Global copper surplus widens in 2MCY'26 as inventories hit 23-year high: ICSG

...

- Scrap-driven supply offsets weak primary output

- Inventory build-up signals slowing demand momentum

Regional trends in copper mine production

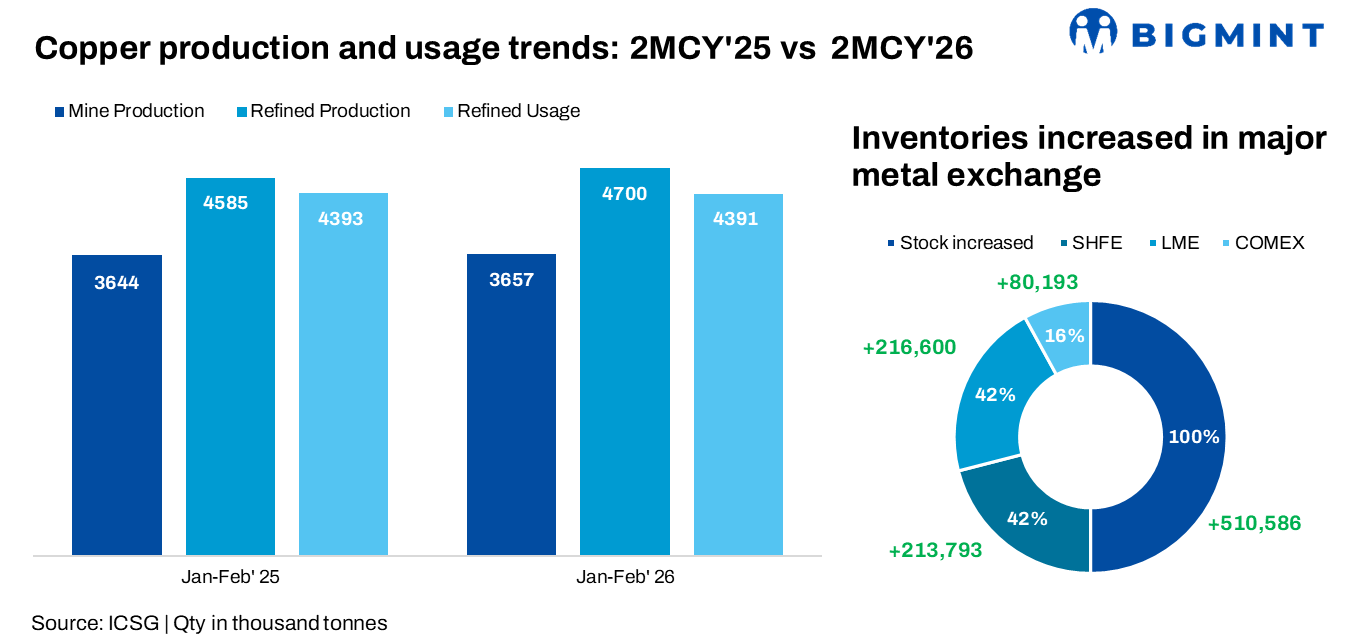

Global copper mine production increased marginally by ~0.4% in January-February 2026 compared to the same period in 2025, indicating a largely stable trend, despite a 0.2% decline in concentrate output. This was offset by a 2.5% increase in solvent extraction-electrowinning (SX-EW) production, supporting overall growth.

Growth was supported by higher output from Peru (+2.9%) and a sharp ramp-up in Mongolia (34%) due to the Oyu Tolgoi underground expansion. However, gains were partially offset by a 4% decline in Chile, alongside significantly lower output in Indonesia following disruptions at the Grasberg mine and reduced concentrate production in the DRC. The overall trend indicates that while new project ramp-ups are supporting supply, operational disruptions and regional declines continue to cap stronger growth.

Refined copper production edges up via secondary production

Global refined copper production increased by 2.5% in January-February 2026, showing a stronger supply response compared to mining output. This growth was largely driven by a 17% surge in secondary (scrap-based) production, particularly in China, while primary production saw a slight decline (-0.5%) due to smelter maintenance and lower concentrate availability in some regions.

China and the DRC together reported a 6.3% increase, reinforcing their dominance in global refined output, whereas production in Chile declined sharply (-8.6%) and Asia (ex-China) also saw lower output. India stood out with a 15% increase, supported by improved capacity utilization and refinery ramp-ups.

Refined copper usage remains unchanged

Global refined copper demand remained largely unchanged y-o-y in first two months of 2026, masking divergent regional trends. Demand outside China increased by 2.7%, reflecting relatively stable consumption across other regions. In contrast, Chinas apparent demand declined by 2%, primarily due to a sharp 49% drop in net refined copper imports. As China accounts for approximately 58% of global refined copper usage, this decline had a significant impact on overall global demand.

Consequently, the global refined copper market recorded a surplus of 0.3 mnt in JanFeb 2026, compared to a 0.19 mnt surplus in the same period of 2025, indicating a notable widening of the supply-demand gap.

Surplus widens as rising inventories signal demand weakness

Copper inventories across the three major exchanges climbed to 1,254,701 tonnes by end-March 2026, the highest level since January 2003. This marks a sharp increase of 0.51 mnt (+69%) compared to end-December 2025 levels, with stock builds observed across all exchanges-LME (+216,600 t), SHFE (+213,793 t), and COMEX (+80,193 t), highlighting continued accumulation of material amid subdued demand conditions.

At the same time, Chinas bonded stocks were estimated to have declined by ~8,000 t during the first two months of 2026 compared to year-end 2025 levels.

Prices soften slightly

The average LME cash price for March stood at $12,500/t, down 3.6% from February ($12,970/t). During the year, copper prices ranged between a high of $13,844/t and a low of $11,826/t, with the year-to-date average at $12,850/t, which is 29% higher than the 2025 annual average.

Market outlook

The global copper surplus widened in early 2026, driven by steady gains in refined production, particularly from secondary sources while demand remained subdued due to weaker Chinese imports. Despite modest growth in mine supply and stable consumption outside China, excess material continued to accumulate, pushing exchange inventories to multi-decade highs and indicating a clear shift of surplus metal into storage.

In the near term, copper prices are likely to remain range-bound, with downside pressure from elevated stocks balanced by expectations of future demand from energy transition sectors, until stronger physical consumption emerges to absorb the surplus.