Brazil's aggressive cotton exports reshape India's import and price dynamics

...

- Heavy early-season Brazilian shipments intensify competition for Indian cotton in Asia

- Lower Brazil output later in the season may support Indian prices post-arrivals

Brazils cotton exports have risen sharply in the early part of the 2025/26 marketing year, creating clear implications for the Indian cotton market. During August-December 2025, Brazil exported 1.405 million tonnes of cotton, up 15.7% year-on-year and the highest-ever shipment volume for the first five months of a season. December alone recorded exports of 452,500 tonnes, showing a strong 28.2% annual increase as Brazil pushed large volumes into the global market amid weak prices.

From Indias point of view, Brazil has emerged as a major source of imported cotton this season. India imported around 184,400 tonnes of Brazilian cotton during August-December 2025, making it the third-largest buyer after China and Bangladesh. Indian spinning millers have increased reliance on Brazilian cotton due to its consistent quality, lower contamination, and availability of BCI-licensed fibre, which is important for export-oriented yarn and textile orders. This has made Brazilian cotton a key balancing factor alongside domestic supplies.

At the same time, Brazil's strong export presence has intensified competition for Indian cotton in key Asian markets. Higher Brazilian shipments to China and Bangladesh have limited India's export opportunities, especially when Indian cotton prices remain relatively firm during the peak arrival period. As a result, Indian exporters are facing pricing pressure, keeping domestic cotton values largely range-bound despite steady mill demand.

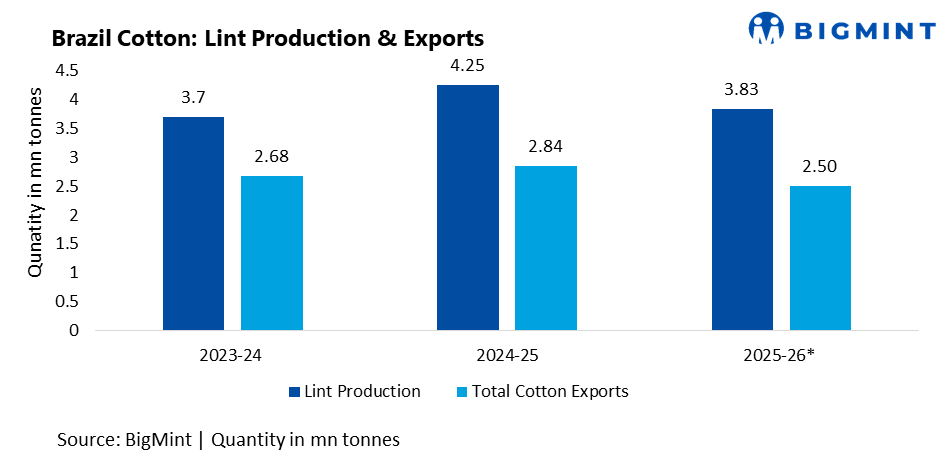

On the supply side, Brazil's production outlook has weakened. The 2025/26 planted area has been revised down by about 5% to 2.05 million hectares, while cotton lint output is now estimated at 3.83 million tonnes, nearly 10% lower year-on-year. Average yields are also expected to fall by around 4.7%. This indicates that Brazil's export strength is largely front-loaded, and shipment momentum could slow in the second half of the marketing year.

Price trends support this view. Brazil's domestic cotton prices declined in December, while global futures also moved lower on a monthly basis. On a year-on-year basis, both domestic and international prices are down by around 6%, suggesting that Brazil is prioritising volume-led exports over price realisation. For India, this keeps imported cotton competitive in the near term and limits any sharp upside in domestic prices during the arrival season.

Looking ahead, lower Brazilian production combined with heavy early-season exports could tighten global cotton availability by mid-2026. For India, this may offer gradual price support once domestic arrivals slow and imported cotton becomes costlier. Ginners could see improved demand later in the season, while spinning millers are likely to remain cautious, continuing a hand-to-mouth buying strategy while balancing domestic cotton with selective imports.