How did Indian steel industry perform in FY'26?

...

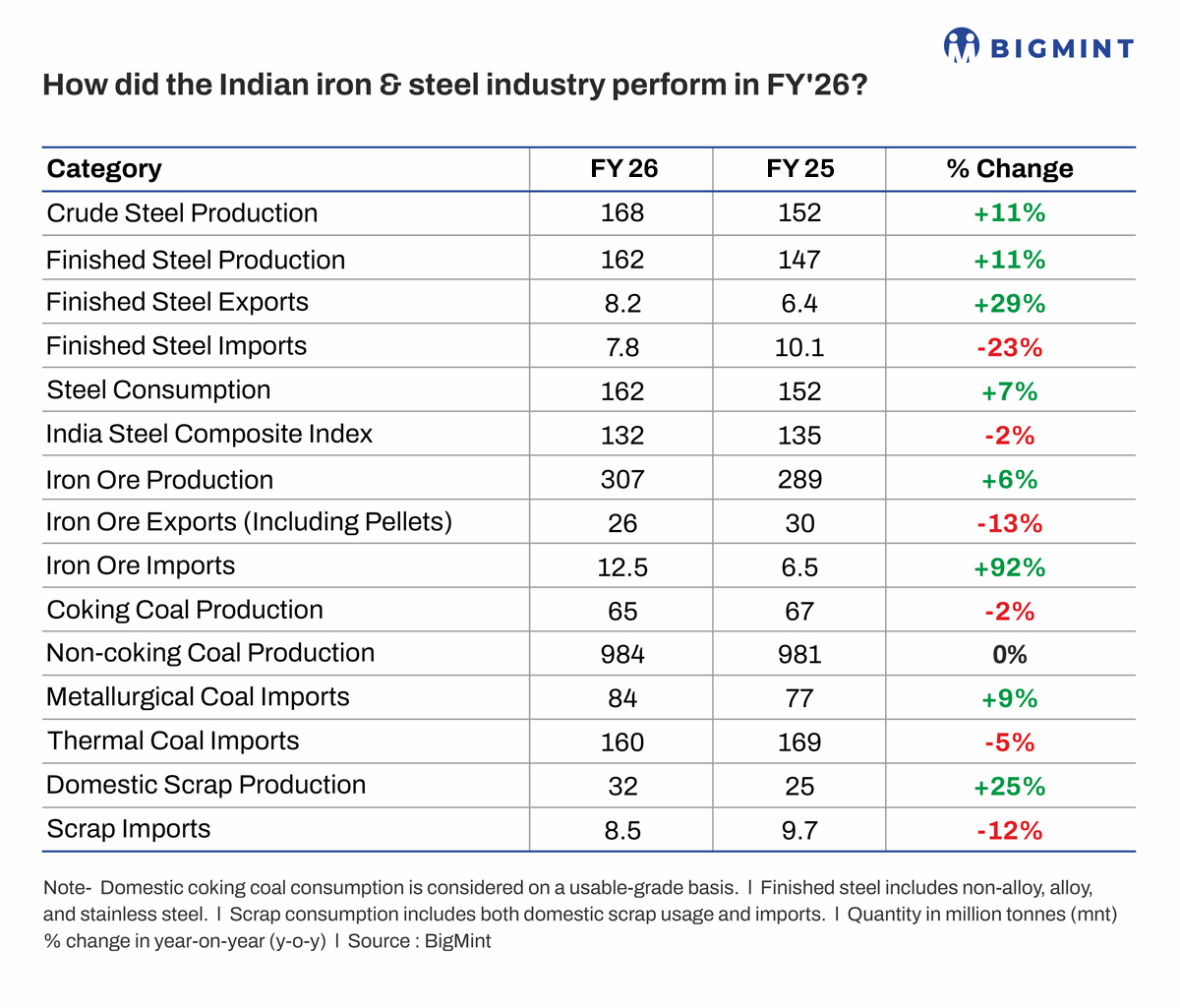

- Crude steel production rises 10.5% y-o-y to 168 mnt

- Finished steel exports rebound 28.7%, imports decline 22.8%

- India Steel Composite Index declines 2.2% y-o-y on continued price pressure

Morning Brief: India's steel industry maintained a strong growth trajectory in FY'26, supported by infrastructure-led demand and ongoing capacity additions across major producers. However, demand growth moderated during the year even as production continued to expand steadily, leading to emerging imbalances in the domestic market.

Pricing remained under pressure despite an improvement in trade dynamics, with the India Steel Composite Index averaging 132 in FY'26 compared to 135 in FY'25, indicating limited absorption of incremental supply. While weak global market conditions continued to influence pricing trends, domestic market dynamics remained the primary driver.

Overall, FY'26 reflects a phase where growth persisted, but the divergence between production, demand and pricing became more pronounced, alongside increasing reliance on imported raw materials.

Production growth moderates; route dynamics remain stable

Crude steel production in India increased by 10.5% y-o-y to 168 mnt in FY'26, marking continued capacity-led growth, albeit at a more measured pace compared to the sharper expansion seen in the previous fiscal.

The increase in output was supported by sustained capacity additions and stable utilisation levels across primary producers. However, the divergence between production growth and relatively slower demand expansion indicates that a portion of incremental output was either exported or absorbed into inventories.

Route-wise, the BF-BOF segment continued to account for a significant share of overall production, supported by integrated steelmakers operating at steady utilisation levels. At the same time, the induction furnace (IF) route remained a key contributor to incremental volumes, driven by its flexibility and cost competitiveness, particularly in the long products segment.

The electric arc furnace (EAF) route also maintained a stable contribution, supported by improved domestic scrap availability, although its share in total output remained relatively unchanged.

Trade rebalancing supports market stability

Indias finished steel trade dynamics improved markedly in FY'26, with exports increasing by 28.7% y-o-y to 8.24 mnt. Finished steel, which includes flat products such as hot rolled coils (HRC), cold rolled coils (CRC), plates and coated products, as well as long products including rebar, and wire rod, along with stainless steel, recorded a recovery in export volumes during the year.

Imports declined by 22.8% y-o-y to 7.8 mnt, reflecting the impact of the 12% safeguard duty on flat steel imports, along with a narrowing price differential between imported and domestic material.

As a result, India moved close to a net exporter position, marking a clear shift from the earlier phase of elevated import dependence. This rebalancing in trade flows also helped absorb part of the excess supply arising from production outpacing consumption, with exports providing an outlet for incremental volumes and lower imports reducing competitive pressure in the domestic market.

However, despite this improvement, the support from trade dynamics was not sufficient to offset broader supply-demand imbalances and weak global pricing trends, which continued to weigh on domestic steel prices.

Composite index softens amid supply-demand imbalance

BigMints India Steel Composite Index, a barometer of domestic finished steel prices, averaged 132 in FY26 compared to 135 in FY'25, reflecting a 2.2% y-o-y decline. While the decline was milder than the sharper correction seen in the previous year, indicating some easing of import-led pressure, domestic prices remained constrained by the imbalance between supply growth and demand absorption. Lower imports and improved trade balance provided partial support, but this was insufficient to offset the impact of elevated supply and weak global benchmarks.

Flat steel prices continued to face pressure from global markets, particularly amid subdued international demand, while the longs segment remained relatively better supported by infrastructure-led demand and limited direct exposure to imports. As a result, pricing remained range-bound through much of the fiscal, constraining margins across the sector.

Steel raw materials landscape

Iron ore: Iron ore production increased by 6.2% y-o-y to 307 mnt in FY26, but this growth lagged behind the pace of steel output expansion. Exports declined by 13.3% y-o-y to 26 mnt, while imports surged by 92.3% y-o-y to 12.5 mnt, indicating increased reliance on imported ore to bridge the gap between domestic availability and steelmaking requirements.

Coal: Domestic coking coal production declined marginally by 2.3% y-o-y to 65 mnt, while imports increased by 9.1% y-o-y to 84 mnt. The rise in imports reflects the need to support higher steel output amid limited domestic availability, reinforcing Indias structural dependence on imported coking coal.

In contrast, thermal coal imports declined by 5.3% y-o-y to 160 mnt, while domestic production remained broadly stable, indicating a lower import requirement. This divergence highlights improving domestic availability in thermal coal, even as dependence on imported coking coal continues to persist.

Scrap: Domestic scrap availability increased by 24.5% y-o-y to 31.5 mnt, supported by policy measures and improved collection and processing systems. Scrap imports declined by 12.4% y-o-y to 8.5 mnt, indicating a gradual shift towards domestic sourcing. The rise in domestic scrap supports the expansion of the electric arc furnace route and reflects a structural shift towards a more circular steel ecosystem.

Outlook:

Domestic steel prices are expected to find some support in the near term, aided by lower finished steel imports and continued policy oversight, although any sharp recovery remains contingent on demand absorption. Export prospects may remain steady on the back of competitive pricing, even as weak global demand conditions limit upside.

On the domestic front, infrastructure-led demand is likely to underpin consumption, but the pace of growth will be key to sustaining utilisation levels amid expanding capacity. At the same time, ongoing US-Iran tensions pose a risk to energy markets, with potential volatility in crude prices likely to translate into higher input and freight costs for the steel sector.