Global steel, raw material prices diverge in Feb'26; Chinese New Year, Ramadan impact trade

...

- Chinese iron ore prices fall on low steel output, high port stocks

- Indian coking coal prices up on tight supply even as demand moderates

- Domestic price surge in EU pushes up Indian HRC export offers

Morning Brief: Global steel and raw material prices showed mixed trends m-o-m in February 2026, as the Chinese New Year (15-23 February) and Ramadan (18 February-20 March) slowed down trading activity in key regions and commodities. Among raw materials, iron ore prices plunged, while tight supply continued to propel coking coal and scrap higher, leading to mixed trends in input costs. Meanwhile, steel prices also showed contrasting movements, though demand was largely muted across most regions.

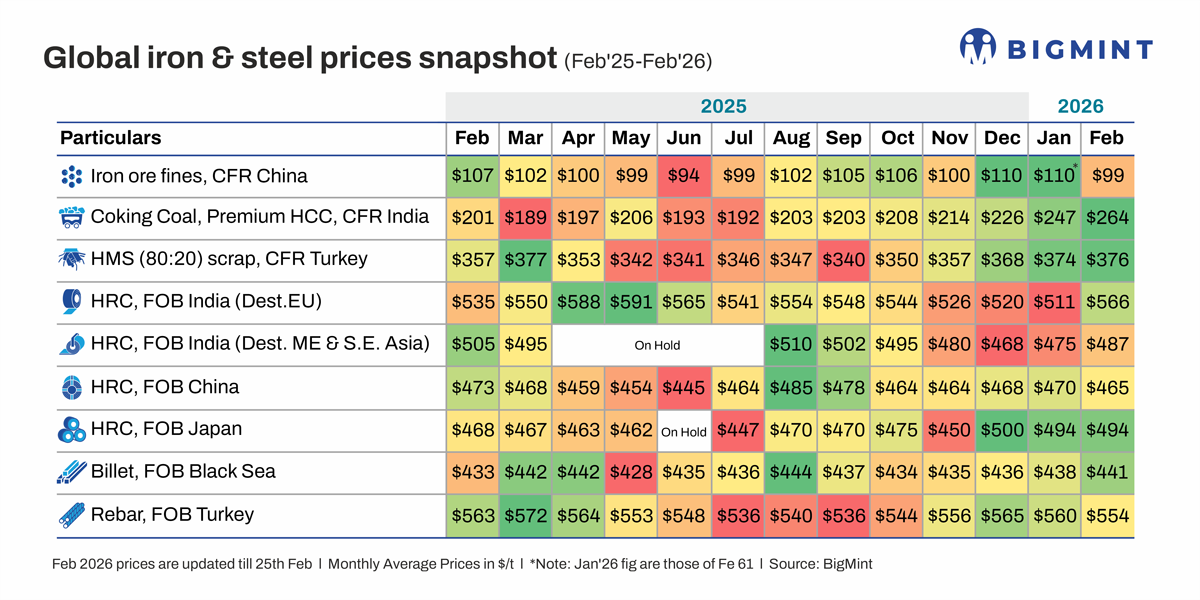

Snapshot of global steel, raw material prices in Feb'26

Chinese imported iron ore: Chinese iron ore fines prices (Fe 61%) fell 10% m-o-m, as demand remained weak in the lead-up to the Lunar New Year holidays. Crude steel production fell 9% y-o-y in early February, while it was up by a minor 0.6% compared to late January, as per the China Iron and Steel Association (CISA). Meanwhile, portside stocks, as well as mill inventories, remained elevated, with Bloomberg reporting that volumes hit their highest since 2022 on 6 February.

Indian imported coking coal: Indian imported coking coal prices continued to surge in February, up 7% m-o-m. Heavy rainfall and cyclone-related disruptions in Australia tightened availability in January, evidenced by a 19% m-o-m decline in exports. Consequently, offers remained high as the market entered February.

However, prices began to soften slightly from the second week, with rains in Australia having subsided and Chinese demand muted due to the holidays. Moreover, Indian buyers pushed back against the higher prices, delaying purchases until prices turned more favourable.

Turkish imported ferrous scrap: Turkish deep-sea scrap prices rose slightly amid tightening scrap availability in the US and Europe due to harsh winter conditions. Scrap collection rates in parts of the Baltic region were said to be just 30-40% of normal levels in early February, with costs remaining persistently at elevated levels.

However, while tight scrap supply supported prices, weak rebar demand and squeezed margins put mills in "wait-and-watch" mode. Additionally, Ramadan-related slowdowns curbed mill activity. Consequently, buying was measured, which limited any sharp price hikes.

Black Sea billets: Russian-origin CIS billet export prices also increased marginally, as sellers lifted offers amid rising production and logistics costs. Russian producers quoted $445-448/t FOB for March-April shipments, with mills refraining from reducing prices, supported by rouble fluctuations and limited spot sales pressure. However, trading activity was largely sluggish, in part due to the onset of Ramadan in key destinations.

Turkish rebar exports: Persistently weak demand, fuelled by sluggish construction activity during winter, led to a 1% drop in Turkish rebar export offers. Only small-lot sales to Africa, Georgia, Cyprus, Chile, and Peru were recorded in February. EU buying interest stayed cautious amid the Carbon Border Adjustment Mechanism (CBAM) implementation. Domestically, subdued construction activity continued, pressuring prices.

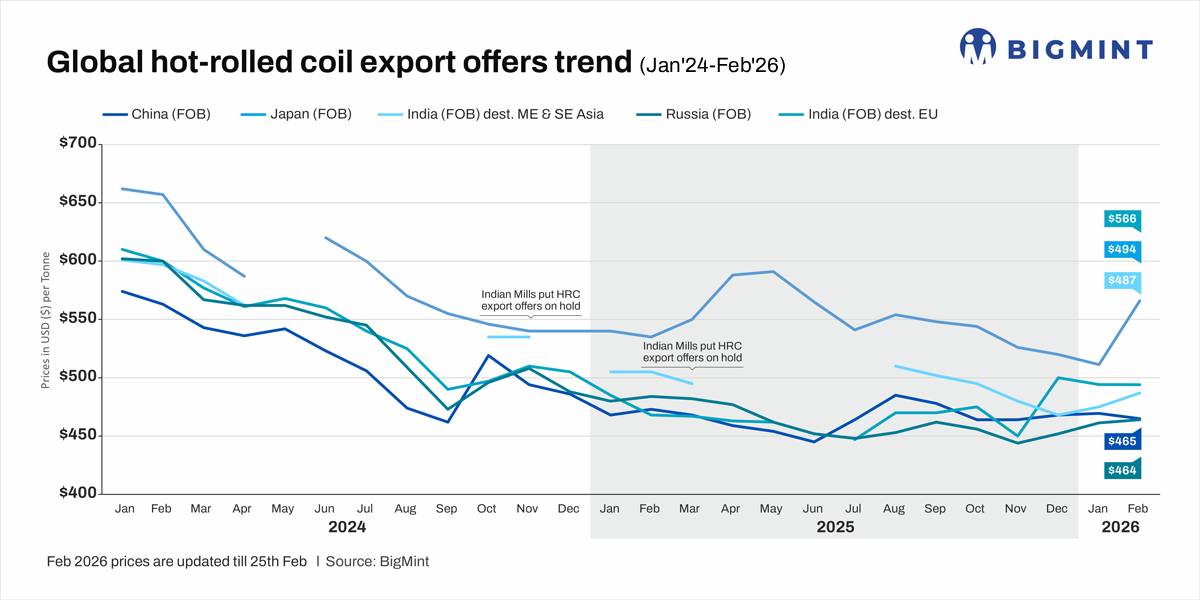

HRC export offers: Chinese HRC export prices declined by 1% m-o-m, as the onset of Ramadan dampened demand in key importing markets such as the Middle East and Southeast Asia. The approaching Lunar New Year holidays also pushed sellers to trim offers.

Indian HRC export offers to the EU surged 11% m-o-m, driven by strong price gains in the Indian and EU domestic markets. European mills continued pushing prices upward as imports remain limited, with expectations of stricter safeguard measures keeping mills bullish. For example, ArcelorMittal, a leading European steelmaker, raised its HRC prices by around EUR 50/t ($59/t) m-o-m to EUR 750/t ($884/t) base delivered for May dispatches. However, demand remained weak due to adequate domestic inventories and uncertainty regarding safeguard quota reductions.

Indian HRC export offers to the Middle East rose moderately by 3% m-o-m. First, higher realisations in the Indian market encouraged mills to lift offers. Demand was also moderately strong, with a deal for around 33,000 t heard concluded. However, market sentiment in the region gradually softened ahead of Ramadan.

Outlook

In March 2026, BigMint expects iron ore prices to rise slightly, as Chinese buyers return to the market for restocking. Chinese steel demand is also likely to improve, recovering from the holiday-driven slowdown of February.

Conversely, coking coal prices will moderate, as supply normalises. This is a cyclical trend observed in most years. Similarly, as winter fades and collection improves in the US and the EU, scrap prices may decline slightly in March.

Lower scrap prices will drag billet prices lower, also enabling buyers to push down Turkish rebar prices, though the approaching domestic construction season in April may limit the price drop.

Chinese HRC prices are also likely to decline as demand in the Middle East and Southeast Asia remains subdued amid Ramadan. While Indian offers to the Middle East may soften for the same reason, the decline is likely to be limited, as the domestic market continues to offer better realisations. On the other hand, Indian export offers to the EU may decrease as demand remains stagnant.