China's steel industry remains under pressure in Jan-Feb'26 amid uneven demand recovery

...

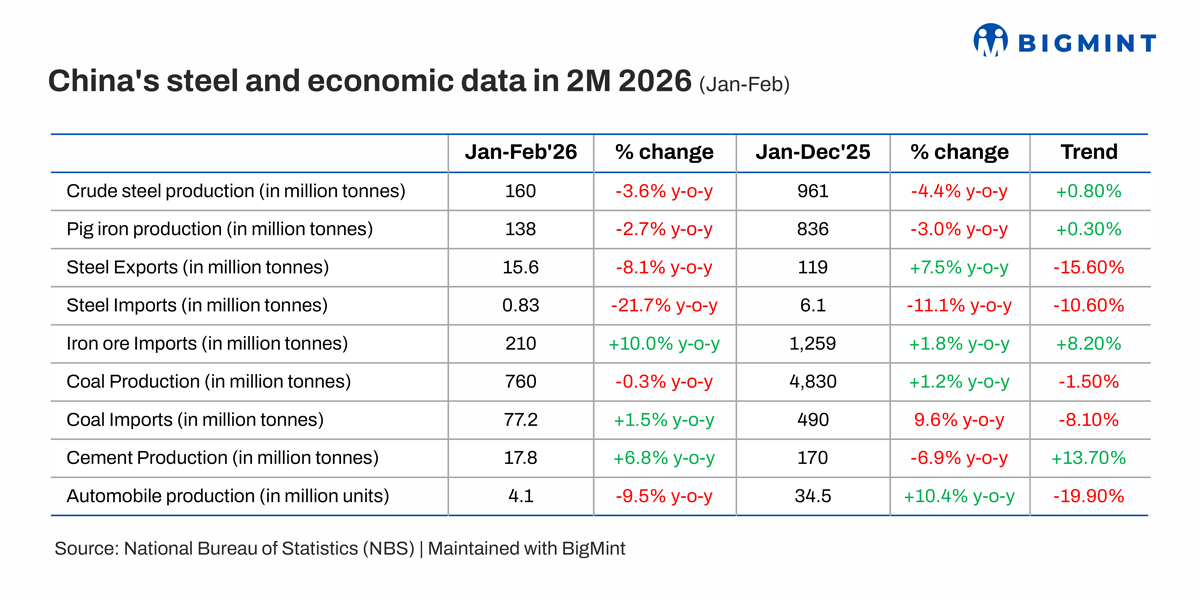

- Crude steel output declines 4% y-o-y as property slump persists

- Steel exports fall by 8% on tighter regulatory oversight, trade barriers

- Manufacturing emits mixed cues, infra investment recovers sharply

Morning Brief: China's steel industry remained under pressure and cautious in January-February 2026, as structural challenges, particularly in the real estate market, continued despite some recovery in infrastructure and manufacturing.

Highlights of China's steel industry performance

Crude steel output declines amid cautious production sentiment: China's crude steel output fell, driven by continued weakness in downstream demand, which dampened production enthusiasm and prompted mills to keep inventories lean.

Steel exports retreat amid new licensing system: China's steel exports slowed down in January-February, as the reintroduction of export licensing requirements from January 2026 increased compliance costs and reduced the competitiveness of Chinese steel in international markets. A significant portion of earlier export growth had been driven by non-VAT trade, which has now been curtailed due to stricter regulatory oversight.

Steel exports retreat amid new licensing system: China's steel exports slowed down in January-February, as the reintroduction of export licensing requirements from January 2026 increased compliance costs and reduced the competitiveness of Chinese steel in international markets. A significant portion of earlier export growth had been driven by non-VAT trade, which has now been curtailed due to stricter regulatory oversight.

Moreover, frontloading in December, before the new system came into effect, led to reduced buying urgency during early 2026. At the same time, rising global protectionism, evidenced by multiple anti-dumping investigations, continued to limit market access.

Iron imports rise on higher supply: In contrast to declining steel production, China's iron ore imports surged. This increase was largely driven by stronger shipments from key suppliers such as Australia (+13% at 136 million tonnes) and Brazil (+14% at around 48 mnt), supported by improved weather conditions and stable mining operations. Additionally, steady blast furnace utilisation contributed to sustained raw material consumption.

Coal production falls marginally, imports inch up: Coal production declined marginally by 0.3% y-o-y. The slight dip was largely due to slower operations during the Lunar New Year holiday, when output hit a two-year low, as per Mysteel Global.

According to the Centre for Research on Energy and Clean Air, China's total power generation was estimated to have increased by 9.9% y-o-y, with coal-fired output up 4.4%. Moreover, geopolitical uncertainties and supply concerns arising from Indonesian production curbs are likely to have incentivised production.

Meanwhile, coal imports rose modestly, despite a 5% y-o-y cut in the yearly target set by the China Coal Transportation and Distribution Association (CCTD). The increase was supported by competitive pricing of imports in January and steady metallurgical coal demand.

Automotive sector loses momentum: Both auto production and sales both declined during January-February. This weakness could largely be attributed to seasonal factors, including the timing and extended duration of the Lunar New Year holidays, as well as policy changes such as the expiration of tax incentives for new energy vehicles (NEVs). Additionally, some demand had been front-loaded into late 2025.

However, exports remained a bright spot, rising sharply by over 48% y-o-y amid growing global competitiveness and robust demand.

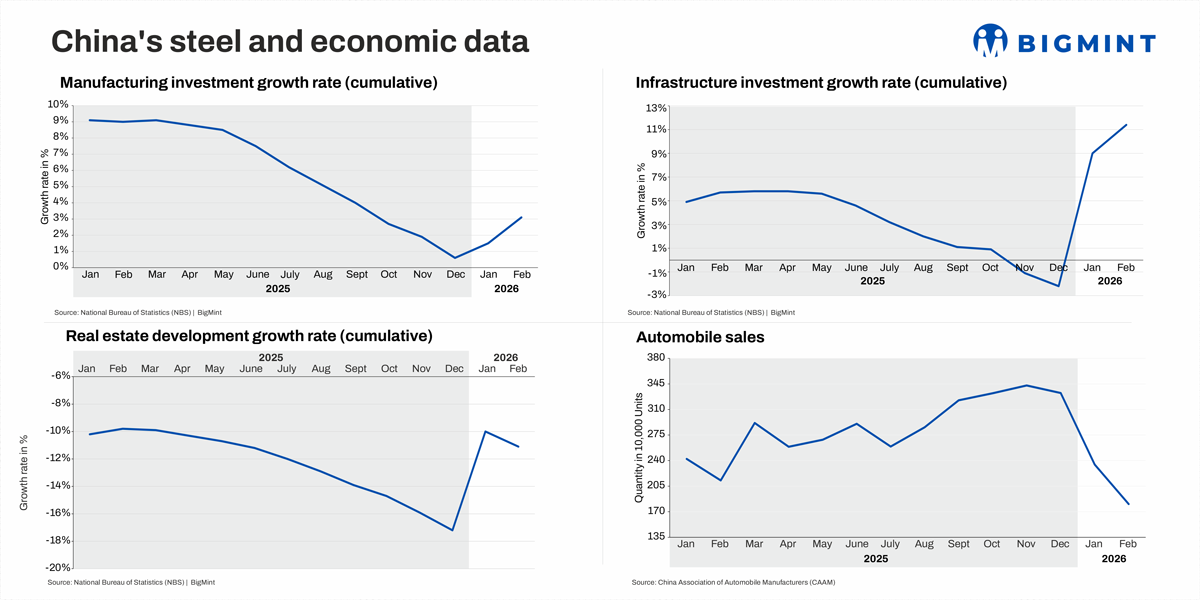

Infrastructure investment rebounds, real estate development remains slow: Overall, the construction steel sector faced mixed demand signals in January-February. Infrastructure investment rebounded strongly in a sharp turnaround from the contraction observed during December. The recovery was driven by policy support and fiscal intervention. Financing tools introduced in late 2025 enabled banks to channel funds into priority projects, alongside accelerated public spending aimed at offsetting weak private sector demand.

However, real estate development growth continued to slide though at a slower pace. Sales by floor area declined 13.5%, reflecting weak buyer sentiment and limited developer activity. The downturn was also reflected in new housing prices falling 3.2% y-o-y in February, which further eroded household confidence and discouraged spending.

Manufacturing investment growth recovers modestly: China's manufacturing investment growth recovered modestly, pointing to uneven momentum. Many manufacturers kept operations slow ahead of the Lunar New Year, while persistently soft consumer demand continued to weigh on production. However, the inflow of new export orders strengthened, leading to the S&P Global China manufacturing PMI rising to its highest since December 2020, at 52.1 points in February.

Outlook

With the onset of spring in March, the outlook for China's steel sector remains optimistic, with demand and output growing as downstream industries ramp up operations after the holiday lull. Higher investment growth in manufacturing and infrastructure bodes well for steel demand, but the continued downturn in the property segment may limit production momentum.

Meanwhile, exports will continue to play a critical role in absorbing surplus production, but rising trade frictions and logistical disruptions due to the US-Iran conflict could limit growth in March, as the Middle East receives around 20% of China's steel exports.