Global metallurgical alumina production stays resilient in 4MCY'26 despite production pressures in key regions

...

- China anchors global alumina output amid regional divergence

- Asia-led gains offset declines across mature refining markets

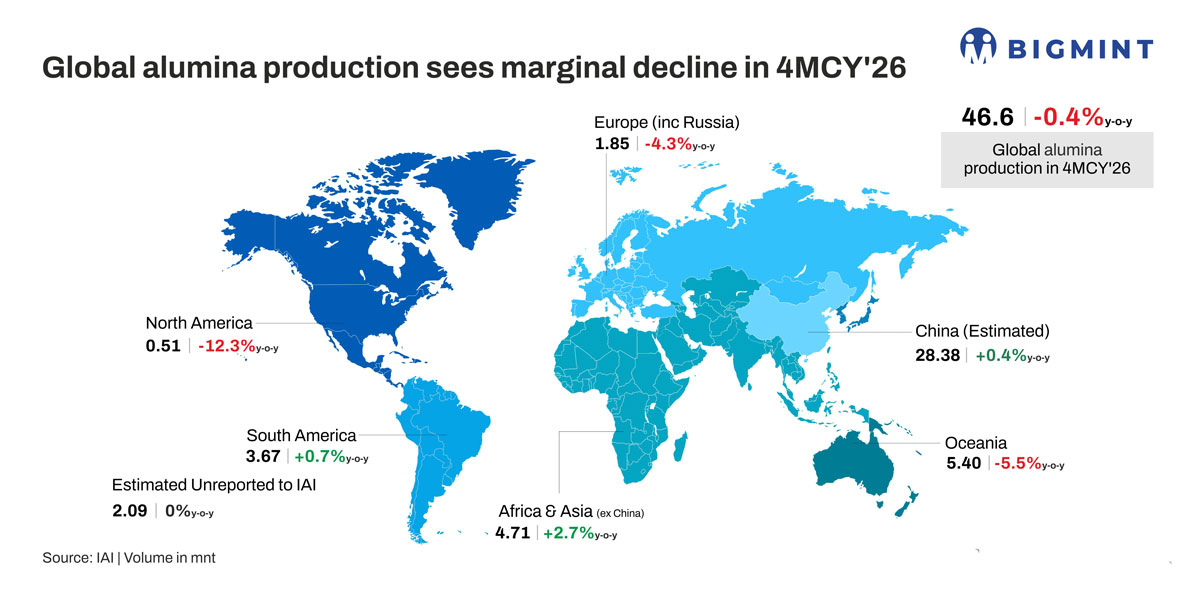

Global alumina production stood at 46.6 mnt in January-April 2026 (4MCY'26), marginally lower by 0.4% y-o-y from 46.79 mnt in 4MCY'25, according to the International Aluminium Institute (IAI), indicating largely stable global output levels. Despite the slight decline, alumina production remained supported by steady refinery operations across key producing regions and adequate supply availability. Overall, the market maintained balanced production conditions during the period, with output levels broadly aligned with downstream aluminium sector requirements.

Regional drivers shaping global metallurgical alumina output

Global alumina production in 4MCY'26 witnessed mixed regional trends, as stable output growth in China and emerging refining regions partially offset production declines across several mature alumina markets amid refinery maintenance shutdowns, environmental restrictions, rising energy costs, operational disruptions, and weather-related challenges. Overall, the global alumina market continued facing pressure from maintenance cycles, shifting regional competitiveness, and softer production momentum following exceptionally strong output levels recorded at the end of 2025.

China, the world's largest alumina producer, reported estimated output of 28.38 mnt, up marginally by 0.4% y-o-y from 28.25 mnt. Production remained supported by stable refinery utilisation rates and adequate raw material availability. However, output momentum slowed sequentially due to scheduled refinery maintenance and environmental-related shutdowns across key producing provinces such as Henan, Guangxi, and Guizhou. Despite temporary disruptions, China continued expanding long-term refining capacity, with several new refinery projects expected to come online during 2026.

Africa & Asia excluding China recorded production of 4.71 mnt, rising 2.7% y-o-y from 4.58 mnt. Growth in the region was supported by refinery expansions, stronger operating rates in India and Indonesia, and rising downstream investments across Southeast Asia. Indonesia remained one of the key contributors following capacity ramp-ups at newly expanded alumina facilities such as PT Bintan Alumina Indonesia.

However, production growth moderated sequentially after aggressive operating rates and elevated output levels recorded during the end of 2025. Meanwhile, Africa also witnessed operational pressure in parts of the aluminium value chain, particularly after Mozambique's Mozal smelter was placed on care and maintenance following electricity tariff-related challenges faced by South32.

South America produced 3.67 mnt, up 0.7% y-o-y from 3.65 mnt, supported by stable operations at Hydro's Alunorte refinery in Brazil along with infrastructure improvements completed in recent years. Output growth, however, remained moderate due to logistical constraints and normalization from elevated year-end production levels. Brazilian operations including Albras and Alupar also continued facing infrastructure-related constraints and elevated power costs during the period.

Meanwhile, North America registered the sharpest decline among major producing regions, with output at 0.51 mnt, down 12.3% y-o-y from 0.58 mnt. The region continued facing pressure from elevated labour and energy costs, lower refinery utilisation rates, structural supply constraints, and maintenance-related disruptions despite limited operational improvements at select refineries such as the Gramercy refinery.

Conversely, Oceania witnessed production of 5.40 mnt, declining 5.5% y-o-y from 5.71 mnt, mainly due to planned refinery maintenance, weather-related disruptions, and ongoing structural challenges within Australia's alumina sector. Operational pressures also persisted due to ageing refinery infrastructure and the gradual closure of high-cost refining assets such as Alcoa's Kwinana refinery, while maintenance activity at Pinjarra and Wagerup also affected regional output.

Europe, including Russia, recorded production of 1.85 mnt, down 4.3% y-o-y from 1.93 mnt, as elevated gas and power costs weakened refinery economics and forced several producers to reduce operating rates amid subdued industrial activity and regulatory uncertainties. Several Russian and European smelters also underwent scheduled maintenance and anode-change cycles during the period.

Meanwhile, estimated unreported production to IAI remained unchanged at 2.09 mnt, indicating relatively stable output from non-reporting regions. Overall, alumina production trends during 4MCY'26 highlighted increasing volatility across the global alumina market, as refinery maintenance activities, energy-related pressures, weather disruptions, infrastructure constraints, and operational challenges continued reshaping global production dynamics.

Outlook

Global alumina production is expected to remain largely stable in the coming months, supported by steady refinery utilisation rates in China, ongoing capacity additions in emerging regions such as India and Indonesia, and sustained downstream aluminium demand.

However, production growth is likely to remain gradual amid refinery maintenance activities, elevated energy and operating costs across mature markets, weather-related disruptions, and logistical uncertainties. While China is expected to continue anchoring global supply, regions such as Europe and Oceania may remain under pressure due to weaker refinery economics and structural operational challenges, keeping global alumina market conditions balanced but volatile over the near term.