steel.

How has India been affected?

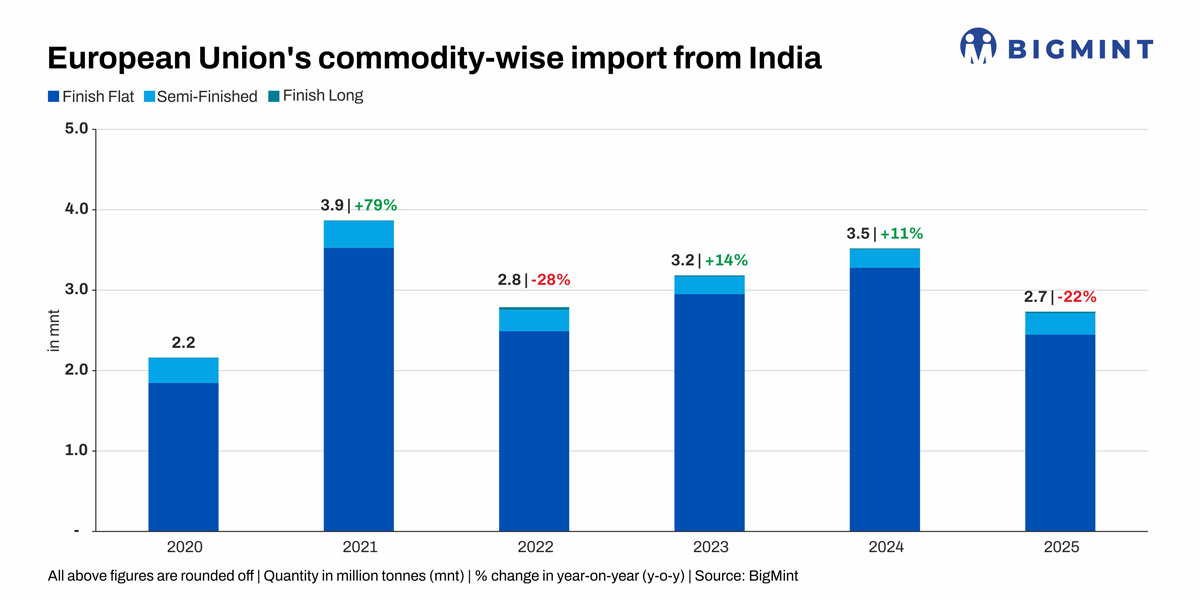

BigMint calculations show that India's quota allocation across five flat steel categories declined by 40.8%, from 2.4 mnt to 1.42 mnt. Incidentally, Indias imports to the EU are predominantly flats: India's flat steel export share stood at over 80% of total exports to the EU in 2025.

CRC saw the steepest decline among the major flat products, falling 58.8%. Metallic coated quotas were reduced by 66.8%. HRC quotas declined by 34%. Organic coated (Category 5) quotas fell by 31.1%. Metallic coated 4A was the only category to register an increase, rising 8.3%.

The tighter quota regime comes at a time when the EU continues to account for the largest share of India's steel exports. Indias finished steel exports of over 3 mnt to the EU in 2025 accounted for 12.3% of the continents total imports, as per BigMint data.

Impact on global market

EU steel industry & imports: The new quotas are designed not only to curb import surges but also to safeguard Europes steelmaking capacity and support decarbonisation, according to EUROFER. It paves the way for restoring up to 15 mnt of lost European steel production. Capacity utilisation of the European steel industry stands at approximately 65%.

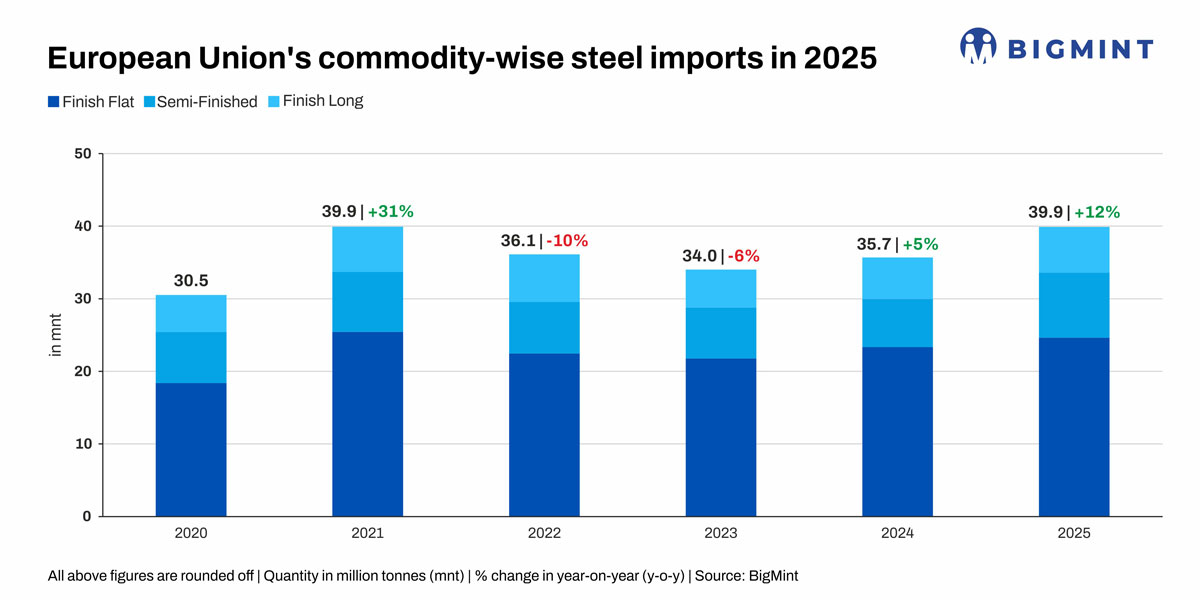

EUROFER data show that the EU's apparent steel consumption in 2025 was over 134 mnt, while domestic production trailed at around 126 mnt. Finished steel imports had a share of over 18% of the EU's total consumption.

A direct effect of the new regulation will be a corresponding contraction in steel imports by the EU. Our projections show that imports into the EU are likely to drop 15-20% y-o-y in 2027.

Declining scrap exports: Another direct impact relates to the prospective decline in steel scrap exports by the EU, one of the largest suppliers in the world. Tighter import quotas will effectively prop up domestic steel production in the EU and, consequently, lead to lower exports of scrap from the EU.

This will deal a direct blow to emerging economies like India that are witnessing a rapid surge in steelmaking capacity but are deficient in domestic scrap and highly dependent on imports. Data show that the EU's scrap exports declined 13% y-o-y to over 16 mnt in 2024 and remained flat at around 16.6 mnt in 2025, down from 19.4 mnt in 2021.

This declining trend is likely to continue amid lower steel imports and higher domestic steel production in the EU, as well as policies like the waste shipment regulations that directly discourage scrap exports.

Possible hike in imports of semis: A likely fallout of the tightening of steel safeguard quotas by the EU could be the hike in imports of semi-finished steel (slabs/billets) by downstream users.

With quotas tightening, demand for semis might increase as these products typically face lighter treatment in safeguard categories than finished flat products. EU re-rollers/finishers may lean more on imported slab to feed finishing lines while quota on finished product tightens, a classic safeguard workaround as seen in past steel trade cases.

In 2025, the EU significantly raised its imports of semis. Total imports of slabs and square billets reached 8.91 mnt, an increase of 35% y-o-y, the highest in recent years. For comparison: in 2024, semis imports amounted to 6.62 mnt. The surge in imports is mainly attributed to efforts by EU producers to minimise costs amid a sharp surge in energy costs and overall economic inflation.

Russia hit hardest: Russian steel already faces sanctions-related exclusions/reduced quotas in many categories since 2022; a further 47% cut compounds an already marginalised position. BigMint data show that Russian exports of finished steel to the EU fell precipitously from over 3 mnt in 2021 to just 0.01-0.02 mnt in 2024-25.

This has had a direct fallout: the sharp deceleration in Russian crude steel production, which fell to a 15-year low in 2025, as per worldsteel data.

Russian exporters are likely to redirect further toward Asia (China, India, and neighbouring markets), Middle East, and Africa, adding supply pressure in these markets and possibly impacting prices.

Low-emissions producers to benefit: Because the EU-CBAM's carbon cost applies on top of whatever volume/tariff regime governs the QR, exporters with cleaner production (lower embedded carbon per tonne) face a smaller effective cost stack.

The likely relative winners will be countries with cleaner grids/newer EAF or DRI capacity. Among these countries, the top beneficiaries will be Turkiye, countries such as Canada, and those in the Gulf that are setting up renewable-powered grid and DRI capacity based on low-carbon fuels.

India and China's coal-heavy BF-BOF-heavy steel mix would face a double hit (quota exposure + high CBAM cost). Therefore, these top steel producing countries, with average CO2 intensity of production between 2.2 and 2.5 tco2/t of steel, will be the most directly affected.

Outlook

High EU-ETS costs and energy inflation have already affected steel production in the EU, as evidenced by the slump in steel industry capacity utilisation and the gradual decline in crude steel production. EU crude steel production dropped from around 160 mnt in 2016-2017 to less than 126 mnt in 2025. Narrowing imports may just squeeze the downstream industries harder and push steel prices higher.

Therefore, the inflation-related threat to industry in the EU remains, although domestic steel production in the EU will receive a boost much like that in the US where Sec. 232 tariffs have had a beneficial impact on domestic production.

For Indian producers, the challenge is no longer securing access to the EU but remaining competitive within a substantially smaller import quota, while simultaneously managing CBAM-related costs. With HRC exports facing the greatest pressure, mills are likely to focus on protecting established customer relationships in Europe while seeking incremental growth in alternative export markets, particularly Vietnam and the Middle East.