China: Iron ore prices to slip further in Jul'26 amid softening domestic steel demand

...

- Strong June shipments to lift July port inventories

- Freight rates plunge sharply as Middle East tensions ease

Mysteel Global: Imported iron ore prices in China are set to continue their retreat in July, weighed down by softening domestic steel demand amid the seasonal summer lull and sustained inflows of ore as strong overseas shipments begin arriving at Chinese ports, Mysteel predicts in its latest monthly report on the commodity. Moreover, the downward pressure is expected to intensify as falling oil prices drag freight rates lower, further eroding cost support, the report adds.

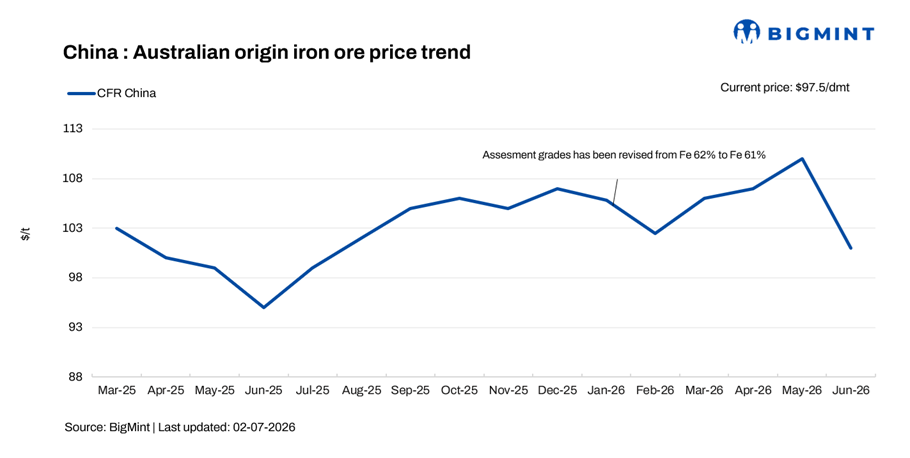

In June, Mysteel SEADEX 62% Australian Fines averaged $102/dmt CFR Qingdao, down $8.2/dmt from May's average of $110.2/dmt and marking the lowest monthly average since September last year.

Iron ore prices faced headwinds from multiple quarters during the past month, the report notes. On the macroeconomic front, rising expectations for US Fed rate hikes, combined with a sharp downturn retail sales, fixed-asset investment, and property data in China, weighed broadly on commodity markets.

At the sectoral level, domestic steel prices weakened as demand entered the usual summer off-season, while steelmakers grappled with elevated production costs amid firm fuel prices and rising coking coal and coke costs. As a result, a growing number of steel mills were pushed into the red, which curbed their appetite for ore purchases and in turn, impacted prices.

Adding to the pressure, seaborne freight rates for iron ore shipments tumbled sharply as signs that Middle East tensions were easing sent oil prices sliding, further depressing ore prices. For example, the daily freight rate for Capesize vessels on the key route from Australia's Hedland port to eastern China's Qingdao port had fallen to $10.3/t on June 30, down by $5.93/t or 36.5% from the previous month, Mysteel's tracking showed.

Looking ahead to July, China's iron ore market will continue to face expanding supply and softening demand, resulting in more downside room for prices, the report predicts.

On the supply side, while shipments from Australian miners tend to taper off seasonally in July, those from Brazil are expected to remain robust. More importantly, the strong overseas shipments that sailed in June are set to arrive at Chinese ports over the coming month, steadily adding to available stocks.

By 25 June, imported iron ore inventories stockpiled at the 47 major Chinese ports tracked by Mysteel had risen by 2.5% on month to reach 175.4 million tonnes. The tonnage is projected to increase to approximately 180 million tonnes by the end of July, the report forecasts.

In terms of demand, domestic steelmakers are expected to scale back hot metal production this month, with their keenness for production being cooled by shrinking profit margins on steel sales and an anticipated further decline in steel consumption during the summer months.

On 25 June, only about 51% of the 247 blast-furnace steel mills under Mysteel's monitoring -- or 126 steelmakers -- said they were making profits on steel sales, down by 11 percentage points from a month earlier.

In addition, the report warns that the likelihood of the Federal Reserve lifting interest rates soon will continue to hang over commodity markets, while freight rates could slide further as the peak shipping season for Australian ore winds down and oil prices lose more ground.

In the worst-case scenario, in July iron ore prices could fall to their lowest level in several years, the report suggests. By 30 June, the lowest Mysteel SEADEX 62% Australian Fines in recent memory was recorded on 23 September 2024 at $89.45/t, according to Mysteel assessment.

Note: This article has been written in accordance with a content exchange agreement between Mysteel Global and BigMint.