China supply tightness supports global met coal, coke prices; Indian buyers stay cautious

...

- FOB Australian PLV prices dip, but Chinese CFR values increase

- PCI may gain relevance as coking coal, coke prices remain firm

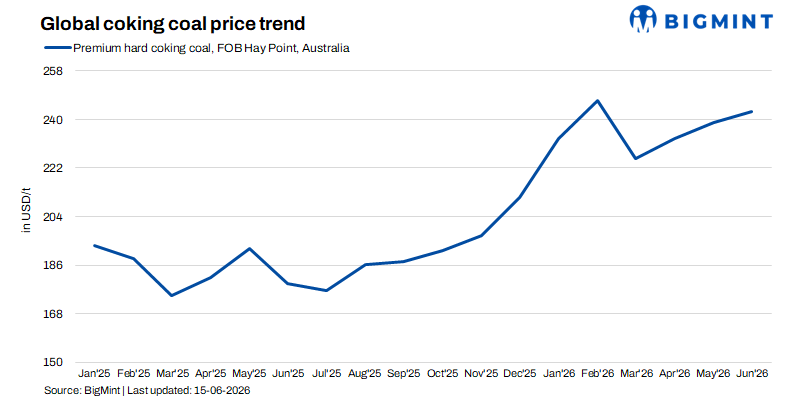

Global metallurgical coal, met coke, and PCI markets remained mixed during the week ended 12 June 2026, with China-led supply tightness supporting prices even as Indian buying stayed muted amid weak steel margins and comfortable inventories.

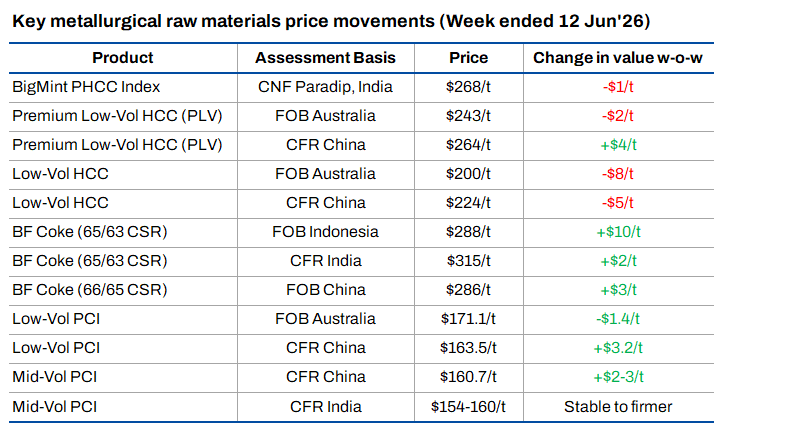

The clearest divergence was visible in premium hard coking coal. Australian PLV prices softened after a 75,000 t Peak Downs cargo for July loading was concluded at $243/t FOB Australia. The trade capped near-term FOB sentiment, particularly as several premium mid-vol cargoes remained unsold with traders.

However, delivered China prices remained firmer. PLV CFR China moved up to around $264/t, supported by tight domestic coking coal availability and sustained interest for prompt-arrival cargoes. Chinese buyers, however, remained selective. While sellers continued to indicate offers above $270/t CFR China for premium mid-vol cargoes, buyers were largely comfortable only around $260-265/t CFR levels.

The underlying bullish driver remains China's disrupted domestic supply. Safety checks in Shanxi have slowed the restart of coking coal mines after the late-May accident. This has kept domestic premium coal prices firm and supported seaborne buying interest. However, buyers are reluctant to commit aggressively to July-loading cargoes amid expectations that supply may gradually normalise and steel mills may schedule maintenance in July.

India remained largely absent from the spot market. BigMint's PHCC index was assessed at $268/t CNF Paradip on 12 June, down $1/t w-o-w, as sufficient inventories, subdued steel demand, and weak finished steel prices limited aggressive procurement. Lower Australia-India vessel freights also softened the landed cost, with Haypoint-Paradip Panamax freight assessed at $23.5/t, down $1.3/t w-o-w.

Met coke prices find strong support

Imported met coke prices strengthened on higher Indonesian FOB levels and firm Chinese demand. A 20,000 t cargo of Indonesian 65/63 CSR coke was concluded at $288/t FOB Indonesia for mid-July loading. Indonesian suppliers are now targeting higher levels for August-loading material, with indications moving closer to $295-298/t FOB.

Chinese coke prices also strengthened after mills accepted the sixth round of domestic coke price hikes of RMB 50-55/t ($ 7-8/t). Tight coking coal availability, active restocking, and low coke inventories have supported sentiment. Expectations of further hikes cannot be ruled out if coal supply disruptions persist.

In India, imported Indonesian BF-grade coke was assessed around $315/t CFR India. However, the domestic market remained relatively stable. Eastern India BF-grade coke was around INR 36,700/t ex-Jajpur, while western India prices were around INR 34,000/t ex-Gandhidham. Foundry-grade coke remained near INR 36,400/t ex-Rajkot.

PCI gains relevance as coke costs rise

PCI markets remained supported, particularly for Russian-origin material. Russian low-vol PCI was heard around $163.5/t CFR China, while mid-tier Russian PCI was indicated around $154-160/t CFR India. A 75,000 t Russian low-vol PCI cargo for August loading was reported at $176/t CFR Indonesia.

The market is increasingly being shaped by Russian material, especially into China and Southeast Asia. With coke prices rising and steel margins under pressure, mills may look to optimise PCI injection rates where technically feasible. This could lend additional support to PCI prices, especially in India and Southeast Asia.

Outlook

The near-term outlook remains cautiously firm but uneven. Met coal prices may remain supported by Chinese supply disruptions, though FOB Australia could stay capped by unsold cargoes and weak Indian demand. Coke prices are likely to remain elevated due to higher coking coal costs, firm Chinese sentiment and rising Indonesian FOB offers.

Indian domestic coke may stay largely stable in the immediate term due to comfortable availability and subdued steel demand, but higher landed costs, a weak rupee and firm tender prices should provide a strong floor.

PCI could emerge as the relative outperformer if coke prices continue rising and mills seek cost optimisation. The key factors to watch are the pace of Shanxi mine restarts, Chinese steel mill maintenance in July, Indian steel demand during the monsoon, and further movement in Indonesian coke offers.