China: Met coke market downturn to persist in Jan'26 on weak fundamentals

...

- Weak demand persists due to low BF utilisation, high coke inventories

- Further price reductions expected as oversupply continues into Jan'26

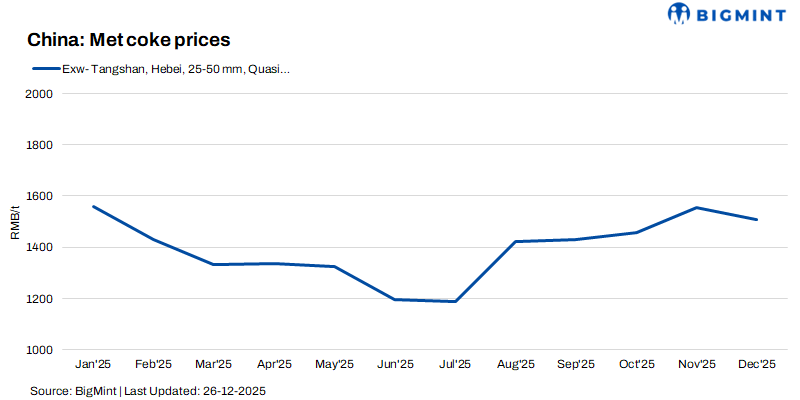

Mysteel Global: China's metallurgical coke market remained under downward pressure in December, and the weak fundamentals are expected to extend into January, as loose supply-demand condition persists and winter restocking provides limited support, according to Mysteel's latest report.

As of 22 December, Chinese steelmakers had pressed their coke suppliers to accept cumulative price cuts of RMB 150-165/tonne ($21.3-23.5/t) across three consecutive negotiations for all metallurgical coke products.

"Weak demand has been the main driver behind the continuous declines in met coke prices throughout December," a ferrous analyst in North China's Shanxi province said.

Chinese blast-furnace (BF) steelmakers' appetite for raw materials continued to weaken in December, as sluggish steel consumption forced mills to persistently scale back operations.

According to Mysteel's survey of China's 247 BF mills nationwide, their average daily hot metal output during December 12-18 fell by 2.5% or 57,500 t/day from early December to 2.27 million tonnes (mnt)/d, the lowest level in about 11 months.

Looking ahead, the Shanxi-based analyst sees little chance of a meaningful rebound in coke demand next month, citing BF mills' ample coke stocks and cautious sentiment in the steel market following the implementation of export licensing for 300 steel products starting 1 January.

As many market participants are concerned about potential export disruptions stemming from the policy, "Chinese steel prices may remain weak in January, prompting further cuts in steelmakers' hot metal output and, in turn, further dampening demand for coke," the analyst said. He also forecast that average daily hot metal output among the 247 BF mills would fall below 2.25 mnt/d in January.

While mills may accelerate raw material replenishment next month to avoid potential logistical disruptions caused by heavy snowfall and the approaching Chinese New Year holiday in February, the analyst noted that mills' current ample coke inventories had curbed their buying interest and delayed winter restocking.

As of 18 December, combined coke inventories held by the 247 BF mills reached 6.34 mnt. Although the volume edged down by 0.2% w-o-w, the surveyed mills' reduced hot metal output slowed coke consumption, leaving inventories sufficient for 11.7 days of use. This marked the highest inventory level since late May, according to Mysteel's data.

Given the weak demand outlook, the analyst predicted China's coke prices to continue trending downward in January, with a fourth round of price cuts potentially on the horizon.

Note: This article has been written in accordance with a content exchange agreement between Mysteel Global and BigMint.