Global manganese ore imports rise 10% in CY'25 BigMint analysis

...

- China's ore imports climb 12% as smelters advance bookings, rebuild inventories

- Global Mn ore imports to grow modestly in CY'26

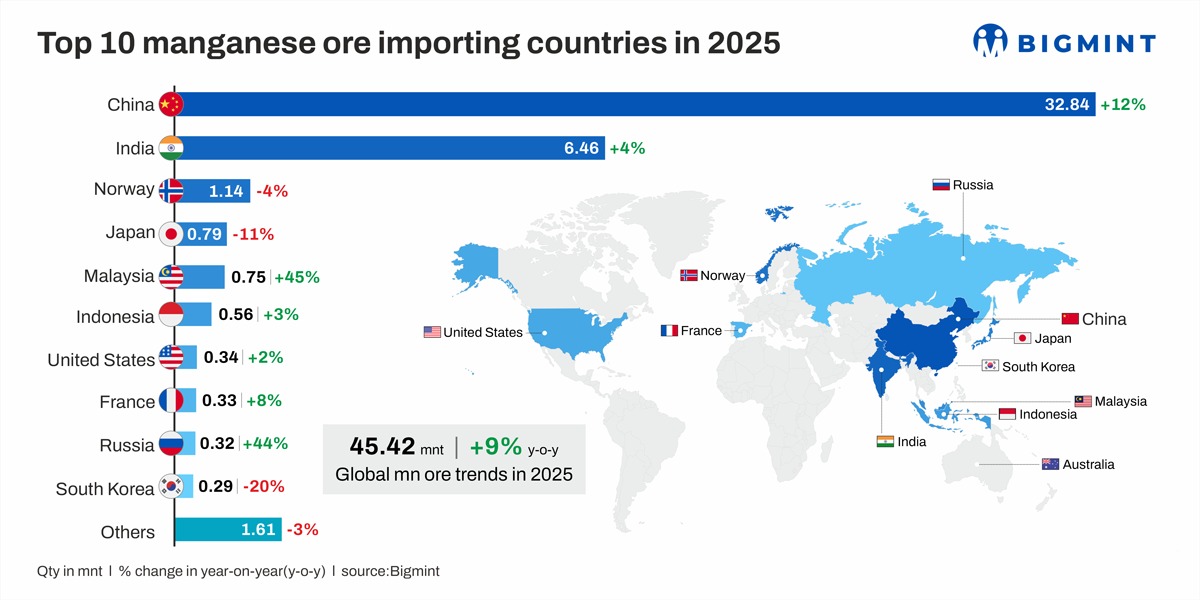

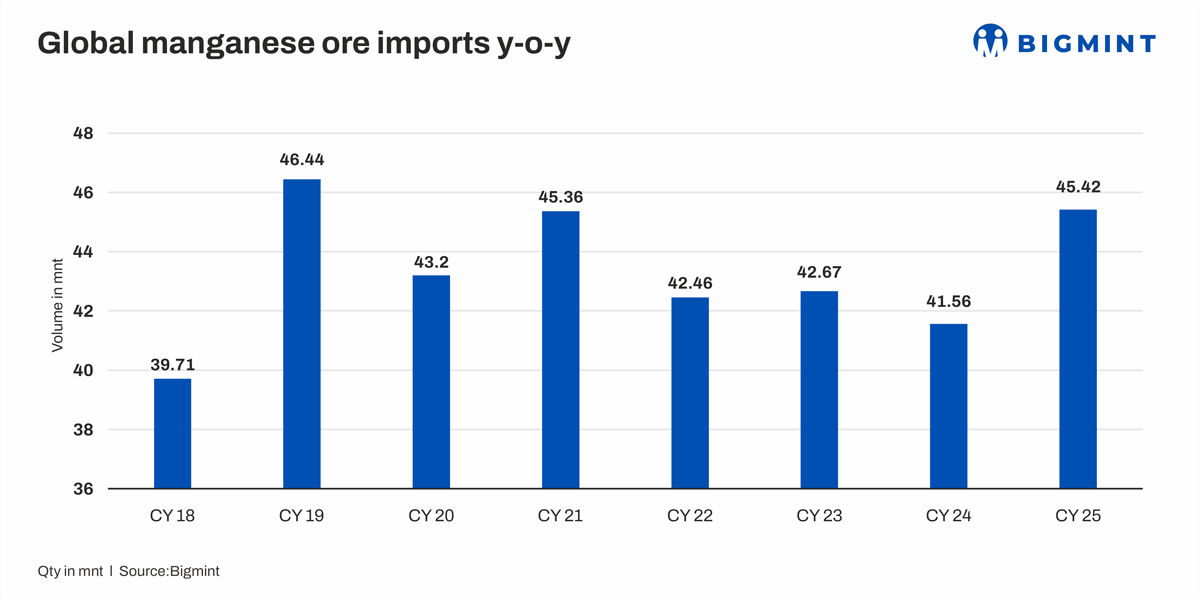

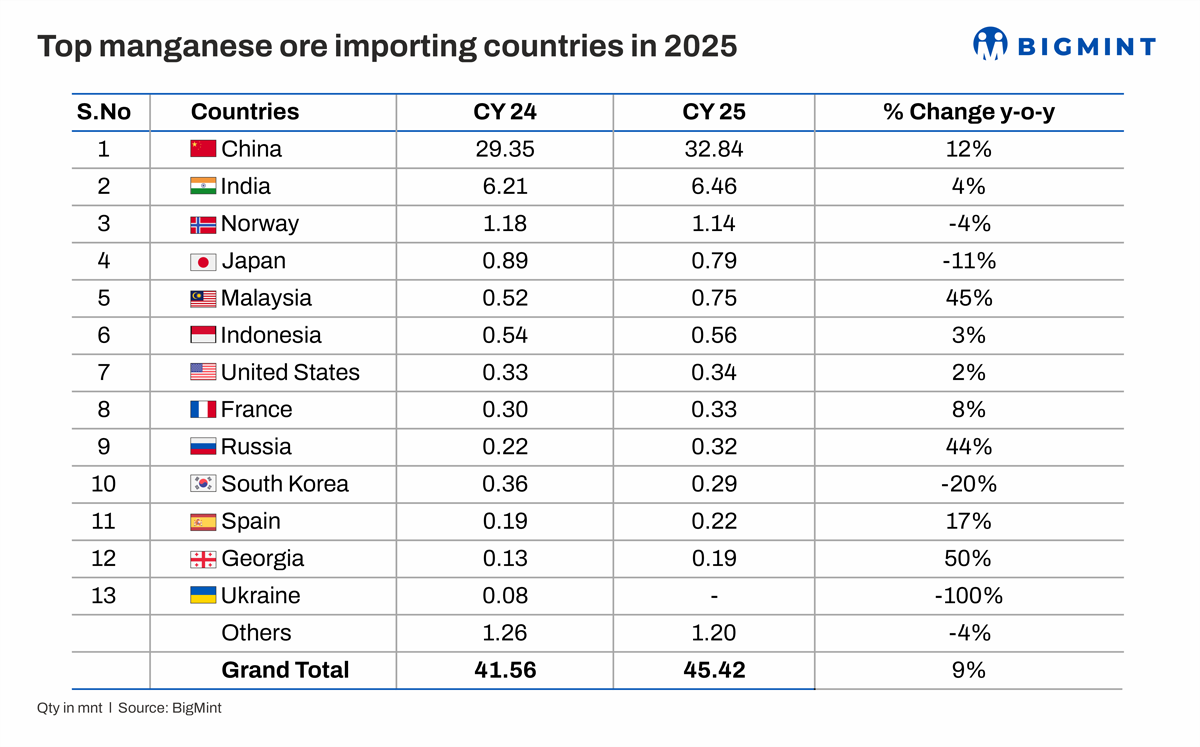

Global manganese ore imports increased from 41.5 million tonnes (mnt) in CY24 to 45.4 mnt in CY25, marking a rise of about 3.9 mnt y-o-y (10%). The growth was largely driven by stronger buying from key Asian markets, particularly China, India, and Malaysia. Factors such as front-loaded procurement, capacity expansions in alloy production, and improved supply availability from major exporters supported higher trade volumes, despite only moderate growth in global steel demand.

Key drivers of import growth

China, being the largest global buyer, saw imports rise 12% y-o-y to 32.84 mnt in CY25 (vs 29.5 mnt in CY24). The increase was primarily driven by procurement timing and improved supply availability, rather than a proportional rise in alloy output. Manganese alloy production remained largely stable, estimated flat to down ~12% y-o-y, indicating a disconnect between imports and actual consumption.

The surge was led by front-loaded buying in H125, as smelters advanced purchases to hedge against hydropower-related constraints and anticipated price increases. Concurrently, seaborne ore prices strengthened, with high-grade offers rising about 1015% during key booking periods, prompting cost-locking purchases.

On the supply side, higher shipments from Gabon, South Africa, and Australia added about 2-3 mnt y-o-y, easing earlier disruptions and improving cargo availability. Port inventories also rose, indicating that a significant share of imports was directed toward restocking. Overall, the growth reflects strategic inventory build (1-1.5 mnt) and advance procurement (1.52 mnt) rather than a structural demand surge.

India's manganese ore imports rose about 4% y-o-y, supported by capacity additions and strong steel demand. The commissioning and ramp-up of 3050 MVA submerged arc furnaces across Raipur, Durgapur, Jharkhand, and Raigarh added incremental alloy capacity, and few are increasing output for filtered carbon material contributing additional ore demand.

From May 2025 onward, softer imported ore prices improved competitiveness versus domestic material, triggering bulk bookings and forward procurement. This led to inventory build-up, making part of the import growth stocking-led rather than purely consumption-driven.

On the demand side, Indias crude steel production increased to 164.89 mnt in CY25 from 149.5 mnt in the previous year (10% y-o-y), supporting higher manganese alloy consumption. Overall, the import rise reflects a combination of capacity-led demand, opportunistic buying, and moderate restocking.

Factors limiting upside

Japan's manganese ore imports declined 11% y-o-y to 0.79 mnt in CY25 (vs 0.89 mnt in CY24), tracking a decline in crude steel production. Crude steel output fell to about 80.7 mnt (down 4% y-o-y) in CY'25, reducing manganese alloy demand and ore consumption.

Lower operating rates at alloy plants, coupled with adequate inventories, limited fresh procurement. Unlike China and India, Japans imports reflected a demand-led correction, with weaker industrial activity weighing on volumes.

South Korea's manganese ore imports dropped 20% y-o-y to 0.29 mnt in CY25 (vs 0.36 mnt in CY'24), reflecting weaker domestic demand. Crude steel production declined 3% y-o-y to 61.9 mnt (vs 63.6 mnt), leading to lower alloy output and reduced ore requirements.

Smelters operated at subdued utilization levels and relied on inventory drawdowns, limiting the need for fresh imports. Additionally, competitive imports of finished manganese alloys further reduced domestic production incentives. Overall, the decline reflects weaker steel demand and inventory-led adjustments, rather than supply constraints.

Outlook

Global imports are likely to grow modestly in CY26, slowing from CY25 highs as inventory-driven buying fades. China may stabilize, while India and Malaysia support demand through capacity growth. Japan and South Korea remain weak, capping gains. BigMint Take: Shift toward demand-led imports as stocking cycle normalizes.

To know more on what's happening in global manganese ore and alloys industry, join the 6th International Ferro Alloys Conference (IFAC 2026) being organized by the Indian Ferro Alloy Producers Association (IFAPA) which will take place in Goa from 16-18 September 2026.