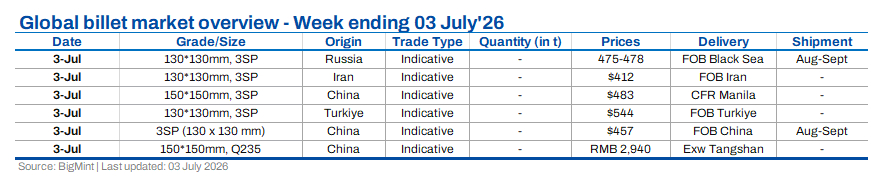

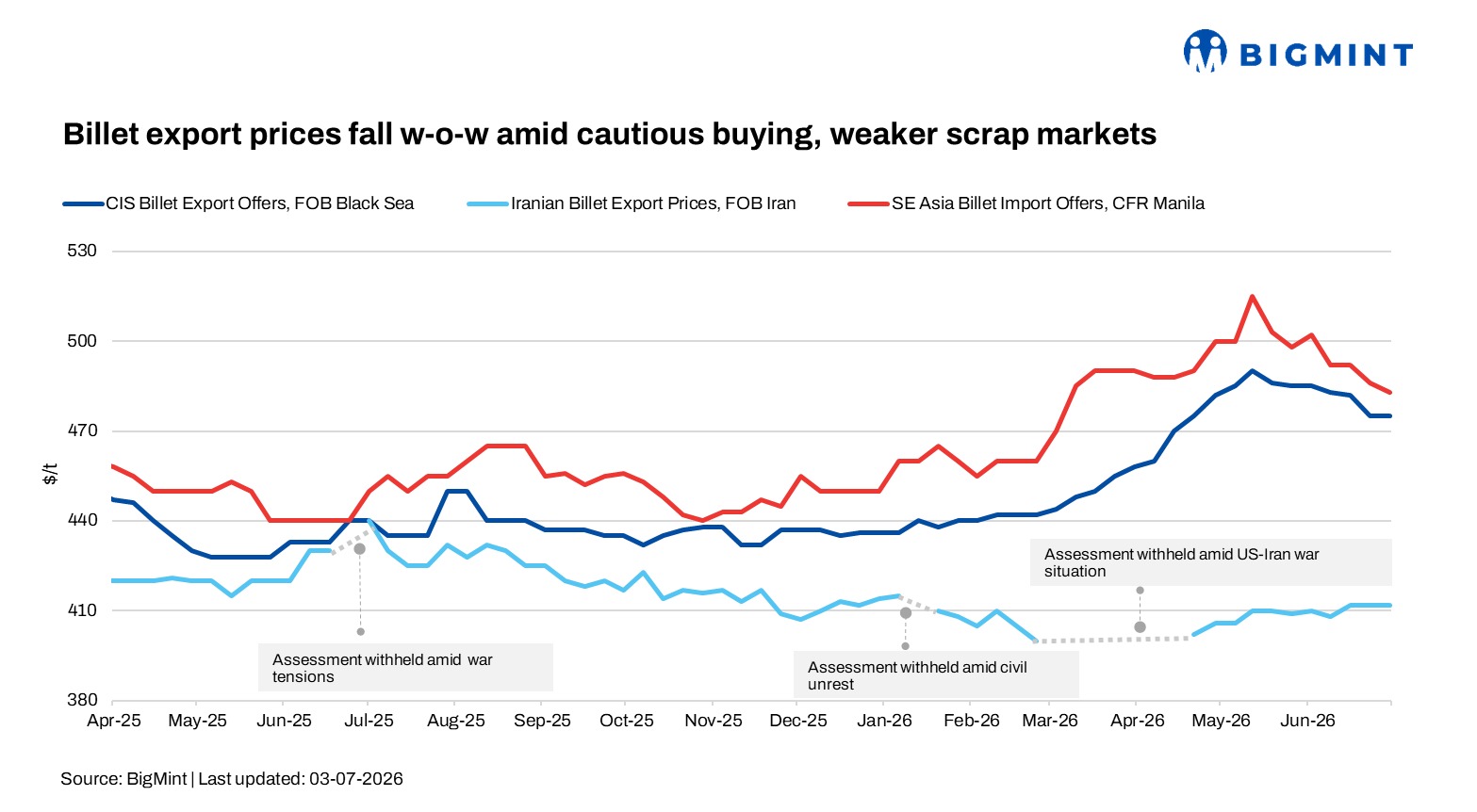

Global: Billet export prices fall w-o-w amid cautious buying, weaker scrap markets

...

- UAE buyers cautious over billet certification concerns

- Iranian export offers decline as buyers resist prices

Global billet markets remained under pressure during the week ended 4 July as weak downstream steel demand, softer scrap prices, and cautious buying sentiment continued to weigh on trading activity. Export offers declined across Asia, the CIS, and the Middle East region, with most buyers delaying purchases in anticipation of further price corrections. While supply constraints and raw material shortages provided limited support in markets such as Iran, overall sentiment remained bearish amid sparse transactions and persistent gaps between buyer expectations and seller offers.

Turkish deep-sea imported scrap prices also weakened during the week as sluggish finished steel demand and cautious mill procurement kept trading activity subdued. US-origin HMS 80:20 declined to around $375-378/t CFR Turkiye, while US East Coast HMS 80:20 export prices fell to $345/t FOB.

Domestic scrap purchase prices were cut by TRY 200-300/t ($4-6/t), but mills continued hand-to-mouth buying despite the scrap-to-rebar spread widening to $195-200/t. Export rebar offers remained stable at around $580/t FOB, while billet export prices were heard at approximately $540-545/t FOB, reflecting continued weakness across the Turkish steel market.

Asian billet market

Asian billet export prices extended their downward trend during the week as weak buying interest and expectations of further price declines kept most buyers on the sidelines. Chinese mills lowered 3SP billet offers to $455-457/t FOB for August-September shipment from $464-470/t FOB a week earlier, but the price reduction failed to revive demand.

Limited buying was reported only from the Philippines, where 10,000-15,000 t of Chinese billet was booked at above $480/t CFR. In Taiwan, seasonal rains continued to weigh on long steel demand, with Chinese billet offers easing to $480-482/t CFR, while buyers largely stayed out of the market in anticipation of further price corrections.

Chinese billet offers to Saudi Arabia also softened to $510-515/t CFR, down from around $520/t CFR a week earlier, although buying activity remained limited. Meanwhile, a major Indonesian producer reduced its September shipment offer by $10/t to $470/t FOB, but no transactions were reported.

In Malaysia, buyers indicated workable levels around $475-480/t CFR, while open-origin 5SP billet offers eased to $485-490/t CFR. Market participants expect Asian billet prices to remain under pressure in the coming weeks as sluggish downstream steel demand and expectations of further price declines continue to delay procurement decisions.

CIS billet market

The CIS and Turkish billet markets weakened further during the week as sluggish steel demand, falling scrap prices, and widening bid-offer gaps kept trading activity subdued. Russian export billet offers for August-September shipment declined to $475-478/t FOB Black Sea from $480-485/t FOB a week earlier, although buyers continued targeting lower levels in anticipation of further corrections.

CIS billet was offered to Turkiye at $495-505/t CFR, while Turkish buyers bid only $475-485/t CFR, resulting in no transactions. Russian billet was also indicated at around $535-536/t CFR Tunisia, but no deals were confirmed.

In Turkiye, buyers remained on the sidelines, expecting further declines in scrap and billet prices. Domestic billet offers were heard at $540-550/t exw, while market participants considered $530-535/t exw more workable. Attention remained focused on the expected reopening of Kardemir's billet sales, with prices anticipated around $515-520/t exw following recent rebar price cuts.

Import offers also failed to attract buyers, with Chinese billet at $510-520/t CFR and Indian billet at $475-480/t CFR. Market participants expect billet prices across the region to remain under pressure until finished steel demand shows signs of recovery.

Middle East market

The Gulf regional billet market remained subdued during the week as weak steel demand, electricity restrictions, and cautious buying continued to pressure prices across the region.

In Iran, export billet prices declined sharply to $405-412/t FOB, down from $415-420/t FOB a week earlier, as buyers resisted higher offers despite limited billet availability caused by electricity shortages and tight DRI supply.

Market participants indicated that most offers came from traders, while many mills withheld sales due to raw material shortages. Export activity is expected to improve after the recent holidays, with a 30,000 t billet cargo from the Khuzestan region reportedly sold at around $412-415/t FOB for July shipment. Easing payment restrictions have also encouraged Iranian suppliers to become more active in export markets, particularly for iron ore pellets.

In Saudi Arabia, one of the country's largest steelmakers raised domestic scrap purchase prices by SAR 140-145/t ($37-39/t) to support rebar prices despite weak seasonal demand. Meanwhile, billet prices eased to SAR 2,250-2,260/t ($600-603/t) exw, while smaller mills lowered rebar offers to SAR 2,400-2,430/t ($640-648/t) DAP. The market is now closely watching whether the benchmark producer maintains its official rebar price of SAR 2,932-2,935/t ($781-783/t) DAP.

In the UAE, billet prices remained stable at $520-530/t CFR for Chinese and Indonesian material. However, buying activity remained cautious as concerns over ECAS certification, material origin, and limited availability of certified billets continued to weigh on procurement decisions.