GCC: Emirates Steel lifts Jul'26 rebar prices even as Saudi billet market remains under pressure

...

- Emirates Steel lifts rebar prices for second consecutive month

- Saudi billet prices fall on weak rebar demand, aggressive mill competition

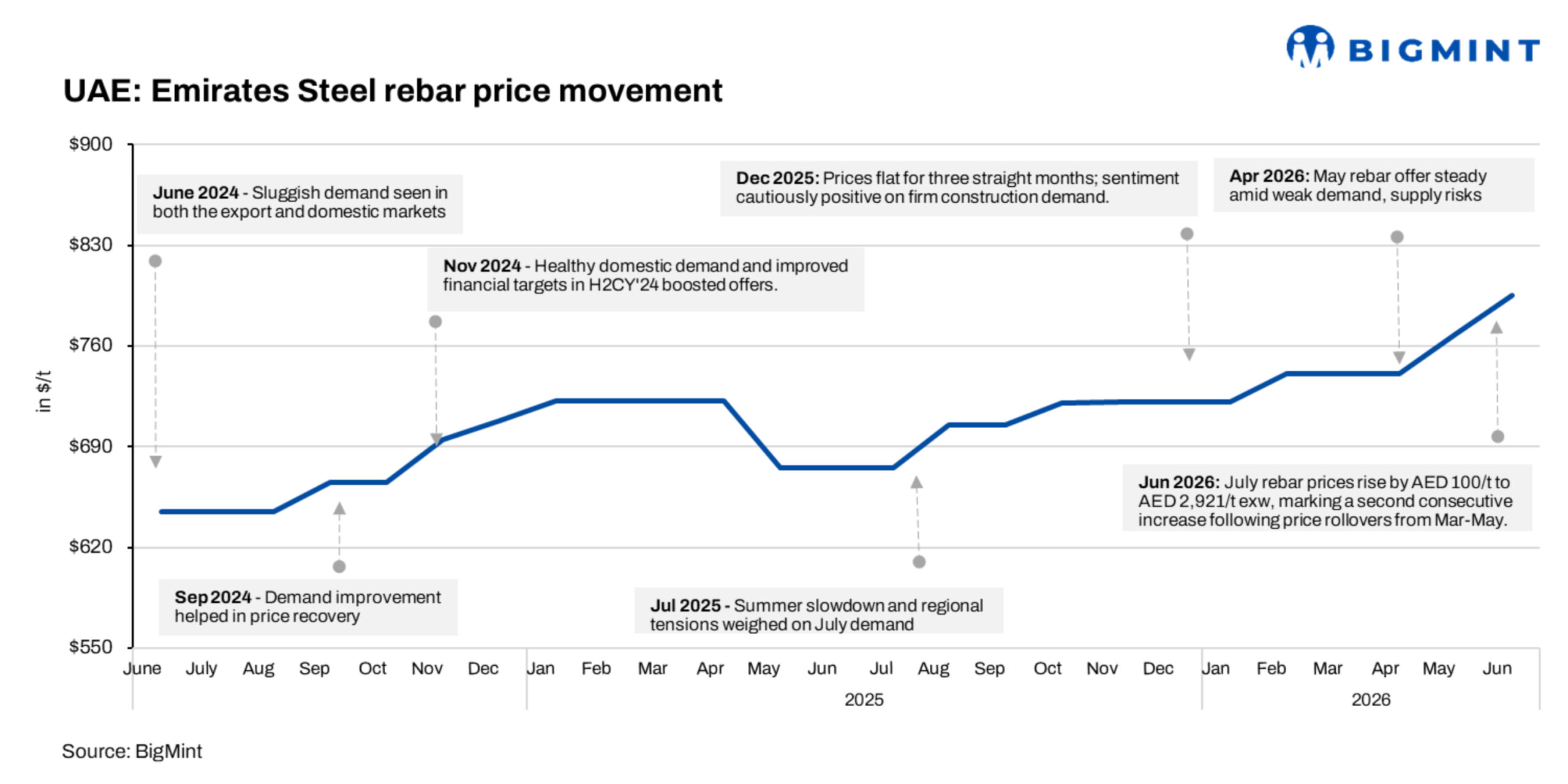

Emirates Steel has increased its domestic 12-32 mm rebar list prices by AED 100/t ($27/t) to AED 2,921/t ($789/t) ex-works for July rolling, marking a second consecutive increase following price rollovers between March and May. The latest adjustment signals improving sentiment in the UAE long-steel market, with the producer continuing to push prices higher despite mixed demand conditions across the wider GCC region.

In the UAE, domestic ferrous scrap prices strengthened modestly, with HMS (80:20) processed scrap assessed at AED 1,038/t ($283/t) DAP Abu Dhabi, up AED 11/t ($3/t) w-o-w. However, comfortable availability across most grades continued to prevent sharper gains.

Market participants noted that Turkish deep-sea scrap prices showed a downward movement, while regional buyers continued to monitor developments in China and coking coal markets for clearer direction.

Saudi billet market faces mounting pressure

In contrast, Saudi Arabia's billet market remains under pressure as sluggish rebar demand continues to weigh on domestic suppliers. Market participants assessed local billet prices at SAR 2,350-2,400/t ($611-624/t) exw, down around $40/t from the previous sales cycle.

Industry sources indicated that weak construction activity and cautious purchasing behaviour have intensified competition among rolling mills. As a result, some billet suppliers are reportedly offering discounts of up to SAR 50/t ($13/t) below prevailing market levels to reduce inventories and improve cash flow.

"Demand is very weak, and rolling mills are competing aggressively just to secure rebar orders," a Saudi trader source said.

Import billet retains niche demand

Despite the weakness in domestic billet prices, imported material continues to attract interest from selected producers involved in project-specific requirements.

Market participants reported that a Saudi buyer is currently working to finalise a purchase of around 30,000 t of Indonesian billet for August shipment at approximately $555-560/t CFR Saudi Arabia.

According to industry sources, imported billet is typically preferred for projects requiring specific approvals, customer specifications, or commercial arrangements that make overseas sourcing more attractive than domestic supply.

Rebar market remains highly competitive

The challenging billet environment reflects broader weakness in Saudi Arabia's rebar segment. Rebar prices were reported at SAR 2,600-2,700/t ($676-702/t) delivered, with buyers continuing to purchase only for immediate requirements.

At the same time, Hadeed maintained its official rebar prices unchanged at SAR 2,930/t ($762/t) delivered. The price gap between Hadeed and smaller producers has widened to around SAR 300/t ($78/t), highlighting intense competition within the market as mills struggle to protect market share.

Outlook

Market conditions across the GCC remain mixed. While Emirates Steel has successfully implemented a second consecutive rebar price increase, Saudi Arabia's billet market continues to face pressure from weak downstream demand and aggressive competition among rolling mills. Unless construction activity improves meaningfully, domestic billet suppliers are likely to remain under pressure, while competitively priced imports could continue to limit any near-term price recovery.