China weekly: steel prices show mix trend amid seasonal headwinds and raw material support

...

- Rising raw material costs continue supporting steel prices.

- Soft downstream buying weighs on China's steel market.

China's steel prices show mixed trend in the week ended 12 June 2026. Chinese HRC prices dropped whereas rebar prices stable with the market facing a seasonal slowdown. On the raw materials front, prices of iron ore and coke prices stable, though billet prices increased w-o-w.

China's finished steel exports reached 10.341 million tonnes (mnt) in May'26, rising by around 840,000 tonnes (t) from April and surpassing the 10 mnt mark for the first time in five months, according to customs data. Although shipments remained 2% lower than a year earlier, the monthly recovery marked a notable improvement against the backdrop of weaker global demand and tightening trade restrictions.

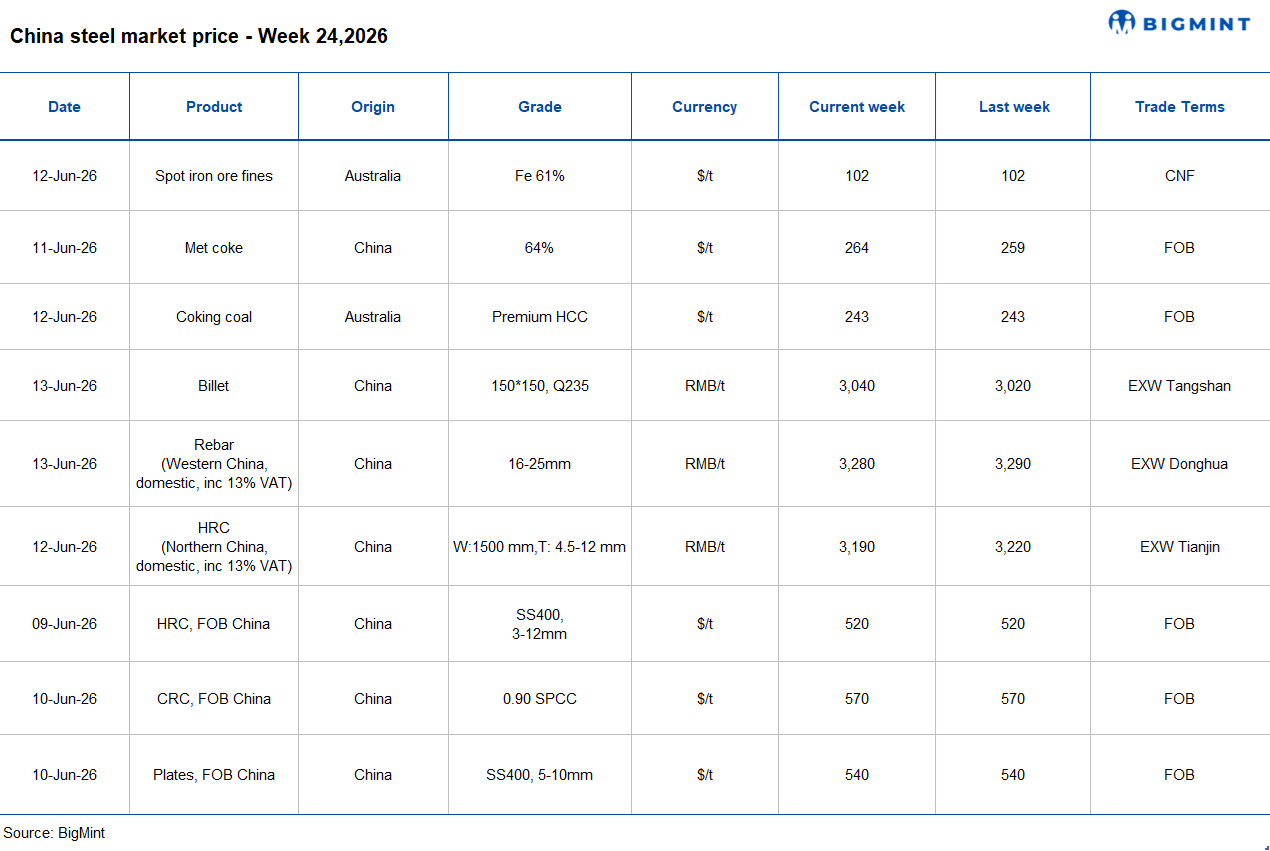

Iron ore spot prices remain stable w-o-w: Iron ore fines benchmark prices for Fe 61% remain supported w-o-w at $102/dmt CFR China on 12 Jun'26.

The market saw a mild technical rebound after prices had fallen to a more than three-month low, supported by the absence of fresh negative developments and easing concerns over coke supply disruptions following a recovery in Chinese coal mine output. However, gains remained limited amid weak steel demand in China, rising port inventories, and pressure on mill margins. As per reports, a marginal uptick in futures supported the marginal rise, while physical market activity slowed slightly due to weaker portside transactions.

a) Spot pellet premium steady w-o-w: Spot pellet premium for Fe 65% grade pellet stood at $19.45/t CFR China on 10 June.

b) Spot lump premium rose marginally w-o-w: Spot lump premium edged up w-o-w by $0.0065/dmtu to $0.1820/dmtu on 12 June.

Chinese demand and coal supply disruptions fuel global sentiment: China's strong procurement, tight coking coal supply, and mine restrictions have supported domestic coke prices, with the sixth price hike of RMB 55/t ($8/t) already implemented. High steel output, restocking, and low inventories have tightened supply-demand balance, raising expectations of further price increases and supporting global coke markets.

Australian Premium Hard Coking Coal (PHCC) prices remained stable w-o-w to $243/t FOB Australia. Combined with ongoing supply concerns in China and logistical challenges affecting Australian exports. In contrast, BigMint's coking coal index was assessed at $268/t CNF Paradip, India, on 12 June 2026, down $1/t w-o-w. Adequate inventories and weaker steel prices have limited aggressive coking coal buying from Indian mills.

Chinese billet prices edge up w-o-w: Chinese billet prices increased to RMB 3,040/t ($424/t) on 12 June from RMB 3,020/t ($421/t) at the start of the week, supported by firmer coke and iron ore prices, as well as stable mill profitability. However, gains remained limited due to seasonally weak steel demand, rising inventories, and cautious trading activity.

Most domestic steel prices saw only minor adjustments during the week, with mills largely maintaining production levels.

Chinese billet export offers remained largely stable, with overseas demand showing little improvement. Leading mills kept offer levels unchanged, while export activity remained slow amid limited buying interest and increasing competition in the semi-finished steel market. Some large-volume billet shipments to Europe were reported, although overall export sentiment remained subdued.

Domestic HRC prices decrease w-o-w: Chinese HRC prices decreased by RMB 30/t ($4/t) w-o-w to around RMB 3,190/t ($472/t) on 12 June from RMB 3,220/t ($477/t) from the previous week. Moreover, SHFE HRC futures (October 2026 contract) edged down by RMB 4/t ($0.5/t) w-o-w to RMB 3,374/t ($499/t) from RMB 3,378/t ($500/t) a week earlier. Meanwhile, China's HRC export offers stood at around $520/t FOB Rizhao, stable w-o-w.

China's HRC market remained range-bound from 8-12 June. While a modest uptick in raw material costs provided some stability, price declines continued at a slower pace. The market remains pressured by the traditional off-season, with sluggish demand particularly in construction and elevated mill inventories reinforcing a soft fundamental outlook.

Chinese steel export prices remained largely stable this week, with a slight downward bias observed this week in the market.

Rebar prices decrease w-o-w: Rebar prices in China were down by RMB 10/t ($1/t) w-o-w to around RMB 3,280/t ($485/t) as on 12 June, compared with RMB 3,290/t ($486/t) in the previous week. However, SHFE rebar futures (October 2026 contract) also inched up by RMB 13/t ($2/t) w-o-w to RMB 3,173/t ($469/t) as on 12 June from RMB 3,160/t ($467/t) a week earlier.

The rebar market remained mildly volatile during the week, with demand continuing to soften due to seasonal summer factors that slowed construction activity. Weaker downstream consumption limited inventory movement from mills to traders, resulting in a fresh build-up of steelmakers' rebar and wire rod stocks despite a moderation in production levels. However, firm raw material costs provided strong support to prices, preventing any fluctuations.

China's Shagang Steel has kept its long steel prices unaltered for mid-June'26 sales amid subdued domestic demand and slower trade activities in the region. Prices of rebars, coiled rebars, and wire rods are as follows:

- Rebars (16-25 mm): RMB 3,400/t ($502/t)

- Coiled rebars (8-10 mm): RMB 3,530/t ($521/t)

- Wire rods (6-10 mm): RMB 3,440/t ($508/t)

Outlook

China's steel market is expected to remain range-bound in the near term. Seasonal weakness in construction and manufacturing demand will continue to weigh on consumption and keep inventories elevated. However, firm raw material costs are likely to provide cost-side support and limit downside risks. Therefore, the domestic HRC market price is likely to continue its range-bound trading pattern next week, while export demand may remain subdued amid intense global competition.