China weekly: Steel prices extend decline amid seasonal demand slowdown

...

- Australian PHCC holds firm despite subdued spot buying.

- Shagang steel maintains long steel prices unchanged for early July.

China's steel prices show downward trend in the week ended 3 July 2026. Chinese HRC and rebar prices dropped with the market facing a seasonal slowdown. Furthermore, on the raw materials front, prices of iron ore and billet prices dropped w-o-w.

Raw material prices

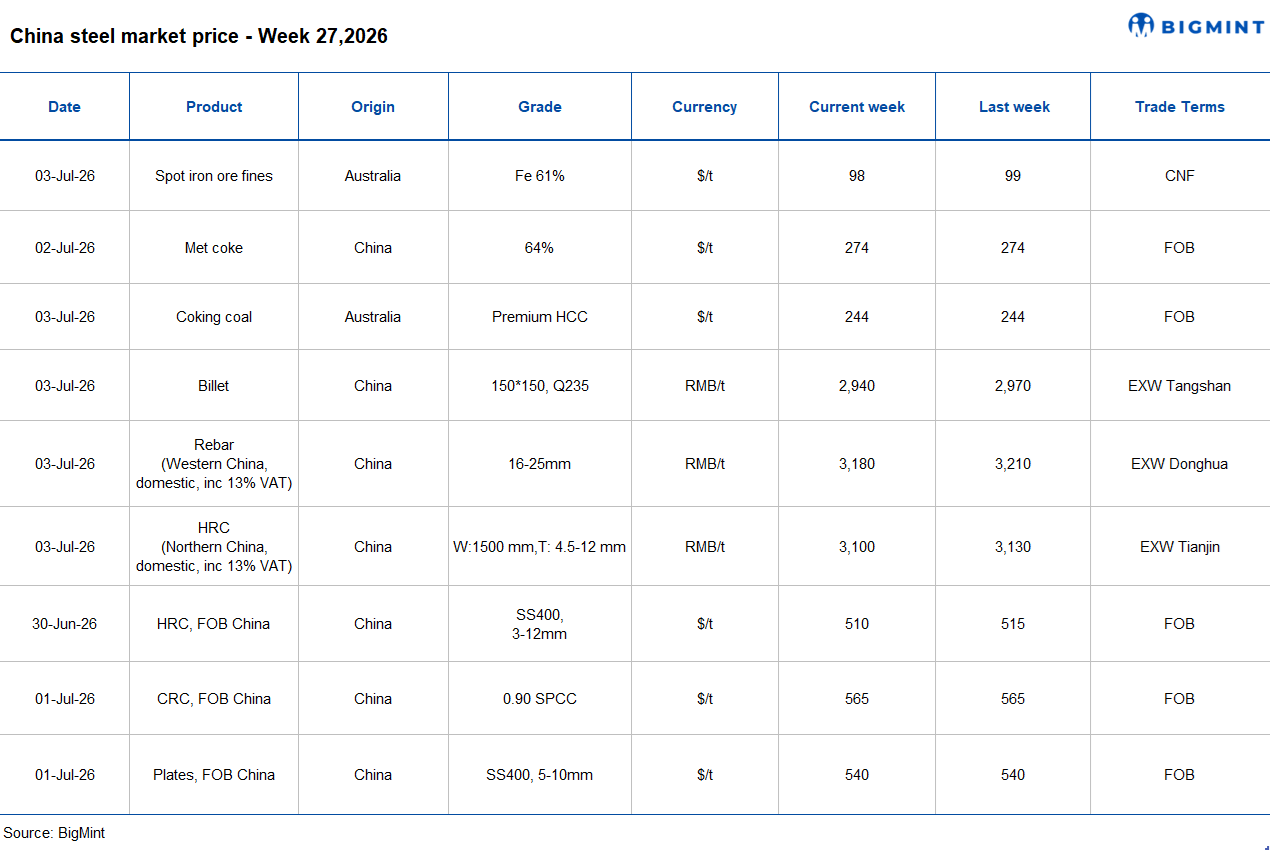

Iron ore spot prices drop w-o-w: Iron ore fines benchmark prices for Fe 61% decline w-o-w by $1/t w-o-w to $98/dmt CFR China on 3 Jul'26.

The decline in iron ore prices was primarily driven by mounting pressure on mills' margins following the ninth round of coke price hikes, which led many mills to adopt a cautious procurement approach. Additionally, the traditional seasonal slowdown in China's steel market continued to weigh on sentiment. Persistent rainfall across key construction regions disrupted project activity and weakened steel consumption, keeping finished steel prices under pressure.

a) Spot pellet premium rises w-o-w: Spot pellet premium for Fe 65% grade pellet gained by $3.05/t to $22.65/t CFR China on 1 July.

b) Spot lump premium edged up w-o-w: Spot lump premium edged up w-o-w by $0.015/t to $0.2000/t CFR China on 3 July.

China coke rally lifts market sentiment; Australian PHCC holds firm: China's domestic coke market strengthened on 2 July, with mainstream coke prices increasing by RMB 55/t ($8/t) following the full implementation of the ninth round of price hikes. Improved coking coal costs and higher coke prices lifted coking plant profitability, while production remained steady and inventories stayed low amid active shipments. Robust blast furnace operating rates and high pig iron output continued to support steel mills' coke demand. Market sentiment remain firm, with expectations of a potential tenth round of coke price increases, supporting a bullish near-term outlook.

Australian Premium Hard Coking Coal prices remained stable w-o-w at $244/t FOB Australia, supported by firm producer offers despite subdued spot buying. BigMint's premium hard coking coal (PHCC) index was assessed at $263/tonne (t) CNF Paradip, India, on 04 July 2026, down by $4/t w-o-w. Sufficient inventories and drop in steel prices have held back Indian mills from bidding aggressively for coking coal.

Domestic billet extends losses as weak demand, rising inventories pressure market: Chinese billet prices continued to soften during the week ended 3 July, pressured by seasonal weakness in construction demand, rising inventories, and sluggish export activity. BigMint assessed domestic billet at RMB 2,940/t ($434/t), down RMB 30/t ($4/t) from RMB 2,970/t ($439/t) a week earlier.

Rebar trading volumes improved to around 90,000 t/day, but failed to support prices as mills maintained relatively high output, resulting in rising inventories and continued pressure on domestic finished steel prices, which fell by RMB 10-20/t ($1-3/t) during the week.

Around 5% of electric arc furnace (EAF) mills reduced operating rates due to compressed margins, while weaker iron ore prices and easing raw material costs provided limited support to billet values.

Export activity also remained weak, with Chinese billet offers easing to around $455-457/t FOB, compared with $462-464/t FOB a week earlier, amid stronger regional competition, tighter European import restrictions, weaker buyer currencies, and limited overseas enquiries.

Weekly steel price trend

Domestic HRC prices decrease w-o-w: Chinese HRC prices decreased by RMB 30/t ($4/t) w-o-w to around RMB 3,100/t ($457/t) on 3 July from RMB 3,130/t ($462/t) from the previous week. Moreover, SHFE HRC futures (October 2026 contract) down by RMB 33/t ($5/t) w-o-w to RMB 3,279/t ($484/t) from RMB 3,312/t ($489/t) a week earlier. However, Chinese HRC export offers dropped by $5/t w-o-w to $510/t FOB Rizhao from the $515/t in the previous week.

China's domestic HRC market remained under pressure this week, with prices declining across most markets as sellers lowered offers to clear inventories. Although some steel mills-initiated maintenance and production cuts after prices approached production costs, overall supply and inventory levels remained elevated. Trading activity continued to be subdued, with the supply-demand imbalance persisting.

Chinese HRC export prices edged lower this week, as mills continued to reduce their offers in an effort to stimulate demand amid the seasonal slowdown during the rainy season.

Rebar prices decrease w-o-w: Rebar prices in China were down by RMB 30/t ($4/t) w-o-w to around RMB 3,180/t ($469/t) as on 3 July, compared with RMB 3,210/t ($473/t) in the previous week. Furthermore, SHFE rebar futures (October 2026 contract) also dropped by RMB 26/t ($4/t) w-o-w to RMB 3,062/t ($452/t) as on 3 July from RMB 3,088/t ($456/t) a week earlier.

Chinese rebar prices fell as the off-season reduced end-user demand and steel mill profits remained under pressure. Orders from downstream industries were lower than expected, while finished steel inventories continued to increase. Low profits and losses led some steel mills to adjust production schedules and cut output through maintenance and production reductions.

China's Shagang Steel has rolled over its long steel prices for early-July 2026 sales, reflecting a weak domestic market environment. The producer has kept rebar (16-25 mm) prices unchanged at RMB 3,400/t ($501/t), coiled rebar (8-10 mm) at RMB 3,530/t ($520/t), and wire rod (6-10 mm) at RMB 3,440/t ($507/t). Facing a sluggish domestic market, steel mill chose to roll over prices as demand remained weak and production gradually increased in June.

Outlook

China's domestic HRC market is expected to remain weak in the coming week. High temperatures, heavy rainfall, and the approaching typhoon season are likely to continue affecting outdoor construction activity. While prices in some regions have neared steelmakers' production cost levels, limiting further declines, the absence of clear demand-side support is expected to keep prices on a downward trend.