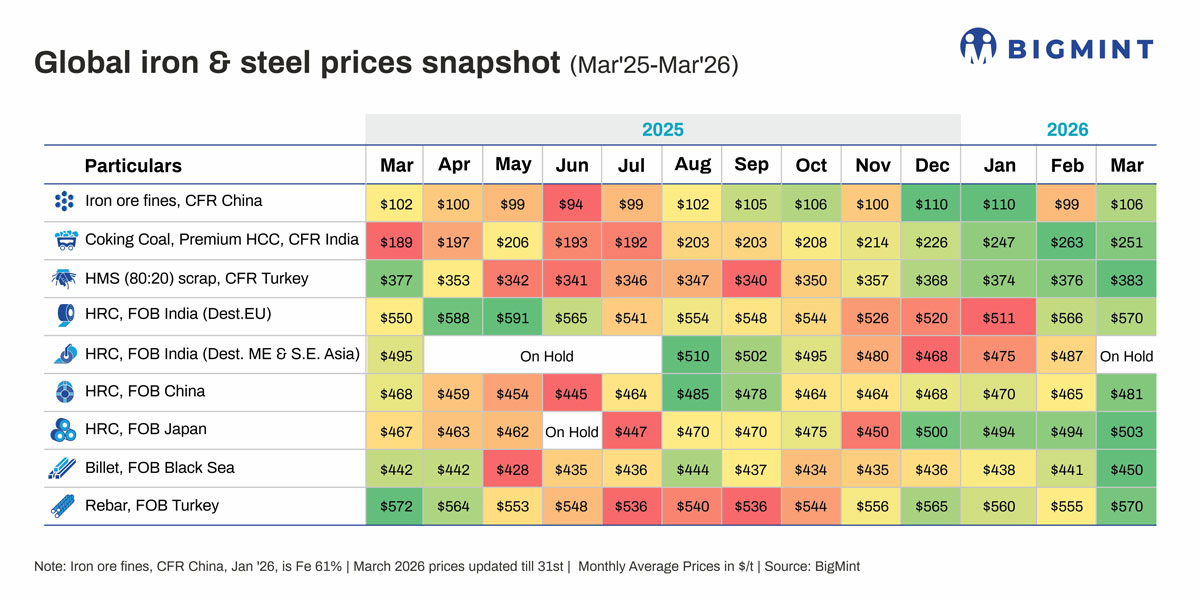

Global steel, raw material prices rise m-o-m in Mar'26 as US-Iran conflict disrupts supply chains

...

- Indian imported PHCC bucks trend, prices drop as supply constraints ease

- Chinese iron ore up 7% on supply uncertainty, high port stocks cap gains

- Firm input costs, domestic demand recovery lift Chinese HRC export offers

Morning Brief: Global steel and raw material prices climbed higher m-o-m in March 2026 except for coking coal, as the US-Iran conflict, which started on 28 February, halted oil and natural gas dispatches from the Middle East and lifted freights across the world. Steel production costs increased due to raw material shortages as trade flows became disrupted, and mills sought to raise prices to pass on cost pressures. However, steel demand remained weak, as activity in end-user segments also slowed due to geopolitical tensions.

Snapshot of key price movements in Mar'26

Chinese imported iron ore: Chinese imported Fe 61% iron ore fines prices rose 7% y-o-y, driven primarily by supply concerns. Uncertainty around sourcing of BHP shipments, higher freight costs due to the US-Iran conflict, and expectations of improved steel exports following the absence of Iranian billets from the market lifted prices.

Moreover, economic announcements at the Two Sessions meeting, lower exports from Brazil (amid wet weather) and from India (due to weak realisations), and Australian supply risks related to Cyclone Narelle also boosted market sentiment. However, ample port inventories, which stood at 177.5 million tonnes (mnt) on 2 April, continued to restrain sharper increases.

Indian imported coking coal: Indian imported premium hard coking coal (PHCC) prices fell 5% m-o-m as supply improved following shortages in January-February due to cyclone-related disruptions in Australia. Buyers were also cautious, waiting for prices to moderate further, amid sufficient stocks accumulated previously. Rising freights and shipping disruptions following the outbreak of the Middle East conflict also kept buyers on the sidelines.

However, from the middle of the month, prices started rising again, as surging freights and steady domestic steel price gains pushed suppliers to raise offers.

Turkish imported melting scrap: Turkish imported HMS 80:20 prices inched up by 2% m-o-m as freights climbed higher and demand strengthened amid limited inflows of semi-finished steel. Delivery timelines from China increased, coupled with reduced billet and slab availability from Iran, Russia, and other Middle East countries, forcing mills to accelerate scrap purchases. In fact, around 23-27 March, over 520,000 t of scrap were booked by mills looking to restock inventories following the conclusion of Ramadan and Eid.

Russian exported billets: Russian billet prices edged up by 2% m-o-m, supported by stronger Asian levels and higher scrap costs. Despite subdued downstream demand, such as for Turkish rebars, mills remained resistant to reducing prices due to higher production and transportation costs and tax burdens.

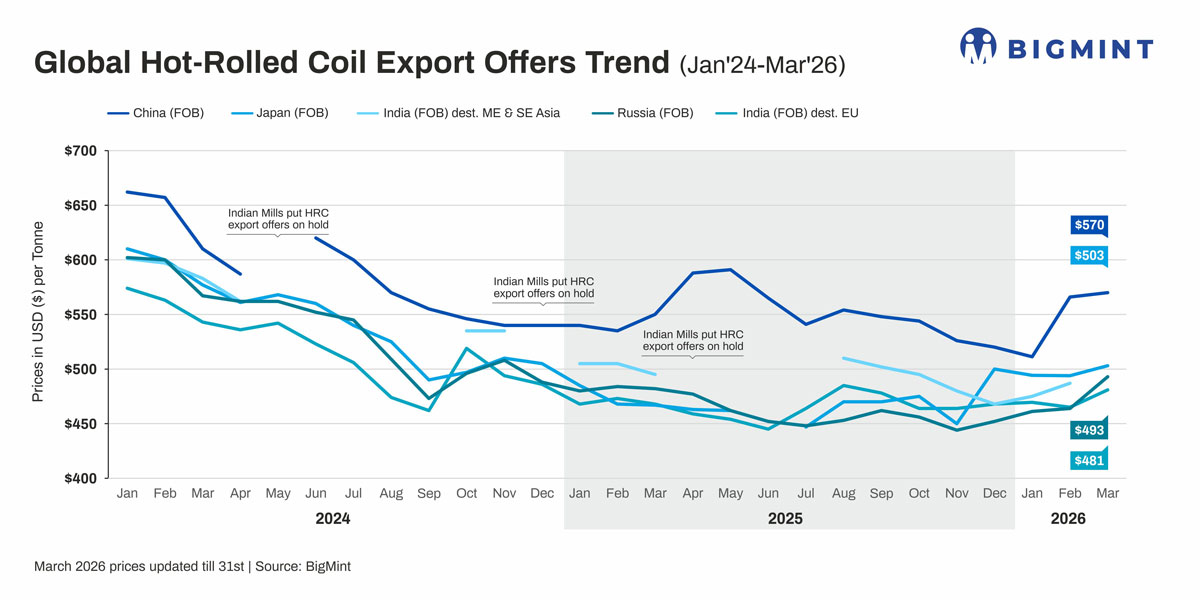

HRC export offers: Chinese hot-rolled coil (HRC) export offers strengthened by 3%, supported primarily by firm raw material costs and improving domestic market conditions. Higher prices of iron ore and coal, along with tightening HRC inventories and better domestic sales, enabled mills to adopt a firmer pricing stance. However, elevated freights and higher offers curtailed buying interest, with overseas buyers remaining cautious.

Indian HRC export offers to the EU also increased by about 1% m-o-m, but trade was largely paused due to logistics disruptions. No firm offers were issued from around mid-March.

A Europe-based source indicated that already booked shipments would be honoured under existing contractual terms. However, disruptions in delivery schedules and routes and a sharp escalation in freights (40-50% to the EU, as per some estimates) and war-risk insurance premiums limited transactions.

Similarly, HRC export activity to the Middle East came to a standstill, with no firm Indian offers heard. Indian mills also prioritised domestic sales due to better realisations amid tight supply.

Turkish exported rebars: Turkish rebar export prices rose around 3% m-o-m in March, driven primarily by higher input costs. A sharp increase in imported scrap prices, along with elevated energy and logistics costs, pushed mills to raise both domestic and export offers.

Additional support came from modest demand recovery after the Ramadan period and improved weather conditions, alongside emerging buying interest from Europe. However, the price uptrend remained largely cost-driven, as overall demand stayed weak amid global uncertainty, geopolitical disruptions in the Middle East, and subdued construction activity.

Notably, in January-February 2026, Turkish rebar exports fell by 17% y-o-y to 648,700 t. Volumes to the MENA region fell 27% y-o-y, though it remained the largest destination. Europe, which received around 34% of Turkish rebar exports in the year-ago period, saw its share shrink to 20% in January-February 2026 following a 51% drop in volumes.

Outlook

BigMint expects global steel and raw material prices to remain on the higher side in April amid increased energy costs. Despite the ceasefire, it will take time for fuel prices and freights to return to February levels, given that exporters may rush to complete pending deliveries as shipping risks ease. This will lead to landed costs of imported materials remaining elevated for the time being.

Moreover, buyers will likely show resistance to higher prices, as fuel shortages have also impacted industrial activities and may push end-users to curtail production. Consequently, prices are likely to rise only modestly.