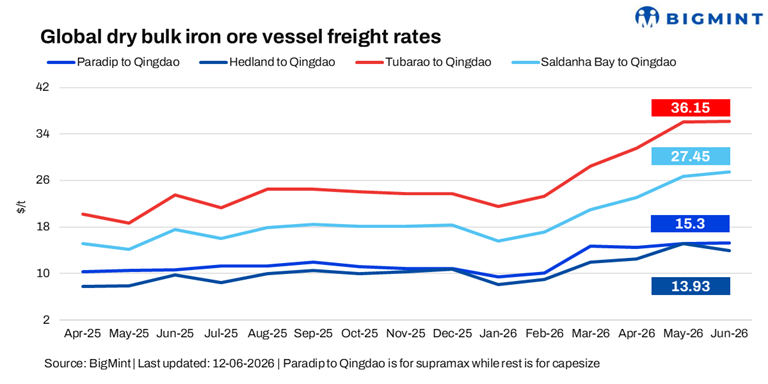

Dry bulk iron ore freights slide sharply w-o-w; Australia-India route hits 2-month low

...

- Muted Chinese demand, limited enquiries dampen sentiment

- Baltic Dry Index falls 10% w-o-w amid sustained Capesize weakness

Dry bulk iron ore freights fell during the assessment week ended 12 June, primarily due to subdued activity in the iron ore market. Limited enquiries on the India-China route reflected soft cargo demand, while the sharp decline in the Capesize segment underscored weaker iron ore trade flows. Australia-India route hits 2-month low amid fixtures at lower level, BigMint noted.

Cautious steel market conditions and muted raw material demand from China continued to weigh on freights, offsetting the relative resilience seen in smaller vessel segments and keeping overall market sentiment bearish.

A shipbroker stated, "Capesize sentiment remained soft on weak iron ore demand, Panamax showed signs of stabilising, while Supramax and Handysize stayed firm, supported by steady minor bulk cargo activity."

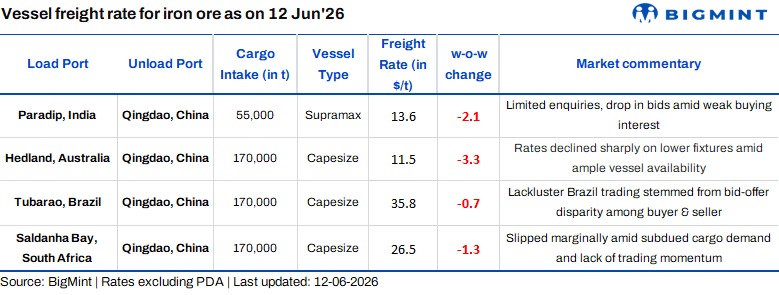

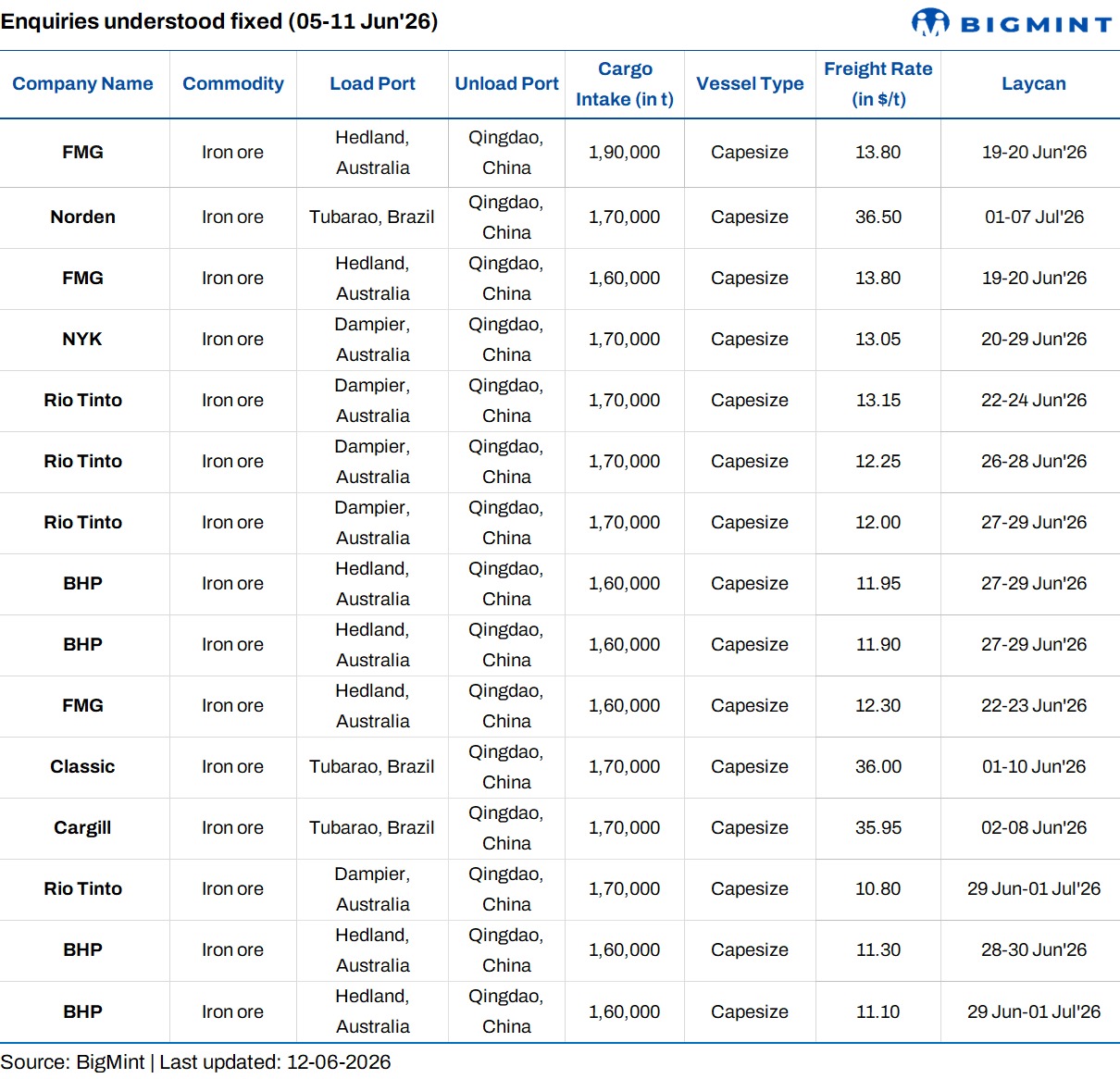

Route-wise update

Why are dry bulk iron ore freights under pressure?

- Baltic Dry Index (BDI) drops w-o-w: The BDI fell by 10.1% (308 points) w-o-w to 2,729 on 12 June, pressured by weaker Capesize sentiment. The Capesize index dropped significantly by 17.9% (900 points) to 4,140 amid softer iron ore demand, while the Supramax index rose by 3% (49 points) to 1,633, supported by steady minor bulk cargo activity.

- Bunker prices decrease w-o-w: Bunker prices fell by $79/tonne (t) w-o-w to $713/t as of 12 June, tracking the sharp decline in crude oil markets. Sentiment turned bearish as easing geopolitical tensions in the Middle East and growing expectations of improved oil supply reduced fuel price support, lowering voyage costs for shipowners.

- Brent crude futures drop w-o-w: Brent crude oil (August 2026 contract) was assessed at $87.11/barrel (bbl) on 12 June, down $7.89/bbl w-o-w. The decline was driven by expectations of improved oil supply from a potential US-Iran agreement and weaker demand prospects after Organization of the Petroleum Exporting Countries (OPEC) lowered its 2026 global oil demand growth forecast.

- DCE iron ore futures remain largely stable w-o-w: Iron ore futures on the Dalian Commodity Exchange (DCE) remained largely stable w-o-w at RMB 764/t ($113/t) on 12 June, reflecting balanced sentiment as steady steel demand offset concerns over softer buying activity and seasonal market weakness.

Outlook

BigMint learnt that monsoon conditions are expected to support higher iron ore freight rates, as iron ore fines -- classified as Group A cargo -- require stricter loading supervision during periods of elevated moisture.

Owners are expected to remain cautious in ensuring cargo moisture stays below the Transportable Moisture Limit (TML), given the safety risks associated with liquefaction and vessel instability.

Additional inspections, operational precautions, and potential loading delays may increase vessel turnaround times, prompting shipowners to seek higher freight premiums to offset the added risks and costs.