Ferrous scrap to anchor India's rising metallics demand as steel capacity expands

...

- Steel production growth lifts metallics requirements

- Scrap demand rises 17% y-o-y, accounting for 1/4th of metallic mix

- Import dependence to persist despite higher domestic generation

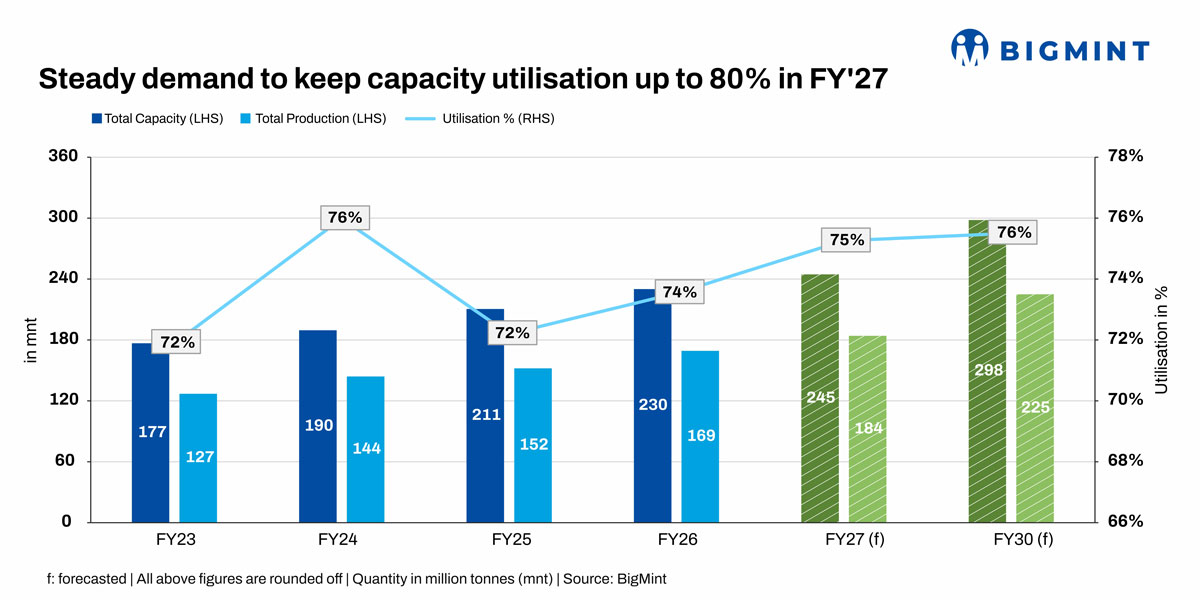

Morning Brief: India's steel industry is entering a phase of significant capacity expansion, with steelmaking capacity projected to increase from 230 million tonnes (mnt) in FY26 to 298 mt by FY30, an addition of nearly 68 mnt. This expansion is being driven by ongoing investments from major steel producers and the government's long-term vision of achieving 300 mnt of steelmaking capacity by 2030.

While crude steel production is also expected to grow steadily-from 169 mnt in FY26 to 225 mnt in FY30, adding around 56 mnt-the pace of capacity addition is slightly higher than production growth. As a result, capacity utilisation is projected to remain broadly stable at around 75-76%, indicating that demand growth is largely absorbing the new capacities coming online.

The sustained utilisation level suggests a balanced expansion cycle, where steelmakers are investing ahead of anticipated demand from infrastructure, construction, manufacturing, and automotive sectors. This also provides sufficient headroom for future production growth without creating excessive supply-side pressure in the market.

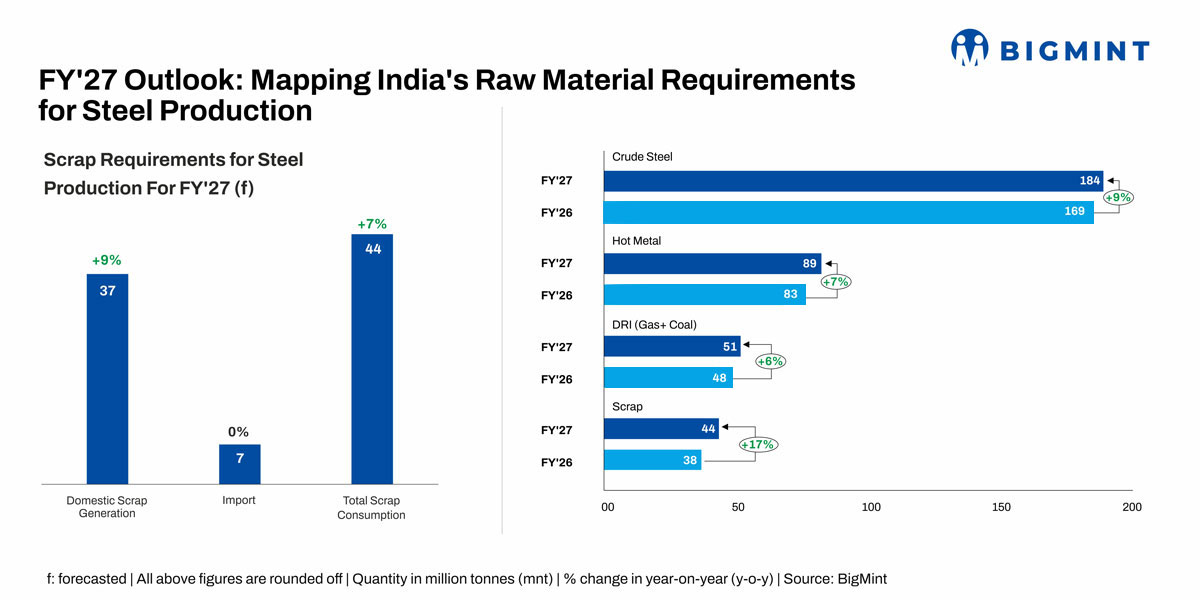

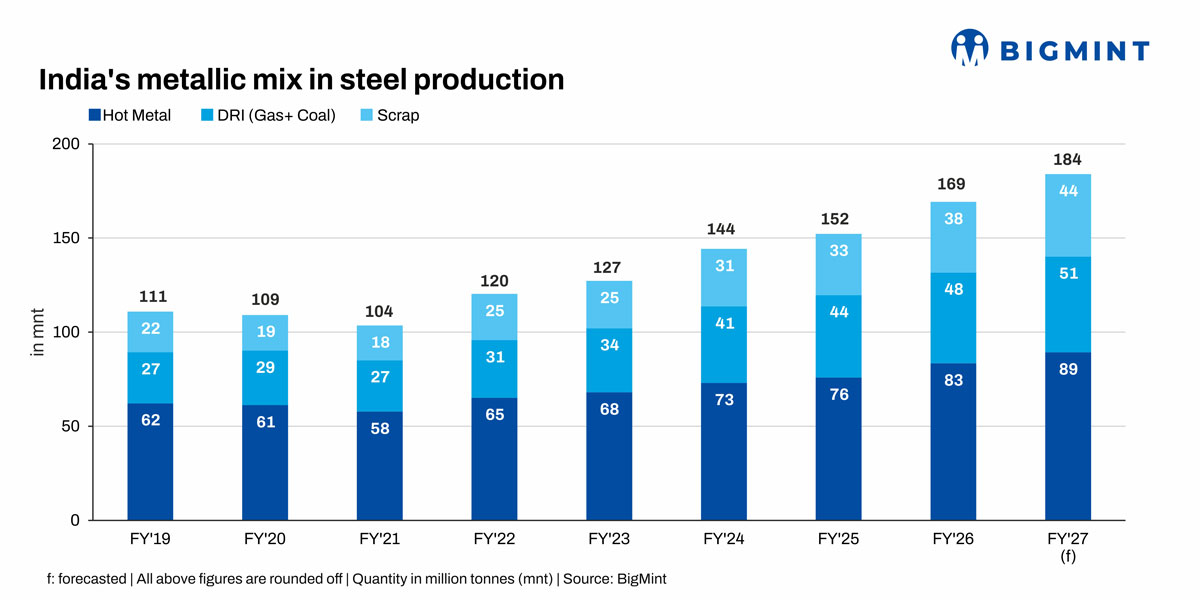

India's crude steel production is projected to increase from 169 mnt in FY26 to 184 mnt in FY27, requiring an additional 15 mnt of metallic inputs within a single year. The growth is supported by increases across all major metallics: hot metal rises from 83 mnt to 89 mnt (+6 mnt), DRI from 48 mnt to 51 mnt (+3 mnt), and scrap from 38 mnt to 44 mnt (+6 mnt).

Notably, scrap contributes nearly 25% of the incremental metallic requirement, matching the contribution of hot metal despite its smaller base. This indicates that as steel production expands, steelmakers are increasingly relying on scrap alongside traditional iron-bearing materials.

The FY27 metallic mix highlights the growing strategic importance of scrap in India's steelmaking sector. Of the total 184 mnt metallic requirement, scrap accounts for 44 mnt (24%), compared to 38 mnt (22%) in FY26.

The increasing share of scrap reflects the expansion of EAF/IF steelmaking capacity, rising focus on cost optimisation, and long-term decarbonisation efforts. The data suggests that India's steel growth is not only boosting overall metallic demand but is also structurally strengthening the demand outlook for ferrous scrap.

What does this mean for scrap market?

India's growing steel production will continue to drive higher scrap demand. In FY26, domestic scrap generation was estimated at 34 mnt, while imports contributed around 7 mnt, taking total scrap consumption to 41 mnt. In FY27, domestic scrap availability is projected to increase by about 9% y-o-y to 37 mnt, supported by improved collection efficiency, rising vehicle scrappage, and expanding processing infrastructure. Scrap imports are expected to remain broadly stable at around 7 mnt, resulting in total scrap consumption of 44 mnt.

This means that to support the production of 184 mnt of crude steel in FY27, India will require 44 mnt of scrap, making it one of the fastest-growing metallic inputs in the steelmaking value chain. While domestic generation is increasing, it may not be sufficient to fully meet the rising demand, keeping India dependent on imported scrap.

The widening gap between steel production growth and domestic scrap availability underscores the need for stronger recycling infrastructure, greater formalisation of scrap collection, and continued import support to ensure adequate metallic supply for the steel industry.

Every 1 tonne increase in steel production strengthens India's need for both domestic scrap generation and imported scrap, supporting a structurally positive long-term outlook for the ferrous scrap market.

Challenges with imports

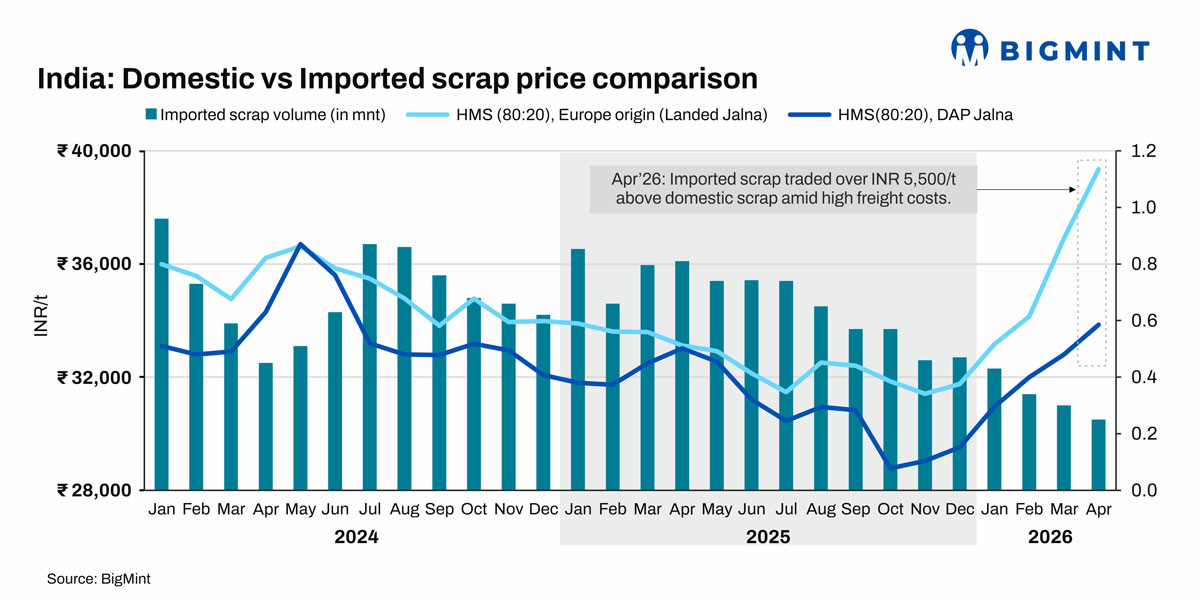

While domestic scrap availability is projected to improve, the imports face several challenges, including freight volatility, currency fluctuations, geopolitical uncertainties, and changing export policies from key supplying countries. These factors are expected to shape near-term procurement strategies and price trends in the imported scrap market.

Over the past two years, India's imported scrap volumes have generally declined, while import prices have become increasingly volatile due to fluctuations in freight rates and global market conditions. A notable example was April 2026, when imported HMS commanded a premium of over INR 5,500/t compared to domestic scrap, prompting mills to reduce import purchases and prioritise local sourcing wherever feasible.

This highlights a broader shift in the market: procurement decisions are now driven primarily by landed cost economics rather than traditional sourcing preferences. As buyers become increasingly cost-conscious, the competitiveness of imported scrap remains a key factor influencing trade flows and purchasing strategies.

Relative economics of scrap and DRI

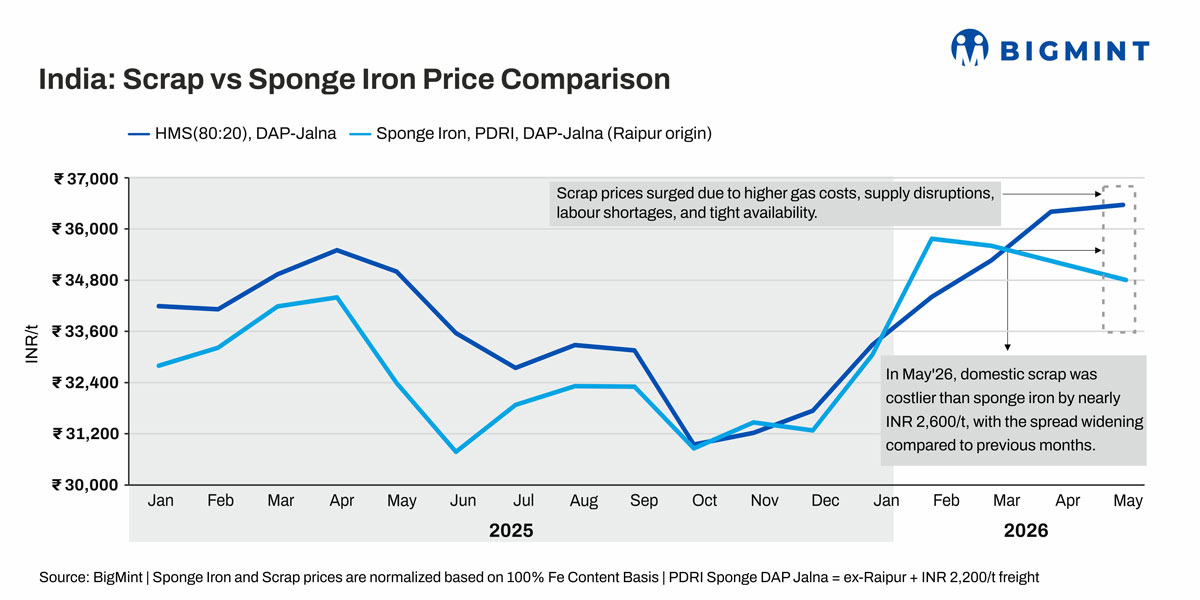

Steelmakers have increasingly shifted towards sponge iron (DRI) consumption since the beginning of FY27, driven by the relative cost advantage of DRI over scrap. This trend was largely influenced by supply-side challenges in the scrap market, including higher gas costs, West Asia-related supply disruptions, labour shortages, and tight scrap availability, which pushed scrap prices sharply higher.

During Jan-May CY'26,HMS (80:20) scrap prices rose by INR 3,200-3,300/t (+9-10%), compared to an increase of only INR 800-850/t (+3%) in sponge iron prices. As a result, the price differential widened significantly from a scrap premium of INR 200-250/t in January'26 to INR 2,600-2,700/t in May, making sponge iron a more economical option for steelmakers.

Looking ahead, the spread may narrow modestly as scrap supply conditions improve and prices ease. However, sponge iron is expected to retain its cost advantage in the near term, encouraging mills to maintain a higher DRI share in their metallic mix.

Outlook - FY27 and beyond

India's scrap demand outlook remains structurally positive, supported by rising steel production, expanding EAF/IF capacity, and increasing emphasis on decarbonisation and circular economy practices. Domestic scrap generation is expected to improve steadily; however, it is unlikely to fully meet the growing demand, keeping the market fundamentally supportive over the medium to long term.

In the near term, procurement decisions will be driven by relative metallic economics rather than volume requirements alone. With sponge iron currently offering a cost advantage over scrap, mills are expected to maintain a higher DRI share in their metallic mix. While improving domestic scrap availability may narrow the price spread, DRI is likely to remain a key competitor to scrap in the coming quarters.