Global billet prices weaken as China returns post holiday, Iran resumes supplies

...

- Chinese exporters lower offers amid weak domestic demand

- Iranian billet returns to key Middle East markets, adds supply pressure

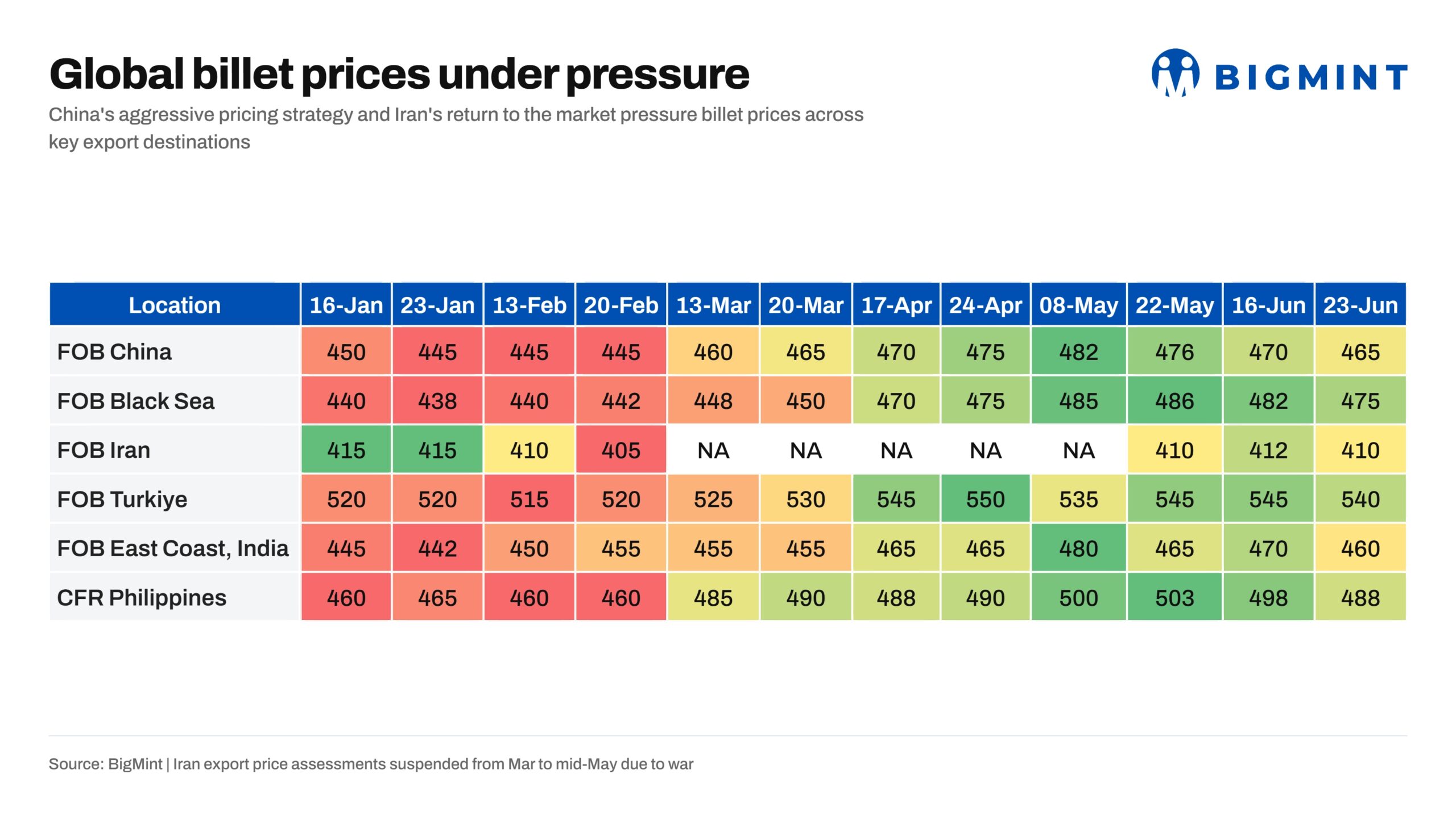

Global billet prices have come under renewed pressure over the past two weeks as Chinese mills stepped up exports following the holiday period, Iranian suppliers returned to the international market, and buying activity remained subdued across key importing regions.

The increase in export availability has pushed billet prices lower across Asia and the Black Sea, while buyers have largely deferred purchases in anticipation of further price declines. Easing freight rates have further enhanced the competitiveness of Asian exports, adding to the downward pressure on global billet prices and weighing on the outlook for other exporters, including India.

Chinese billet export offers have weakened further, with tradable levels increasingly discussed around $455/t FOB compared with prevailing offers of $460-465/t FOB. The decline follows a softer domestic steel market, where SHFE rebar futures have fallen by around RMB 30/t ($5/t) and the RMB has depreciated to about 6.8 against the US dollar since early June, improving the competitiveness of Chinese exports. Weak domestic demand has prompted mills to rely more heavily on overseas markets, while traders are also reported to be under pressure to cover short positions, adding further downside pressure to export offers. Market participants expect lower freight rates to further strengthen the competitiveness of Chinese cargoes.

Additional pressure has emerged from the Middle East following the return of Iranian suppliers to the export market. Iranian billet offers have resurfaced at around $470-475/t CFR Saudi Arabia, with three to four of the kingdom's five to six major billet consumers understood to be in discussions with Iranian suppliers. The return of Iranian material is expected to intensify competition in one of the region's largest billet import markets.

Southeast Asian billet prices have also retreated to below $490/t, compared with around $510/t two weeks ago, highlighting the broad-based correction across major export markets.

Elsewhere, activity in the Black Sea remains subdued, with only one billet transaction of around 25,000-30,000 t reported recently. Nevertheless, limited buying interest has pushed Black Sea FOB billet prices down to around $475/t from approximately $490/t one week earlier.

Outlook

The recent decline in billet prices reflects growing export competition amid subdued global demand. Chinese mills have maintained high operating rates despite weak domestic steel consumption, while the return of Iranian exports has added fresh supply to the market, intensifying competition across Asia and the Middle East.

Buyers have largely stayed on the sidelines, anticipating further price declines. In Turkiye, weak rebar demand has kept mills from booking deep-sea scrap cargoes, with many expecting imported scrap prices to ease further. Lower scrap costs could add another layer of pressure on billet prices by improving the economics of scrap-based steel production.

Weaker global market is also likely to weigh on Indian exporters. East Coast billet offers could slip below $465/t FOB as Indian mills compete with increasingly aggressive Chinese offers and the return of Iranian material.