EU steel demand growth to slow sharply in CY'26 despite easing import pressure

...

- Apparent steel demand growth forecast at 0.4% in CY'26 after import-led rebound

- Record import penetration eases, but production remains near historic lows

- Construction recovery offsets only part of manufacturing weakness

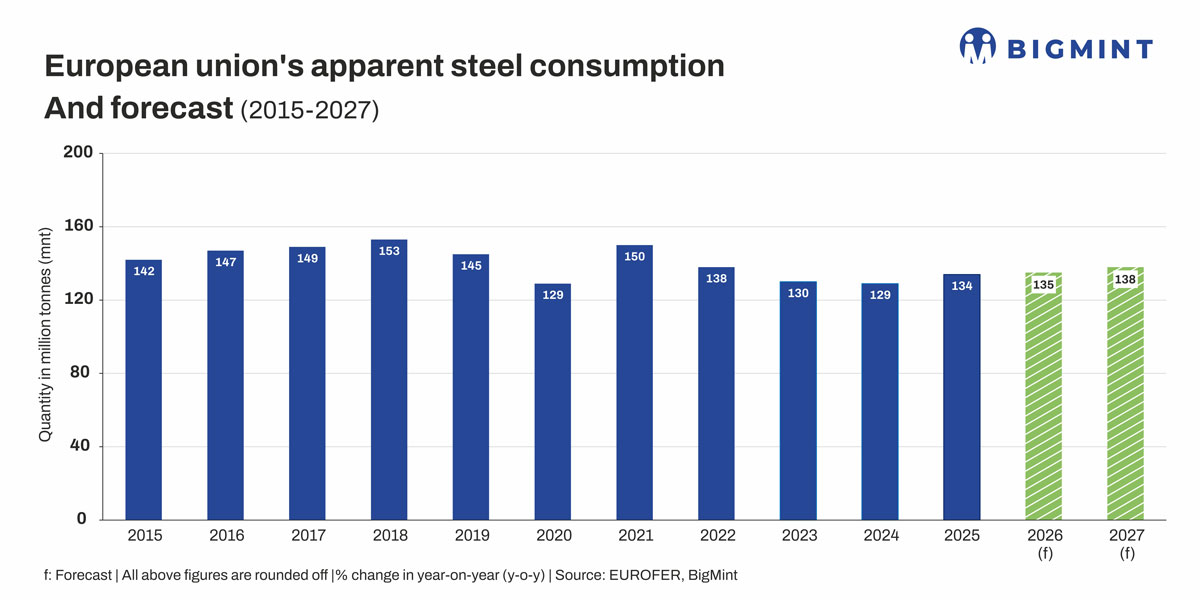

Morning Brief: EU steel demand growth is expected to slow sharply in CY'26 as the import-driven rebound witnessed last year gives way to weaker underlying market fundamentals, according to EUROFER's latest Economic and Steel Market Outlook. The industry association forecasts apparent steel consumption will increase by just 0.4% this year, compared with an estimated 4.4% growth in CY'25, when exceptionally strong imports during the second half inflated headline demand. While import pressure has begun easing and construction activity is gradually stabilising, weak manufacturing, subdued automotive production, elevated energy costs and persistent geopolitical uncertainty continue to weigh on the pace of recovery. Consequently, domestic steel production remains near historic lows despite improving apparent demand, highlighting the disconnect between headline consumption and underlying market conditions.

Import correction exposes underlying demand weakness

The sharp slowdown in apparent steel demand this year reflects the unwinding of the exceptional import surge witnessed during the second half of CY'25 rather than a sudden deterioration in market conditions. Record import arrivals last year lifted apparent steel consumption to an estimated 4.4% growth despite subdued manufacturing activity across the region. As imports normalise, apparent demand growth is expected to ease to 0.4% in CY'26, while steel demand remains around 10 mnt below pre-pandemic levels. The moderation suggests underlying steel consumption has yet to recover sufficiently to sustain stronger market growth without support from imports.

Import pressure eases, but mills remain cautious

Steel imports began correcting during Q1CY'26, with total imports declining 23% y-o-y and finished steel imports falling 17% after reaching record penetration during late CY'25. Imported steel accounted for 37% of apparent consumption in Q4CY'25, underscoring the scale of competitive pressure domestic producers faced entering the year. Although easing imports should improve the competitive environment, mills remain reluctant to increase production amid weak order books, subdued manufacturing activity and continued uncertainty over energy prices and trade policy. Turkey retained its position as the EU's largest steel supplier during Q1CY'26, while India was among the few major exporters to expand shipments into the bloc.

Construction stabilises, manufacturing recovery remains uneven

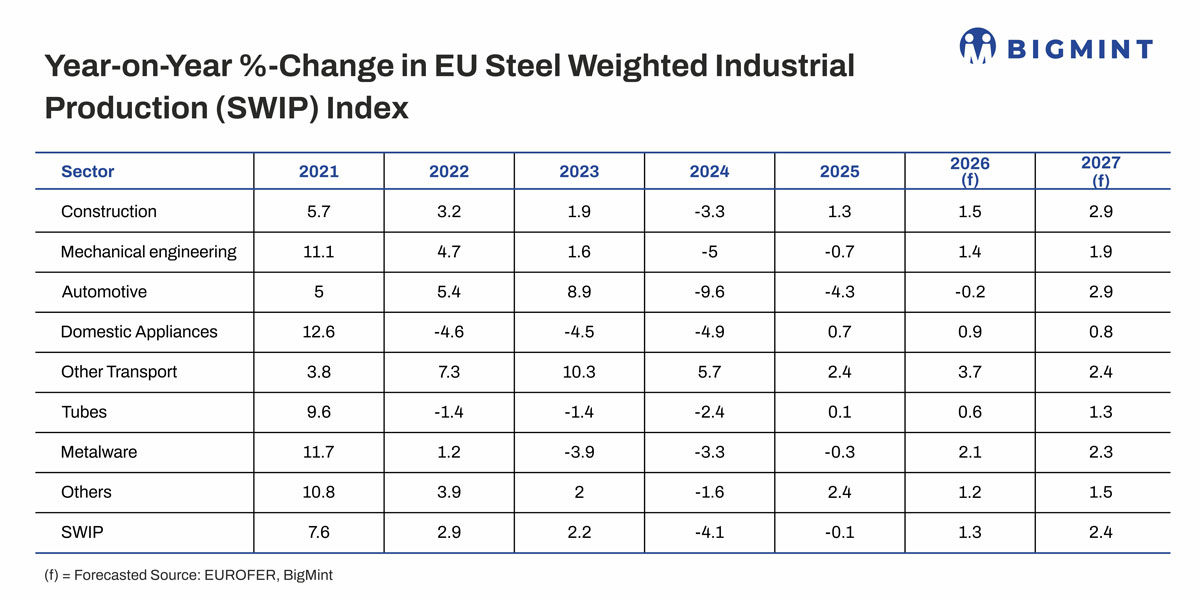

The recovery in steel-consuming sectors continues to lack breadth. Construction is forecast to expand 1.5% in CY'26 after several years of contraction, supported by easing inflation and lower financing costs. Mechanical engineering is expected to grow 1.4%, but automotive production is forecast to contract another 0.2%, delaying a broader industrial recovery until CY'27. Consequently, EUROFER expects Steel Weighted Industrial Production (SWIP) to increase by only 1.3% this year, indicating that manufacturing demand is improving only gradually despite stabilising construction activity.

Production recovery remains elusive

Domestic production continues to lag improvements in apparent demand. EU crude steel output declined 2.9% y-o-y to a historic low of 125.8 mnt in CY'25, while capacity utilisation averaged just 65.4% during Q1CY'26. Weak industrial activity, elevated operating costs and uncertainty surrounding demand have discouraged mills from restarting idled capacity, suggesting that lower imports alone will not be sufficient to drive a meaningful recovery in European steel production.

Outlook

The latest quarterly outlook suggests the European steel market is entering a slower phase of recovery after the import-led rebound of CY'25. Construction is expected to provide the principal source of demand growth during CY'26, but continued weakness in manufacturing and automotive production is likely to limit overall steel consumption. Although easing imports should reduce competitive pressure on domestic producers, elevated energy costs, geopolitical tensions and persistent uncertainty surrounding global trade continue to discourage higher capacity utilisation and fresh investment. As a result, European steel production is expected to recover more slowly than apparent demand, leaving the market dependent on a sustained improvement in industrial activity before a broader recovery can take hold.