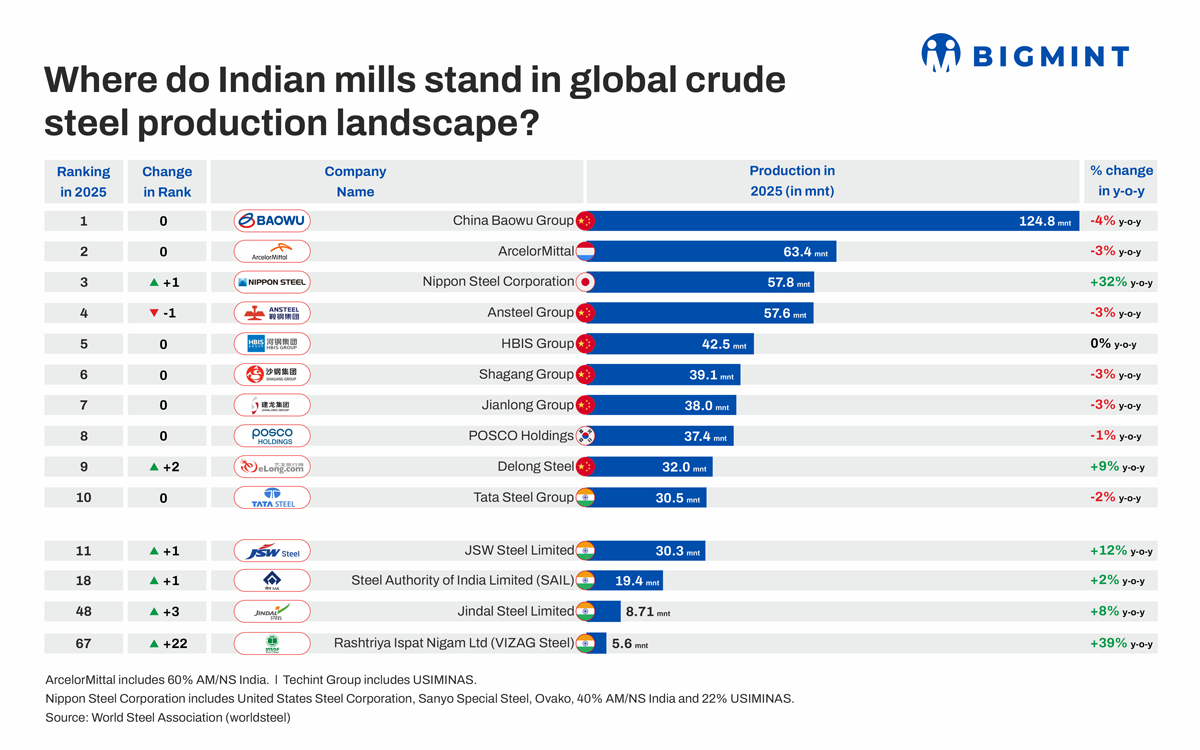

How did leading global steel producers fare in CY'25?

...

- 21 out of 33 largest Chinese steel producers record drop in output

- Nippon Steel rises to 3rd spot after successful acquisition of US Steel

- Tata remains 10th largest producer, other Indian mills ascend ranking ladder

Morning Brief: The World Steel Association's global steel producers' rankings underwent significant shifts in CY'25, as several Chinese producers reported lower output and slid down the hierarchy amid persistent weakness in the country's property sector and efforts to rationalise capacity.

On the other hand, Nippon Steel's output increased sharply as its acquisition of US Steel finally went through. Additionally, Indian and US producers gained ground, as crude steel production from both countries climbed up amid significant demand growth and protection from mounting imports.

Notably, crude steel production by the top 10 global steel producers, representing around one-third of global output, stood at 518 mnt, down by 1% y-o-y. This broadly coincides with the 2% drop in global production.

However, it should be noted that the decline would have been slightly sharper had the Nippon Steel-US Steel deal remained in limbo. Besides Nippon Steels 32% y-o-y surge, only HBIS Group recorded 0.4% growth, and Delong Steel raised its output by 9%; all other companies recorded declines of 1-4%.

Key highlights

Chinese producers remain dominant but face pressure: Chinese companies accounted for 33 of the 77 listed overall, indicating overwhelming representation among the world's largest steelmakers. However, production trends point to a broad-based slowdown, with around 21 recording a drop in output and 15 sliding down the rankings.

India strengthens its global position: India's leading steelmakers continued to gain ground, supported by capacity expansions and robust domestic steel consumption. Tata Steel remained the 10th largest, though production dipped. JSW Steel climbed up to 11th, after recording one of the strongest growth rates of 12% y-o-y. State-owned SAIL also climbed up by one spot to 18th, while Jindal Steel rose to 48th from 51st. Rashtriya Ispat Nigam Ltd (VIZAG Steel) jumped 22 places to 67th.

US-based producers gain: Most US steelmakers improved their standing in the global rankings, having recorded higher output y-o-y. Nucor increased crude steel production by 8% but remained stable at 16th, while Cleveland-Cliffs expanded output by 6% and moved up to the 22nd.

Previously, in CY'24, before its acquisition by Nippon Steel, US Steel had been the 29th largest steelmaker and the 3rd largest in the US.

Fewer steelmakers cross 3 mnt threshold: The number of companies producing more than 3 mnt of crude steel annually and qualifying for the global ranking fell to 77 in 2025 from 104 in the previous year.

The sharp reduction suggests that production is increasingly consolidating among larger steelmakers, while smaller and mid-sized producers are finding it more difficult to maintain output above the reporting threshold amid weaker demand, tighter margins, and growing competitive pressures.

China Baowu Group retained its position as the world's largest steelmaker, but production declined by 4% y-o-y. The fall reflects broader weakness in China's property sector and slower infrastructure and manufacturing momentum relative to previous years.

ArcelorMittal's output declined by 3%amid continued weakness in the EU, where manufacturing activity and steel demand remained subdued. Rising imports into Europe and weak industrial demand weighed on utilisationrates. The company's ranking remained unchanged at second globally.

Nippon Steel recorded by far the largest increase of around 32%, among the top 10 producers, with the jump being primarily acquisition-driven following the inclusion of US Steel Corporation in consolidated figures. This is less a reflection of underlying Japanese demand growth, which remains subdued due to the US tariffs and an uncertain manufacturing outlook.

State-owned Ansteel (-3%) slipped from third to fourth place as Chinese steel demand remained under pressure. However, HBIS maintained its position at fifth, beingone of the few large Chinese producers to post growth, albeit marginal. Additionally,whileboth Shagang Group, China's largest privately owned steelmaker, and Jianlong Group, the largest privately owned enterprise in Tangshan, Hebei, recorded declines of 3% y-o-y, both remained at sixth and seventh, respectively.

POSCO's output remained relatively stable, dipping by 1%. South Korea's steel sector benefited from automotive and shipbuilding demand, which helped offset weakness in construction and manufacturing.

Delong Steel recorded a 9% increase in output, moving up by two spots to ninth place. It was one of the few Chinese steelmakers to lift its output.

Tata Steel remained India's highest-ranked producer despite a modest 2% decline. The fall was largely influenced by weaker European operations, with the Port Talbot facility shut for its transition into an electric arc furnace from a blast furnace.

Outlook

Future changes in the global steel hierarchy are likely to be increasingly driven by divergences in regional demand trends, which will naturally influence capacity additions and operating rates.

China is likely to remain home to the world's largest steelmakers for the foreseeable future, but the country's influence on global production growth is diminishing. Worldsteel expects Chinese steel demand to contract by a further 1.5% in CY'26, so the downtrend in rankings is expected to continue.

With India remaining the world's fastest-growing major steel market, we may see more Indian producers gaining ground. JSW Steel could enter the top 10, following the restart of BF-3 at Vijayanagar. However, there may be some volume loss from the transfer of Bhushan Power and Steel Ltd. (BPSL) to JSW-JFE Steel Ltd. in March 2026. The ramp-up of the Kalinganagar facility in Odisha and the newly commissioned EAF in Ludhiana, Punjab, is also set to boost Tata Steel's production in CY'26.

US crude steel production rose 7% during January-April 2026, with demand projected to grow at a more modest 1.7% in CY'26. This should help maintain the position of leading producers such as Nucor and Cleveland-Cliffs within the global rankings.

Meanwhile, producers in emerging steelmaking centres such as Turkiye and Vietnam could continue climbing the rankings. Crude steel production in Turkiye and Vietnam increased by 6% and 8%, respectively, in the first four months of 2026. Companies such as Tosyali Holding and Hoa Phat Steel were among the fastest-rising producers in the latest ranking, facilitated by rapid capacity expansions.

Russia presents a contrasting picture. Although six Russian companies remain in the CY'25 ranking, with steelmakers such as Metalloinvest, EVRAZ, and Severstal increasing output, production trends point to a more challenging environment in CY'26. Russia's crude steel output declined 12% y-o-y during January-April 2026 amid weaker domestic steel consumption and constrained export opportunities. These steelmakers could also move down the ranking in that case.