China's steel industry continues to lag even as industrial output rises in Jan-May'26

...

- Property slump deepens as real estate investment falls 16.2% y-o-y in Jan-May'26

- Infrastructure investment slows to 0.6%, manufacturing investment slips into negative territory

- Steel exports rise in May, but trade barriers, Iran's export return cloud outlook

Morning Brief: China's industrial production rose in January-May 2026, but growth was concentrated in emerging sectors, while traditional drivers - most importantly, steel - continued to struggle.

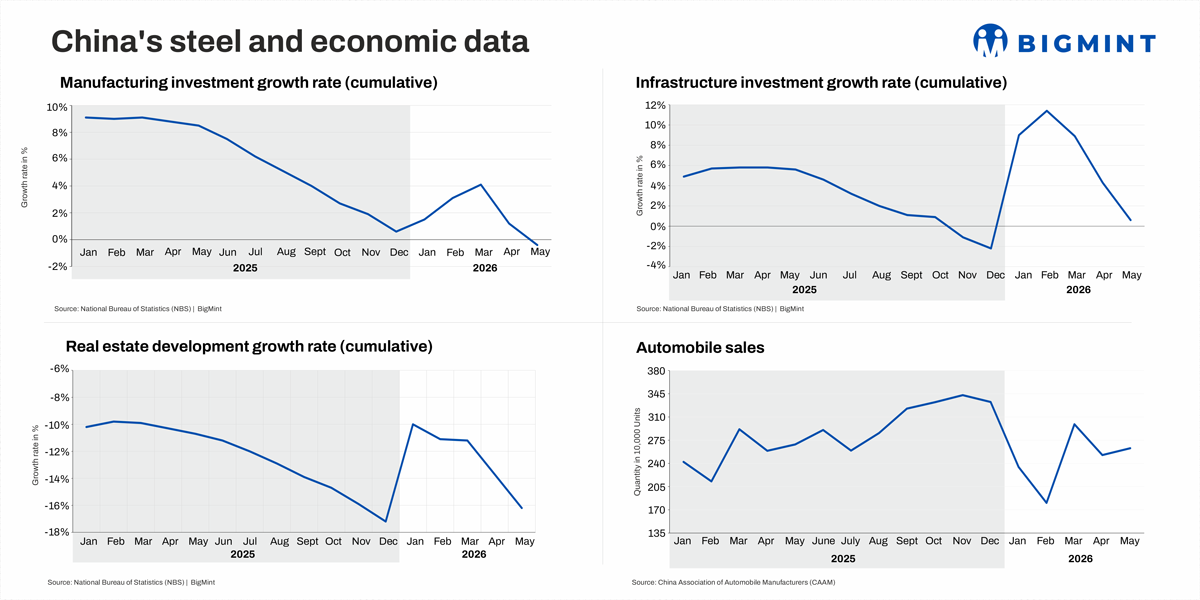

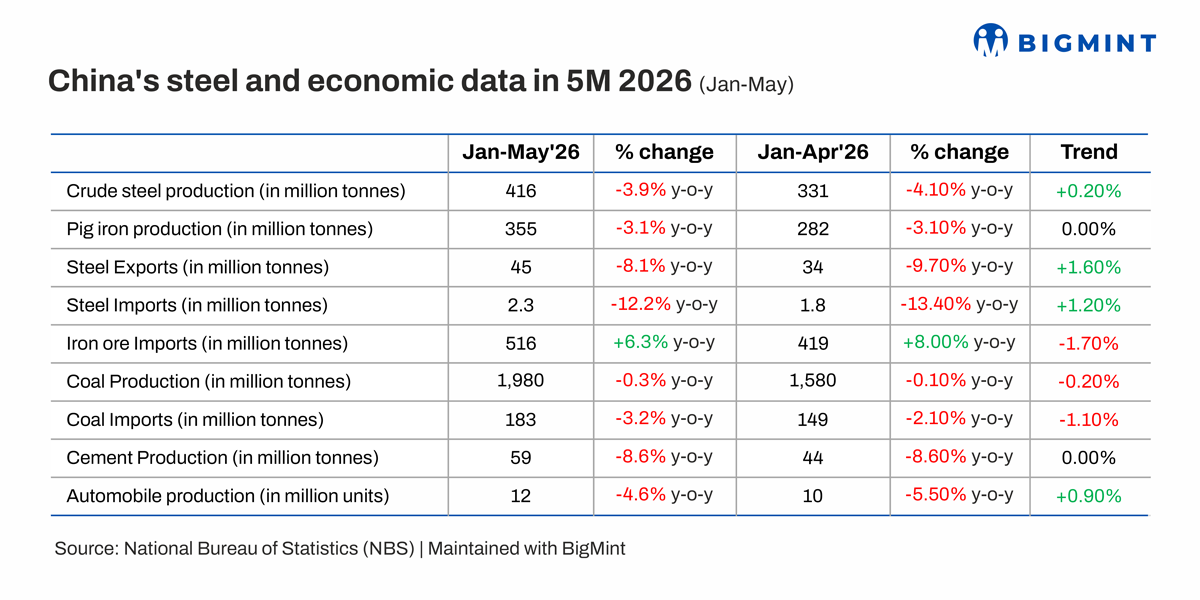

While overall industrial output grew 5.4% y-o-y during January-May, high-tech manufacturing expanded 13.1% and equipment manufacturing rose 9.5%, according to National Bureau of Statistics (NBS) data. In contrast, crude steel output fell 3.9% during the period, while real estate development contracted by 16.2% y-o-y and infrastructure investment growth slowed to 0.6%.

Overall manufacturing investment declined 0.4%, as consumer spending weakened. Retail sales contracted by 0.6% for the first time since December 2022, as the boost from consumer goods trade-in programmes that supported spending throughout CY'25 continued to fade and a high base effect amplified the slowdown.

The widening sectoral gap underscores a key challenge for China's steel industry: the sectors powering industrial growth today are significantly less steel-intensive than the property and infrastructure sectors that historically accounted for the bulk of steel consumption. Moreover, despite China's total exports reaching record highs in both April and May, weak domestic consumption continued to weigh on manufacturing momentum.

Highlights of China's steel industry in Jan-May'26

Crude steel production continues to fall: Chinese steelmakers continued to practice supply-side discipline in May, aligning production schedules with recent sales trends. Consequently, production fell 2.7% in May, while volumes were down by 3.9% in January-May.

However, China's crude steel production rose by a minor 0.9% m-o-m in May. The y-o-y drop was also softer than before. Consequently, the decline in cumulative volumes narrowed to 3.9% in January-May 2026 compared to 4.1% in January-April.

Although demand remained subdued, steelmakers maintained high operating rates as May is traditionally one of the strongest months for steel sales before activity slows from June amid the onset of the rainy season in southern China and extreme summer temperatures elsewhere. Production was also supported by positive sales realisations, with around 60% of surveyed steel mills remaining profitable in May, according to Mysteel, broadly in line with the level recorded a year earlier.

However, the share contracted slightly by the month-end as raw material costs surged but steel prices softened.

Steel exports fall 2% y-o-y but rise 9% m-o-m in May: Despite persistent trade barriers and tighter export controls, China's steel exports fell only 2.2% and rose 8.9% m-o-m to 10.34 million tonnes (mnt) in May as overseas buyers turned to Chinese suppliers to offset production disruptions elsewhere. The increase largely reflected orders placed in March and April, when steel production in parts of the Middle East came under pressure following the escalation of the US-Iran conflict, tightening the availability of semi-finished steel products in key import-dependent markets.

Overall finished steel exports fell by 8.1% y-o-y to 44.6 mnt during January-May amid tighter export licensing requirements and a growing number of trade remedy measures. Conversely, shipments of semi-finished steel products rose by 43.2% to 6.22 mnt, as billets and slabs faced fewer trade restrictions and benefited from supply disruptions in Iran.

Cautious steel market sentiment pulls down iron ore imports in May: China's iron ore imports fell 6% y-o-y in May, as steelmakers adopted a cautious procurement strategy despite maintaining relatively high production rates. With steel demand entering its seasonal slowdown phase and uncertainty persisting in the property sector, mills largely restricted purchases to immediate production needs and relied on existing port inventories. China's iron ore inventories at 34 major ports fell by 4 mnt m-o-m to 158 mnt in May, primarily driven by reduced port inflows.

However, imports remained higher by 6.3% y-o-y during January-May, supported by portside stockpiling of material amid continuing disputes between the China Mineral Resources Group (CMRG), the country's nodal authority for iron ore procurement, and some major overseas miners.

Coal production dips following fatal mine accident: China's raw coal production fell 1.7% y-o-y to 400 mnt in May, as intensified safety inspections and temporary mine suspensions following the fatal Liushenyu mine accident disrupted output in key producing regions, particularly Shanxi. The decline came despite steady demand from the power and steel sector, with a 4.2% increase in total power generation during the month. Fossil fuel-based power generation rose 2% y-o-y in May as wind speeds fell to a 10-year low across regions, curtailing renewable electricity output, according to the Centre for Research on Energy and Clean Air.

Meanwhile, China's coal and lignite imports declined 8% y-o-y to 33.27 mnt in May, with high import costs and regulatory uncertainty in Indonesia discouraging buyers.

Auto sector remains in slow lane but exports, NEVs emerge as bright spots: China's automotive sector remained under pressure in May as weak domestic demand and a high base effect due to last year's trade-in subsidies continued to weigh on production and sales, although the pace of contraction moderated from earlier in the year. Vehicle sales during January-May fell 4.2% y-o-y to around 12.2 million units, while domestic sales slumped 20.6%, driven by a sharper 24% fall in the conventional internal combustion engine vehicle segment. However, amid persistent domestic caution, exports remained a major source of support, with overseas shipments surging 63% y-o-y to 4.06 million units during the first five months of 2026. Strong overseas demand for new energy vehicles (NEVs) also helped offset domestic weakness, with NEV exports more than doubling y-o-y to 1.83 million units in comparison to a 16.5% drop in domestic sales.

Manufacturing investment softens amid prolonged slowdown: China's factory activity softened in May, with the official purchasing managers' index (PMI) at 50 points in May compared to 50.3 in April. The slowdown is also evident from the manufacturing investment growth rate slipping into negative territory this month, with the January-May 2026 value sliding to -0.40% y-o-y compared to 7.5% in the year-ago period and 4.1% in the first quarter of this year.

Among steel-intensive segments, while solar cell production fell 16.4% y-o-y during January-May, shipbuilding output declined by 20% y-o-y to 13.32 million deadweight tonnage (dwt), with the orderbook down 5.3% y-o-y. However, there was an 11.1% increase in the overall production of railway, ship, aerospace, and other transport equipment. Manufacturing of power generation equipment also increased moderately by 5.4%, while industrial robot output increased 28.1%.

The mixed performance indicates limited support to steel demand from manufacturing, with growth concentrated in a relatively narrow set of sectors.

Infrastructure investment slows amid weaker private spending on fixed asset creation: Infrastructure investment growth slowed sharply to 0.6% in January-May from 4.3% in January-April, dragged down by a 6.6% drop in construction and installation. This reflects a 7.1% drop in private spending on fixed asset creation, while government expenditure was marginally lower at 0.4%. Investment in road transport fell 5.7%, water conservancy investment declined 8.3%, and spending on public facilities dropped 3.2%, suggesting local governments became more cautious amid fiscal constraints and rising debt burdens.

Real estate crisis continues: China's property sector continued to deteriorate during January-May, with real estate development growth falling 16.2% y-o-y, extending the decline that started over four years ago. New housing starts dropped 22.6%, while floor space under construction fell 12.3%, highlighting the continued contraction in new project activity.

Property developers also remained under financial pressure, with funds raised for real estate development declining 19% y-o-y on year despite ongoing policy support measures.

Outlook

The divergence between industrial output and steel demand is likely to widen through the third quarter as China increasingly relies on high-tech manufacturing and export-oriented industries to offset weakness in traditional sectors facing overcapacity, weak profitability, and growing trade barriers. The decline in real estate investment and the contraction in manufacturing investment have eroded two of steel's key demand pillars. The weakness is particularly notable given that May is typically one of the strongest months for construction and manufacturing activity before seasonal disruptions from heavy rainfall and extreme heat emerge in June. This suggests that the recent decline in steel output may not yet have fully reflected underlying demand conditions. While mills are expected to continue targeting export markets to absorb surplus supply, the return of Iranian steel exports and the easing of geopolitical disruptions could reduce overseas demand for Chinese material, limiting the support seen in May. As a result, China's steel market is likely to remain characterised by persistent oversupply and pressure on producer margins.