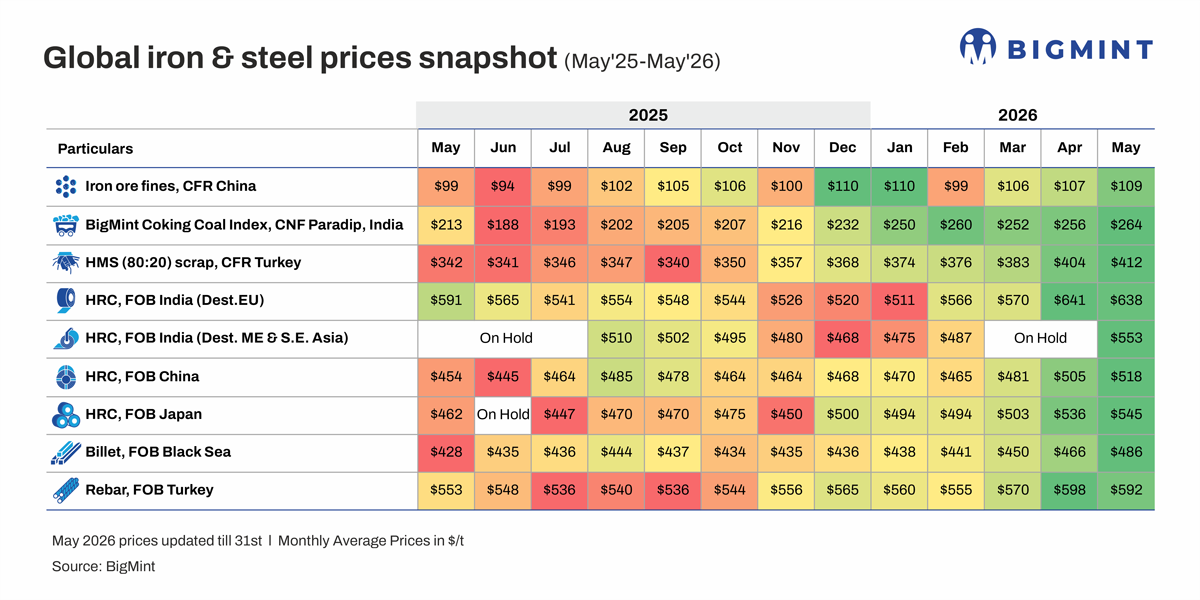

Global steel, raw material prices climb up in May'26; Chinese HRC export offers hit 19-month high

...

- Higher freights amid Middle East conflict continue to lift prices

- Indian imported coking coal hits 3-month peak on supply crunch

- Chinese iron ore prices inch up as hot metal output remains high

Morning Brief: Global steel and raw material prices increased by 2-4% m-o-m across most commodities in May 2026 amid supply constraints and elevated freights. Only export offers for EU-bound Indian hot-rolled coils (HRCs) and prices of Turkish rebars fell by 1% m-o-m.

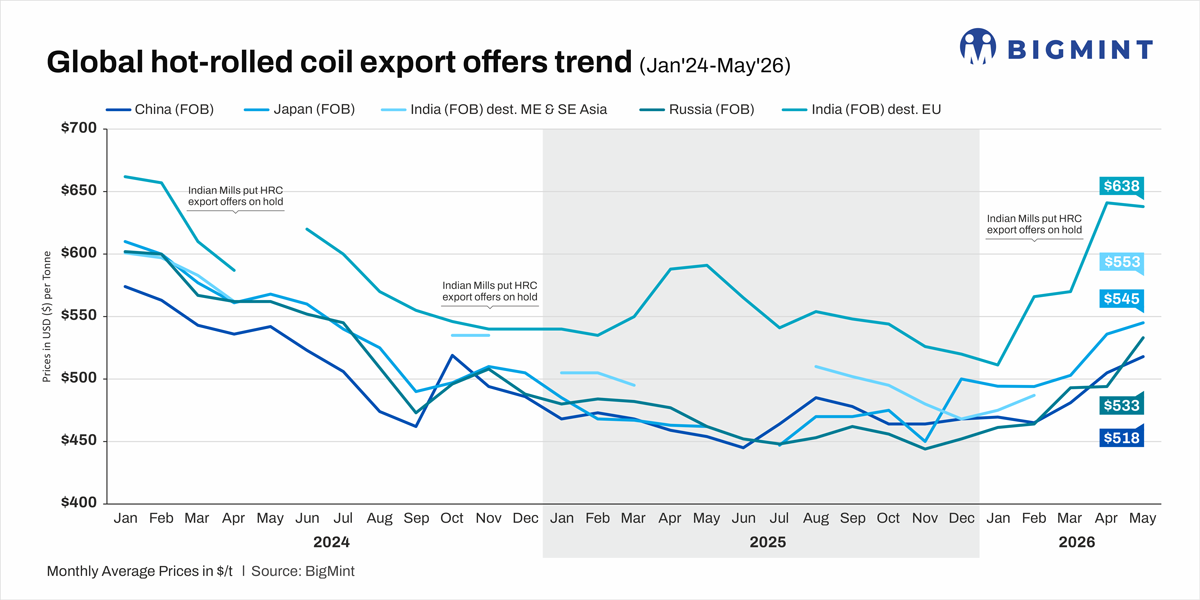

Notably, Chinese HRC export offers hit a 19-month high, increasing for the fourth consecutive month, supporting an uptrend in global flat steel prices.

Although the US and Israel have reached a fragile truce in their conflict with Iran, crude oil prices remain elevated (WTI crude futures are up nearly 40% from pre-conflict levels). As such, prices of most commodities tracked remained higher by over 10% since pre-conflict levels.

Only Indian coking coal prices were up a minor 2%, having already surged earlier in the year following weather-related supply disruptions in Australia. Meanwhile, Turkish rebar export prices were higher by 7% due to lacklustre demand.

Global manufacturing sentiment also remained broadly supportive for steel demand. According to the global purchasing managers' index, global factory output growth accelerated to its strongest level since 2021, as manufacturers accelerated purchases of raw materials and finished goods to build inventories against potential shortages and continued price hikes.

However, concerns have emerged that while forward purchasing and inventory accumulation may support demand in the short term, it could result in slower purchasing activity later in the year once inventories are rebuilt.

Snapshot of key price movements in May'26

Chinese imported iron ore: Chinese iron ore fines (Fe 61%, Australia origin) prices increased a minor 2% m-o-m. Prices strengthened after the Labour Day holidays amid elevated freights, improving steel market profitability, and stable hot metal output at 2.4 mnt/day. Hot metal output remained elevated despite easing from around 2.45 mnt/day last year).

However, the price rise moderated in the second half of the month, driven by adequate cargo availability, ample portside inventories, and softening steel export demand.

Indian imported coking coal: BigMint's premium hard coking coal (PHCC) index increased 3% m-o-m in May, reaching the highest level since February. The increase was driven by delays across Australian premium mid-volatile coal production, which tightened prompt cargo availability. Expectations of tighter supply in China, following a deadly mine accident in Shanxi, also supported prices. Additionally, higher shipping costs from Australia to India increased delivered coal prices. Consequently, sellers maintained firm offers despite patchy buying activity due to weakening Indian steel prices and ample inventories.

Turkish imported melting scrap: Turkiye's imported HMS 80:20 scrap prices increased 2% m-o-m due to elevated freight costs, tight availability of premium US-origin cargoes, strong collection prices, and reduced supply of billets.

However, Turkish mills remained cautious throughout the month as finished steel demand failed to keep pace with rising raw material costs. The scrap-to-rebar spread narrowed to $177-185/t, and most mills limited purchases to immediate requirements and increasingly turned to domestic scrap.

Sentiment weakened towards the end of May as Eid holiday-related slowdowns and growing availability of short-sea cargoes shifted bargaining power towards buyers.

Russian/CIS billet exports: Black Sea billet prices gained 5% m-o-m, as Russian exporters raised offers amid tighter billet availability, firmer scrap prices, elevated production costs, and a stronger rouble. However, momentum weakened towards the month-end as poor downstream steel demand in Turkiye and compressed steelmaking margins reduced billet procurement.

Chinese HRC export offers: Chinese HRC export prices rose 3% m-o-m, recovering to levels last seen in October 2024.

The rally was supported by firm iron ore and coal prices, an appreciating yuan, and strong export order books. Steelmakers also benefited from improved domestic demand after the Labour Day holidays, which pushed them to resist lower bids. Ongoing slab exports (driven by limited semis supply from the Middle East) reduced flat steel availability, while continued pricing advantage over competing suppliers supported buying interest.

However, demand softened slightly towards the month-end amid increasing price resistance.

Indian HRC export offers: Indian HRC export activity showed a mixed regional trend during May. Export offers to the EU inched down by 1% amid muted demand as buyers waited for clarity on revised safeguard measures scheduled to take effect from 1 July. Concerns over the potential downsizing of safeguard quota allocations, higher out-of-quota duties, compliance costs related to the Carbon Border Adjustment Mechanism (CBAM), and weak downstream demand continued restricting buying interest.

Meanwhile, offers to the Middle East and Southeast Asia resumed after weeks of disruption linked to geopolitical tensions and shipping constraints around the Strait of Hormuz. BigMint recorded around 50,000 t booked at $550-560/t FOB for June shipment, with a sharp jump in offers compared to February, supported by a steep price rise over the same period and supply shortages in the domestic market.

Turkish rebar export offers: Turkish rebar export prices inched down by 1% m-o-m in May. While higher scrap costs continued supporting offers, weak construction activity, sluggish rebar sales, and subdued demand across key export markets limited mills' ability to raise prices further. The market remained primarily cost-supported rather than demand-driven throughout the month.

Outlook

BigMint expects global steel and raw material prices to show mixed trends in June, with support from elevated energy and shipping costs offset by improving supply conditions and seasonal demand weakness.

Supply disruptions in Australia and China should lift coking coal prices. However, iron ore is likely to face supply pressure as June marks the peak season for iron ore shipments to China, with Australian miners boosting volumes as part of a fiscal year-end push and Brazilian miners taking advantage of improving weather.

Additionally, scrap prices may also soften as supply improves in the US and narrow rebar margins push mills to reduce bids. Slower steel demand in China, given the onset of the rainy season, may also weigh on Chinese HRC prices.

However, price movements are likely to remain within a narrow range, supported by still-positive manufacturing activity across major economies.