Global primary aluminium output posts marginal decline in 5MCY'26 amid regional supply disruptions

...

- GCC recovery hinges on geopolitical stability

- Mozal shutdown hits African aluminium production

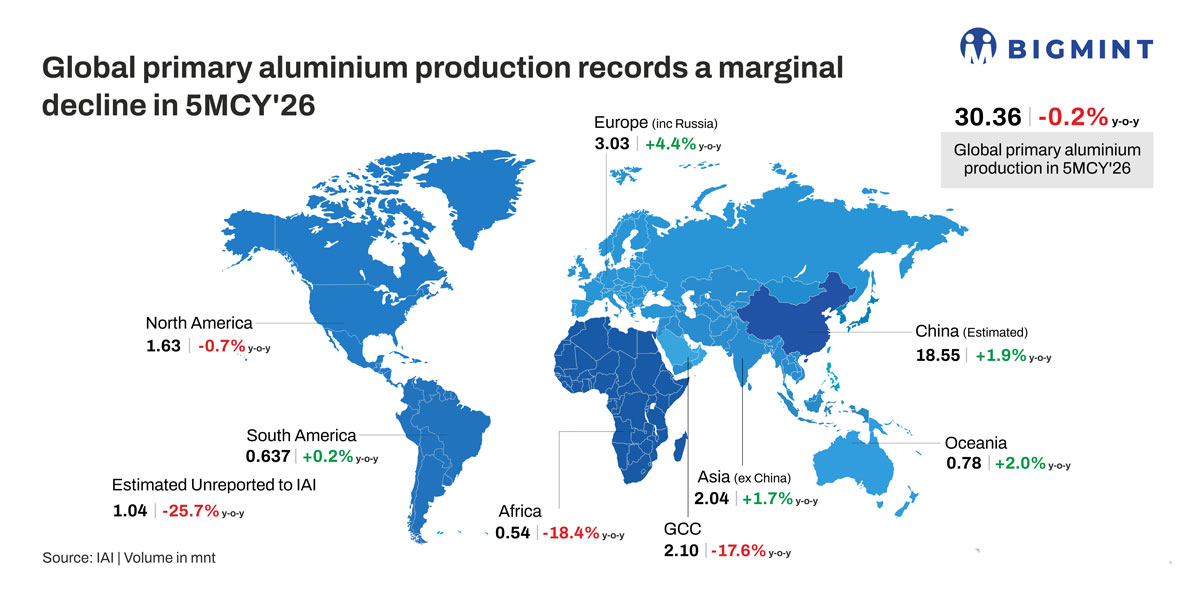

Global primary aluminium production stood at 30.24 mnt in 5MCY'26, marking a marginal y-o-y decline from 30.25 mnt in 5MCY'25, according to data from the International Aluminium Institute.

Global primary aluminium production in 5MCY'26 exhibited mixed regional trends, reflecting the combined impact of energy availability, geopolitical disruptions, raw material supply adjustments, operational changes and evolving trade dynamics across major producing regions. While production increased in China, Europe (including Russia), Asia (excluding China) and Oceania, sharp declines in Africa and the Gulf Cooperation Council (GCC) offset much of the growth, with the Middle East continuing to emerge as a key factor influencing near-term global aluminium supply conditions.

Regional drivers shaping global primary aluminium output in 5MCY'26

China, the world's largest aluminium producer, increased estimated primary aluminium output by 1.9% y-o-y to 18.55 mnt during 5MCY'26, supported by resilient smelter operating rates, adequate alumina availability, relatively stable power supply and firm domestic demand. However, production momentum remained constrained as the country continued operating close to its national smelting capacity ceiling of around 45 million tonnes, leaving limited room for further expansion. Following the Lunar New Year, downstream demand softened while exchange inventories increased, prompting producers to moderate operating rates rather than push additional supply into an already well-supplied domestic market. At the same time, China continued benefiting from improving export opportunities amid supply disruptions in the Middle East, helping maintain relatively stable production despite broader global uncertainties.

In Africa, primary aluminium production declined sharply by 18.4% y-o-y to 0.54 mnt from 0.67 mnt in 5MCY'25. The decline was primarily attributed to the shutdown of South32's Mozal aluminium smelter in Mozambique after the company failed to secure a long-term, cost-effective electricity tariff agreement. As one of Africa's largest aluminium producers, the closure significantly reduced regional output and tightened global aluminium availability.

North America recorded a marginal 0.7% y-o-y decline to 1.63 mnt, as elevated energy costs, competitiveness pressures and limited investment in new smelting capacity continued to constrain production growth. Although most smelters maintained relatively stable operating rates, routine maintenance activities and cautious production management amid uncertain market conditions weighed on overall output.

South America remained broadly stable, with production increasing marginally by 0.2% y-o-y to 0.637 mnt. Stable power availability, consistent operating rates and the absence of major operational disruptions enabled regional producers to maintain output close to last year's levels. However, some Brazilian facilities continued to operate below full capacity due to planned maintenance activities, infrastructure constraints and elevated electricity costs.

Conversely, Asia (excluding China) posted a 1.7% y-o-y increase, with production reaching 2.04 mnt during 5MCY'26. Growth was supported by improved operating rates, stable alumina availability, recovering industrial activity and rising regional competitiveness as global buyers increasingly diversified supply chains beyond China. Nevertheless, operational challenges persisted across parts of Southeast Asia, particularly in Indonesia, where grid constraints, coal supply issues and routine maintenance limited stronger production growth.

Europe (including Russia) registered the strongest regional growth, with production increasing 4.4% y-o-y to 3.03 mnt. The improvement was driven by the gradual restart of previously idled smelting capacity as stronger aluminium prices and easing energy-related pressures improved operating economics. However, elevated electricity and natural gas costs continued to restrict a broader recovery, while periodic maintenance shutdowns and operational adjustments at several European and Russian smelters limited further output gains.

Oceania recorded a 2.0% y-o-y increase in production to 0.78 mnt, supported by stable hydropower-linked smelting operations, reliable electricity supply and improved operational efficiency across Australian facilities. Growth, however, remained partially constrained by scheduled maintenance activities and tighter alumina availability.

Production across the Gulf Cooperation Council (GCC) declined sharply by 17.6% y-o-y to 2.10 mnt from 2.55 mnt in 5MCY'25, making it the weakest-performing major producing region during the period. The decline reflected the continued impact of the US-Iran conflict, which disrupted smelting operations, regional logistics and raw material supply chains. According to the International Aluminium Institute (IAI), GCC primary aluminium production fell to 338,000 t in May, down 35% y-o-y and nearly 40% below pre-conflict levels, marking the region's lowest monthly output since 2013. The prolonged disruption effectively erased more than a decade of capacity growth across the GCC. Although month-on-month production stabilised in May, the IAI noted that a meaningful recovery will depend on further geopolitical stability and the gradual restoration of normal operating conditions. Disruptions to aluminium and alumina shipments through the Strait of Hormuz, combined with operational challenges at major regional smelters, continued to weigh heavily on output. Despite contributing less than 10% of global primary aluminium production, the GCC supplies a disproportionately large share of aluminium imports to key consuming markets, including the US, Europe and Japan, amplifying the impact of lower regional production on global supply chains and keeping physical aluminium markets outside China relatively tight.

Finally, estimated unreported production to the International Aluminium Institute (IAI) declined by 25.7% y-o-y to 1.04 mnt during 5MCY'26.

Impact of pricing

On a 5MCY basis, LME aluminium prices averaged $3,369/t in 5MCY'26, marking a sharp 32.4% y-o-y increase from $2,544/t in 5MCY'25. Meanwhile, LME aluminium inventories declined by 12.8% y-o-y, averaging 413,428 t compared with 474,092 t during the same period last year.

The higher average LME aluminium prices in 5MCY'26 were underpinned by continued physical market tightness, lower exchange inventories, and concerns over supply disruptions from the Middle East. Fears of potential disruptions to shipments through the Strait of Hormuz supported prices for much of the period, while the subsequent easing of geopolitical risks and a stronger US dollar triggered a correction toward the end of June. Despite this pullback, average prices remained well above year-ago levels.

Outlook

Global primary aluminium production is expected to remain constrained in the near term as supply losses in the GCC and Africa are unlikely to be fully offset by incremental gains in China and Europe. With China's smelting capacity nearing its policy ceiling and GCC recovery dependent on geopolitical stability, global supply growth is expected to remain limited.