Daily round-up: LME base metals prices show mixed trends; oil supply recovery faces hurdles

...

- Hormuz reopening may release 700,000-t aluminium supply

- Ukraine strikes refinery supplying 40% of Moscow's fuel

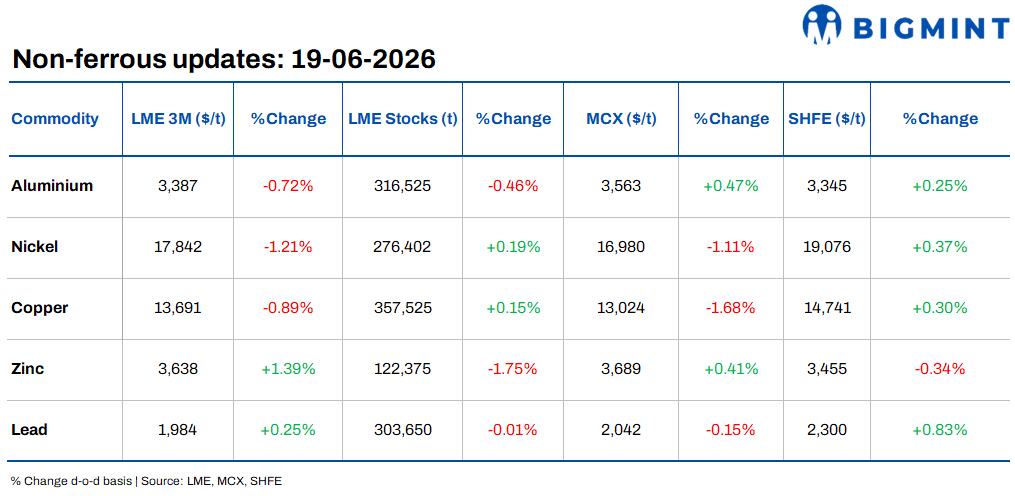

Base metals on the London Metal Exchange (LME) traded mixed on 19 June 2026, with zinc recording the strongest gain among major non-ferrous metals, rising 1.39% d-o-d to $3,638/tonne (t). Lead also edged higher by 0.25% to $1,984/t, while aluminium, nickel, and copper declined 0.72%, 1.21%, and 0.89% to $3,387/t, $17,842/t, and $13,691/t, respectively. The decline in copper and nickel reflected continued profit-booking after recent gains.

On the inventory side, trends remained mixed. Zinc stocks recorded the sharpest decline, falling 1.75% d-o-d to 122,375 t, followed by aluminium inventories, which dropped 0.46% to 316,525 t. Lead stocks also edged lower by 0.01% to 303,650 t. In contrast, copper and nickel inventories increased marginally by 0.15% and 0.19% to 357,525 t and 276,402 t, respectively. Despite the modest rise in copper inventories, overall exchange stock levels remain relatively tight by historical standards.

Domestic market overview

India's non-ferrous scrap market weakened further on 19 June amid softer global prices and cautious buying activity. Aluminium tense scrap (loose), ex-Delhi, declined by INR 2,500/t, or 0.85% d-o-d, to INR 290,500/t, while ex-Chennai prices fell by INR 2,000/t, or 0.68%, to INR 295,000/t.

Meanwhile, copper armature scrap (Cu 99%), ex-Delhi, dropped by INR 10,000/t, or 0.80% d-o-d, to INR 1,240,000/t. The decline reflected subdued downstream demand and softer sentiment in the domestic copper scrap market.

Oil prices remain volatile despite US-Iran agreement

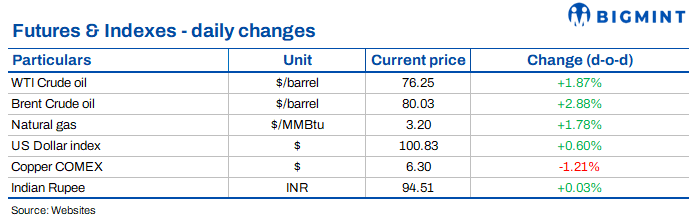

Global crude oil prices rebounded on 19 June 2026, although sentiment remained cautious despite the US-Iran memorandum of understanding aimed at reopening the Strait of Hormuz. Brent Crude rebounded 2.88% d-o-d to $80.03/bbl and WTI gained 1.87% to $76.25/bbl, but prices remain well below the peaks seen during the conflict. Since rising above $100/bbl in May, Brent has fallen more than 25%, reflecting the unwinding of geopolitical risk premiums and expectations of improving Middle Eastern supply.

However, the International Energy Agency (IEA) estimates that the Strait of Hormuz disruption removed around 14 million bpd from global supply, while global oil inventories have been declining at nearly 4 million bpd since late February. US crude inventories have fallen by more than 50 million barrels over the past nine weeks, and more than 500 vessels remain stranded in the Gulf awaiting clearance.

Analysts highlighted that global oil inventories have been significantly depleted following months of supply disruptions, and rebuilding both commercial and strategic stockpiles will likely support demand in the coming quarters. Goldman Sachs expects Brent crude to find support around $70-75/bbl, with prices likely to remain volatile until a more permanent resolution is reached and global inventories are replenished.

Other updates

Copper stocks make a comeback on AI-driven demand

Copper mining stocks have regained investor attention as rising demand from AI data centres and electric vehicles continues to strengthen the outlook for the metal. Companies such as Ero Copper and Southern Copper have benefited from expectations of robust copper consumption, with industry estimates suggesting that hyperscale AI data centres can use up to 50,000 t of copper per facility, compared to 5,000-15,000 t in conventional data centres.

Ero Copper reported first-quarter revenue of $263.2 million, more than double the previous year, while its full-year 2026 earnings are projected to rise 88%. Meanwhile, Southern Copper posted a 36% increase in quarterly sales to $4.25 billion. The strong growth outlook for AI infrastructure, power grids, and EVs continues to support bullish sentiment toward copper producers and the broader copper market.

Hormuz reopening could ease aluminium supply tightness in H2CY'26

The outlook for aluminium prices in the second half of 2026 has turned more cautious following the preliminary US-Iran agreement and the potential reopening of the Strait of Hormuz. Analysts estimate that up to 700,000 tonnes of delayed aluminium shipments could gradually return to the market, easing supply concerns that had driven LME aluminium prices to a four-year high of $3,855/t in early June.

LME aluminium inventories, which fell from around 509,000 t at the start of the year to nearly 320,000 t by mid-June, remain historically low, but improving logistics and the resumption of Gulf metal flows could help replenish stocks. While prices may face downward pressure as supply normalises, analysts expect inventory rebuilding and steady demand from energy, infrastructure, and transport sectors to provide underlying support to the aluminium market in H2CY'26.

Ukrainian drone strikes disrupt Moscow refinery operations

Ukraine launched another drone attack on Moscow, with several drones reaching the Moscow oil refinery, a facility that supplies around 40% of the Russian capitals petrol and oil products. The strike marks the second attack on the refinery this week, after an earlier incident forced a temporary halt in operations, adding to pressure on Russias fuel supply system.