China's crude steel production falls in Q1CY'26 as demand slowdown continues

...

- Real estate remains drag on steel demand, rebar output falls 12%

- Manufacturing, infrastructure activity recover but fail to offer support

- Shrinking profit margins, falling exports keep steelmakers cautious

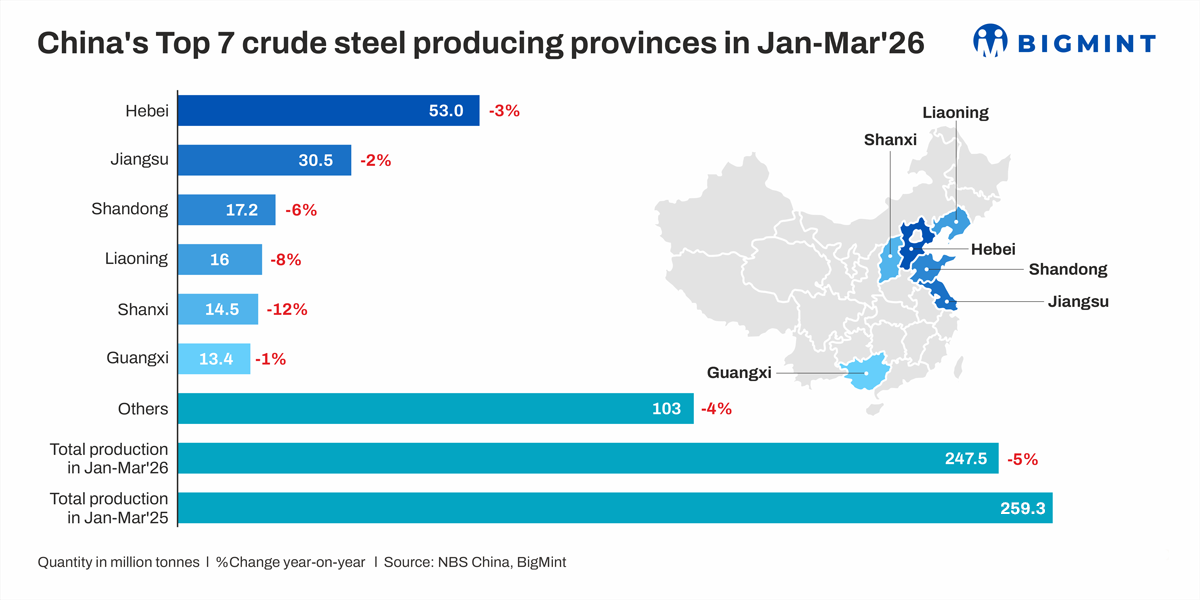

Morning Brief: China's crude steel production declined by 4.6% in January-March 2026 (Q1CY'26) to around 247 million tonnes (mnt), as per data maintained with BigMint. The worlds largest steel-producing nation continued to grapple with subdued demand amid the sustained downturn in the real estate segment, accounting for nearly half of steel consumption.

Region-wise trends

Region-wise trends show uneven performance across provinces. Northern and traditional steel hubs such as Hebei (-3%), Jiangsu (-2%), and Shandong (-6%) recorded declines, while sharper contractions were seen in Liaoning (-8%), Inner Mongolia (-14%), and Shaanxi (-13%), reflecting pressure on older and less efficient capacity. In contrast, southern and western provinces such as Guangdong (+3%) and Sichuan (+2%) witnessed moderate growth, supported by local demand and newer facilities. This divergence indicates a gradual geographic rebalancing of production, with capacity shifting towards more efficient and consumption-linked regions.

Factors influencing China's crude steel production

Steel demand remains lacklustre: Demand-side weakness remained the primary driver of the decline. Real estate investment fell 11.2% y-o-y in Q1CY26 and new construction starts dropped 20.3%, continuing to weigh heavily on steel consumption. Rebar production fell by 12.3% to 26.91 mnt.

Meanwhile, while manufacturing activity improved q-o-q, supported by policy stimulus and growth in high-end sectors, the 4.1% investment growth in Q1CY26 remained modest compared to year-ago levels (around 9%). Hot-rolled coil (HRC) production decreased by 8% y-o-y to 34.06 mnt.

Economic uncertainties, geopolitical tensions, and deflationary pressures have led Chinese consumers to limit discretionary expenses, which has curtailed domestic demand growth. For example, consumer expenditure on automobiles fell sharply by 9.1% y-o-y as tax subsidies shrank.

As such, even the manufacturing sector, which overtook construction to become the largest consumer of steel in CY25, failed to provide adequate demand support.

Infrastructure investment rose 8.9% y-o-y in Q1CY26, compared with 5.8% a year earlier, driven by front-loaded fiscal spending and major project execution with the start of the term of the 15th Five-Year Plan. However, such policy-led investment support was also not sufficient to reverse the broader slowdown in steel consumption.

Exports shrink: Steel exports, which had been the primary outlet for offloading excess supply, declined by a steep 9.9% y-o-y. Low-priced, non-VAT cargo supply contracted as the new export licensing system took effect, raising compliance burdens and administrative costs. Coupled with rising trade barriers, the higher prices discouraged importers, and the downtrend intensified in March, when the US-Iran conflict increased logistics costs and stalled movement through the Strait of Hormuz.

In fact, in March, China's total commodity exports grew 2.5%, its slowest pace in six months. Earlier, January-February had recorded a stupendous surge of 21.8% y-o-y.

Therefore, limited export momentum in both steel and derived commodities kept steelmakers wary about increasing production.

Mills struggle with profitability: Mills' profit margins remained narrow in Q1CY'26, dampening production enthusiasm. Only around 41% of mills were profitable in March, down from 53% a year earlier, according to Mysteel data cited by Reuters.

Additionally, as per Mysteel estimates, blast furnace (BF) mills faced average losses of RMB 33/t ($5/t) on rebars in March, widening from RMB 30/t ($4/t) in February and RMB 15/t ($2/t). On HRCs, losses declined to RMB 17/t ($2/t) in March from RMB 28/t ($4/t) in February but remained higher than Januarys RMB 9/t ($1/t).

Inventories remain elevated: Inventory levels remained high through the quarter, reflecting weak demand absorption and capping price recovery. To illustrate, steel inventories at key mills tracked by the China Iron and Steel Association (CISA) were 6-10% higher y-o-y during various phases between mid-February and early April. Inventories were 20-25% higher y-o-y in early to mid-January.

Capacity control efforts continue: Although no explicit directive has been issued by the government for reducing production, this quarter's decline follows from previous regulatory efforts to control overcapacity.

For example, the Work Plan for Stabilising Growth in the Steel Industry (2025-2026) targets value addition of around 4%, with a shift in focus from scale to high-quality development. In line with this, China has aimed to eliminate outdated, inefficient furnaces by imposing a 1.5:1 ratio for capacity swaps.

Outlook

BigMint expects China's crude steel production to continue declining through CY'26, though growth is likely during select periods, aligned with seasonal consumption trends.

While demand is expected to recover gradually, supported by infrastructure and high-end manufacturing, the ongoing weakness in real estate and traditional sectors will continue to weigh on overall steel consumption. Moreover, high inventories, weak realisations, and cost pressures are expected to limit any sharp rebound.

As per Chinese Research company, full-year production may come to 930 mnt, down 3% y-o-y. This is aligned with the World Steel Association's projections of a contraction in Chinese steel demand, though at a milder pace of 1.5% compared to CY'25's 5-7% (as per various sources), as the housing market correction nears its bottom.