Global lead market records marginal surplus in Jan-Apr'26 despite higher imports into China

...

- Refined lead market posts 7,000 t surplus in first four months of 2026

- Global lead demand remains flat as gains in key regions offset declines elsewhere

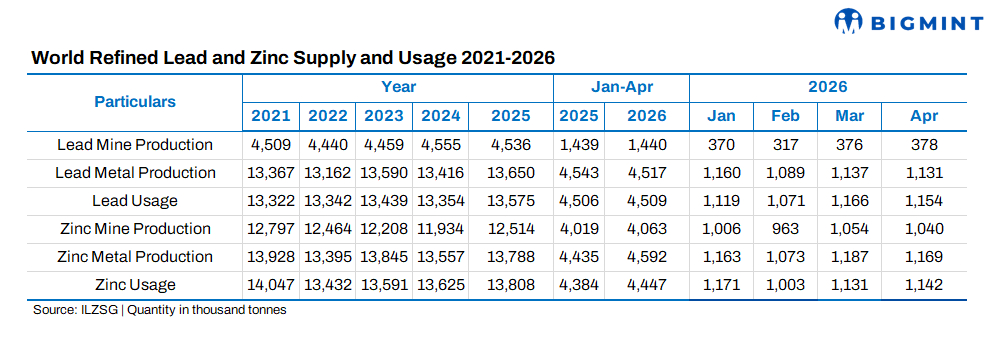

The global refined lead market recorded a surplus of 7,000 tonnes (t) during January-April 2026, according to preliminary data released by the International Lead and Zinc Study Group (ILZSG). Over the same period, total reported lead inventories increased by 48,000 t, indicating a gradual build-up in available material despite relatively balanced supply-demand fundamentals.

Mine supply remains stable

Global lead mine production remained broadly unchanged y-o-y during the first four months of 2026. Production gains in Portugal and Trkiye were offset by lower output in China, Sweden, and the United States, resulting in stable overall mined supply.

On the refined side, global lead metal production declined by 0.6% y-o-y. Reduced output in China, Mexico, and South Korea weighed on global production levels, although higher production in Brazil partially mitigated the decline following the commissioning of new secondary lead capacity in 2025.

Demand growth remains muted

Refined lead consumption increased marginally by 0.1% y-o-y during the review period. Higher demand in Brazil, Spain, and the United States was largely balanced by weaker consumption in Argentina, Mexico, South Korea, Trkiye, and the United Kingdom, reflecting subdued growth across major end-use sectors.

China import activity strengthens

China continued to increase its reliance on imported raw materials and refined metal. Imports of lead contained in concentrates rose 4.7% y-o-y to 412,000 t during January-April. Meanwhile, net refined lead imports surged to 126,000 t, up by 122,000 t compared with the corresponding period last year, highlighting stronger import requirements amid domestic supply constraints.

Outlook

The global lead market is expected to remain broadly balanced in the near term. Stable mine output, moderate inventory growth, and subdued consumption trends may limit significant price volatility. However, China's increasing import requirements and developments in secondary lead production will remain key factors influencing market dynamics through the remainder of 2026.