EU releases country-specific steel quotas; lower HRC allocation to weigh on Indian exports

...

- Quotas allocated for 18.3 mnt of imports

- Total HRC quota a little over 5 mnt

The European Commission has published country-specific tariff-rate quotas for steel imports under its new Steel Regulation, effective from 1 July to 31 December 2026, which will replace the bloc's safeguard measures that had been in force since 2018.

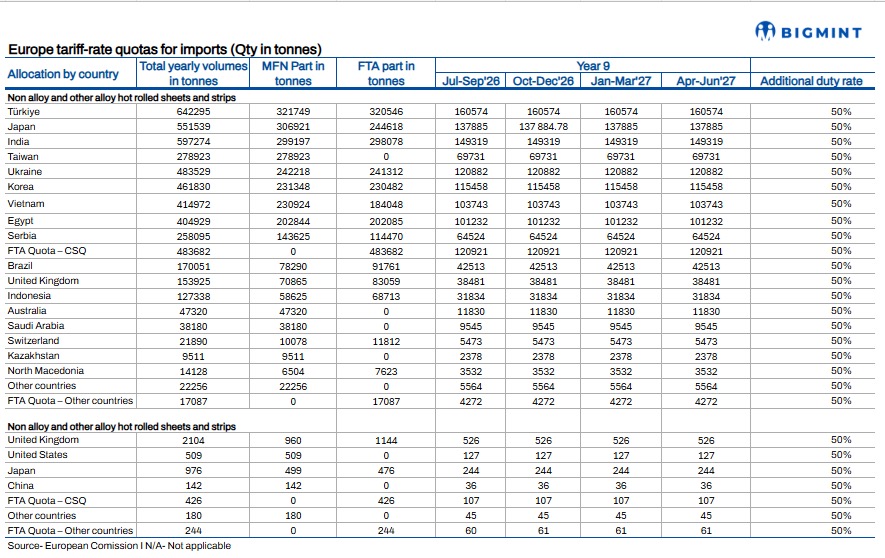

The latest implementing regulation allocates quotas for 18.35 million tonnes (mnt) of imports across 26 product categories based largely on individual countries share of EU imports during 2022-24 and defines how much steel these countries can ship into the European Union before attracting a 50% out-of-quota duty.

As announced earlier, under the new framework, the EU reduced total tariff-rate quotas by around 47% from the previous safeguard regime while increasing the duty on out-of-quota imports to 50% from 25%.

The measures were introduced in response to persistent global steel overcapacity, rising import pressure following higher US tariffs, and weak capacity utilisation across the European steel industry.

For Indian exporters, the allocations confirm a more restrictive trading environment. The tighter framework comes as Europe remains India's largest overseas steel market despite slowing demand and the rollout of the Carbon Border Adjustment Mechanism (CBAM).

Key features of new quota framework

The quotas are divided into two components: a Most Favoured Nation (MFN) allocation available to all eligible exporting countries and a separate Free Trade Agreement (FTA) allocation reserved for countries that have existing or future FTAs with the EU.

Within this structure, the Commission has introduced country-specific quotas, residual quotas, and additional FTA competition quotas. All quotas will be administered on a first-come, first-served basis, while exporters from FTA partner countries may access additional quota pools after exhausting their country-specific allocations.

Notably, Ukraine receives preferential treatment under the framework owing to its security situation and its previous preferential access to the EU market.

The regulation also introduces a more differentiated quota management system than previous safeguard arrangements. For the largest product category, hot-rolled sheets and strips, the Commission has created specialised quota structures to prevent excessive concentration of imports from a limited number of suppliers while maintaining diversified sourcing for European buyers. Existing arrangements governing steel movements into Northern Ireland from the United Kingdom have also been retained to ensure continuity of established trade flows.

Total Indian allocations fall, HRC exports face tighter limits

India has been allocated a definite volume of major flat steel products, including hot-rolled coil (HRC), cold-rolled coil (CRC), galvanised steel, and colour-coated products.

The reduction mirrors the broader contraction in the EU's import quota pool rather than a loss of India's market share.

The tighter quota regime comes at a time when the EU continues to account for the largest share of India's steel exports.

Although India's exports to the region declined y-o-y in 2025 amid weak European manufacturing activity, the second half of the year saw shipments rebound as buyers accelerated purchases ahead of CBAM implementation.

Hot-rolled coil remained India's largest export product to the EU at 1.30 mnt, followed by galvanised steel at 0.82 mnt and cold-rolled coil at 0.56 mnt.

Export growth to Europe likely to slow

The new quota allocations are expected to further limit India's ability to expand steel exports to Europe.

Unlike during CY'25, when Indian mills benefited from CBAM-related frontloading and competitive pricing, the smaller quota pool leaves limited room for additional shipments. The higher 50% out-of-quota duty also makes exports beyond allocated volumes commercially unattractive, particularly for commodity-grade HRC.

As a result, the EU is likely to become a market where Indian producers defend existing business rather than pursue volume growth. Exporters may increasingly prioritise higher-value coated and downstream products that can better absorb compliance and tariff costs, while limiting spot HRC sales once quarterly quotas begin to fill.

Mills likely to diversify beyond Europe

The tighter EU framework is expected to reinforce Indian mills' efforts to diversify exports

Several producers had already begun shifting HRC exports towards Vietnam during the second half of CY'25 as European demand softened and quota availability tightened. Markets in Southeast Asia, the Middle East, and Africa are also likely to receive greater attention, although their ability to absorb volumes comparable with the EU remains limited.

Outlook

The publication of country-specific quotas removes uncertainty over market access for the remainder of 2026, but it also confirms that export opportunities to Europe's largest steel market have narrowed.

For Indian producers, the challenge is no longer securing access to the EU but remaining competitive within a substantially smaller import quota, while simultaneously managing CBAM-related costs. With HRC exports facing the greatest pressure, mills are likely to focus on protecting established customer relationships in Europe while seeking incremental growth in alternative export markets, particularly Vietnam and the Middle East.