BigMint's steel index drops on weak construction sentiment but policy support provides stability

...

- Rebar prices decline across regions on increased inventory levels

- HRC market remains relatively stable amid policy-induced support

- Domestic prices will receive support from AD probe into HRC from 3 countries

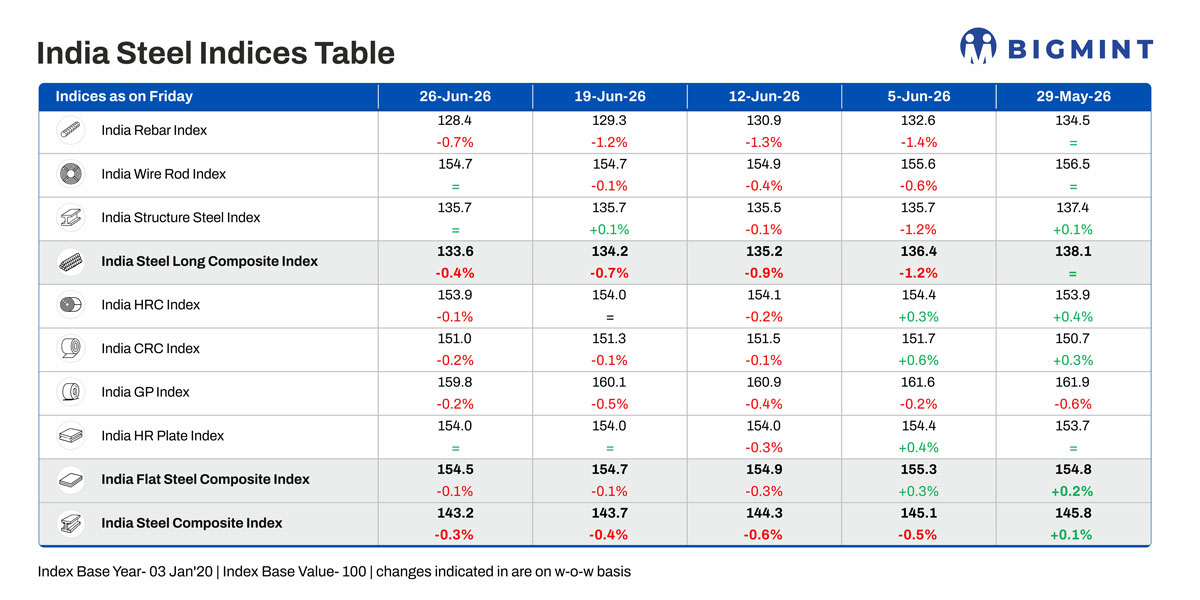

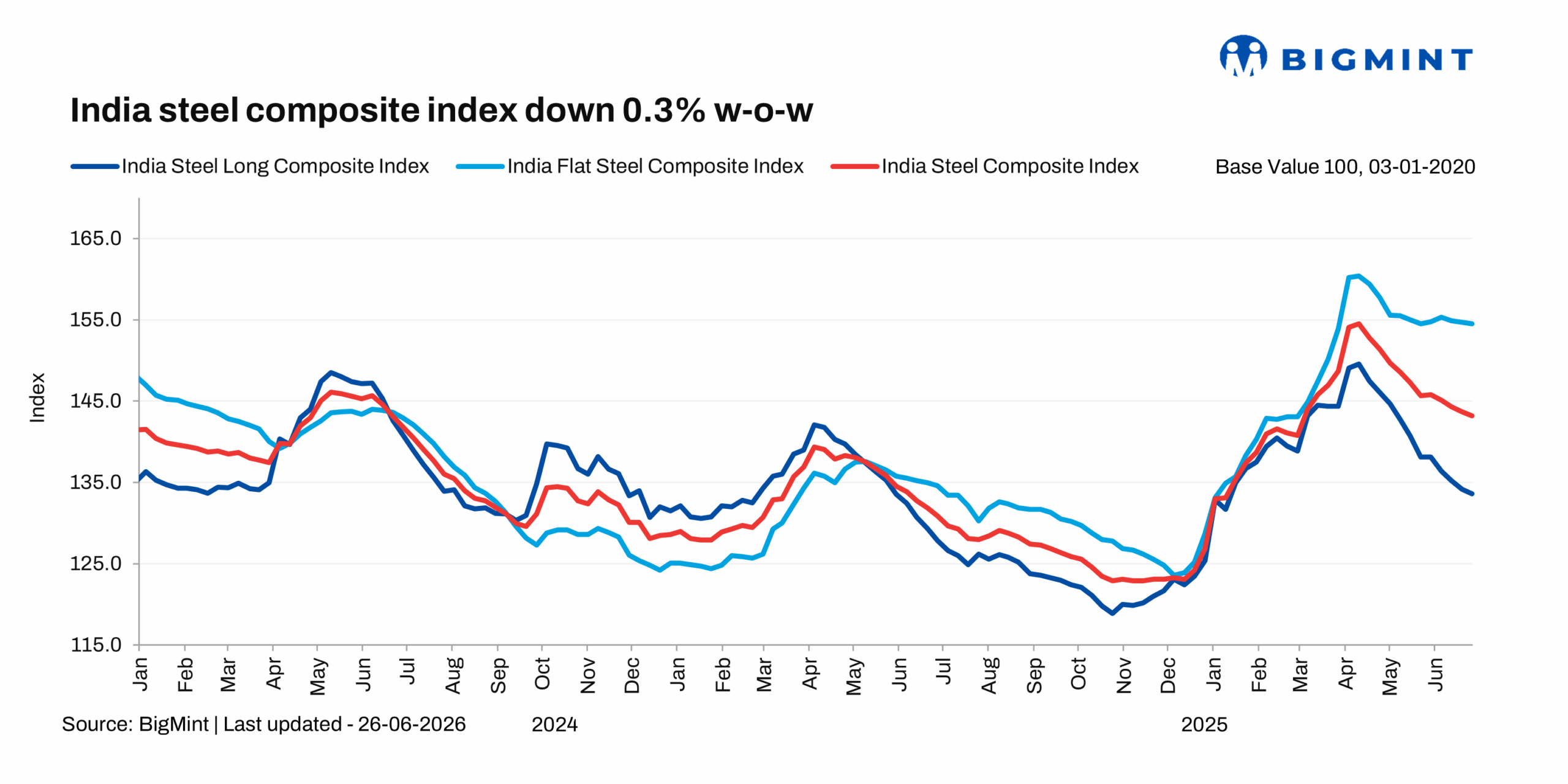

Morning Brief: Domestic steel prices softened further in the week ended 29 June 2026, with BigMint's steel composite index, a barometer of the domestic market, edging down by 0.3% w-o-w. Steel prices continue to remain under pressure as India enters the seasonally weak monsoon period. Trade sentiment remains downcast and the gradual softening in key raw material prices further weighed on steel prices.

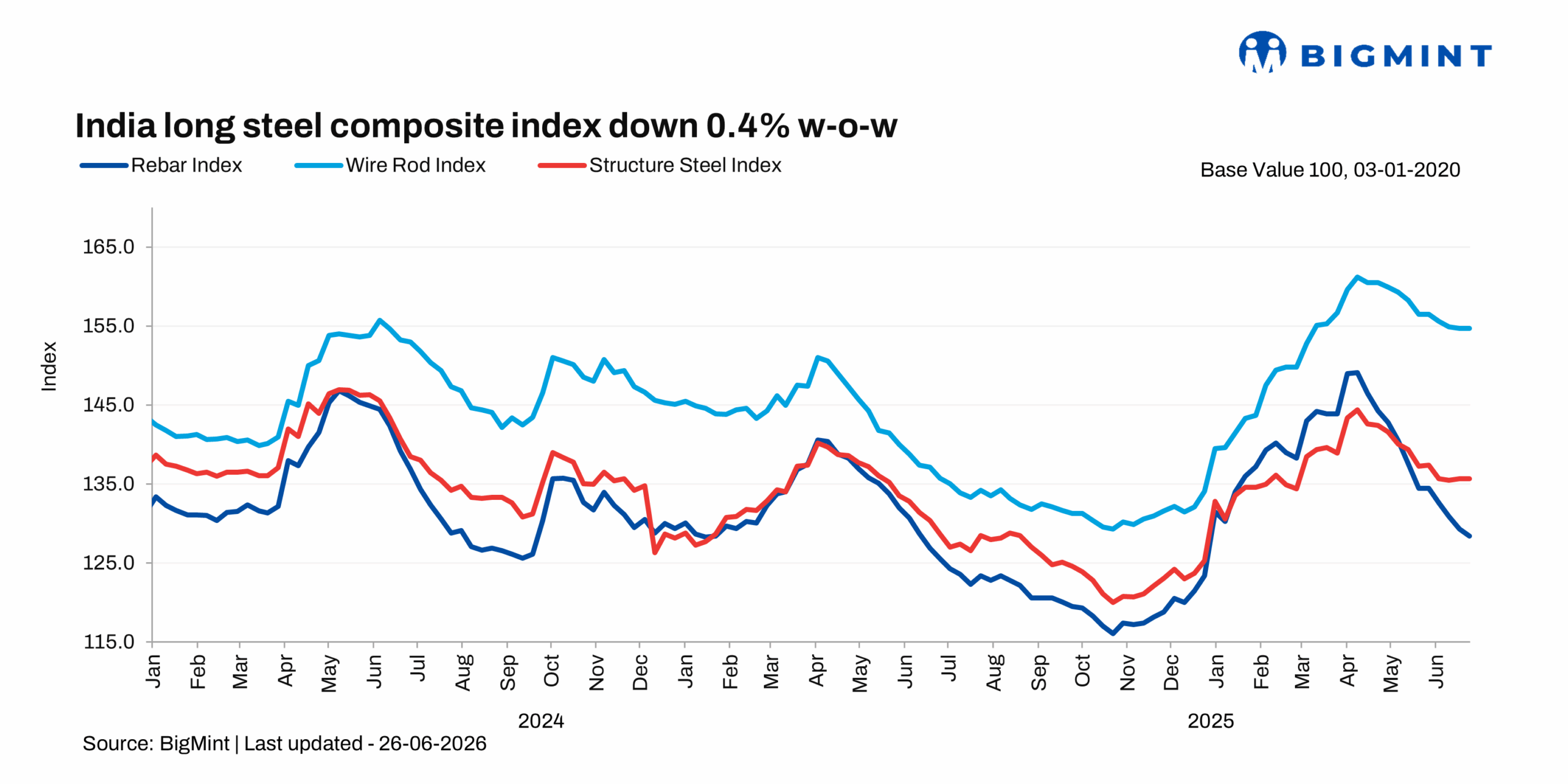

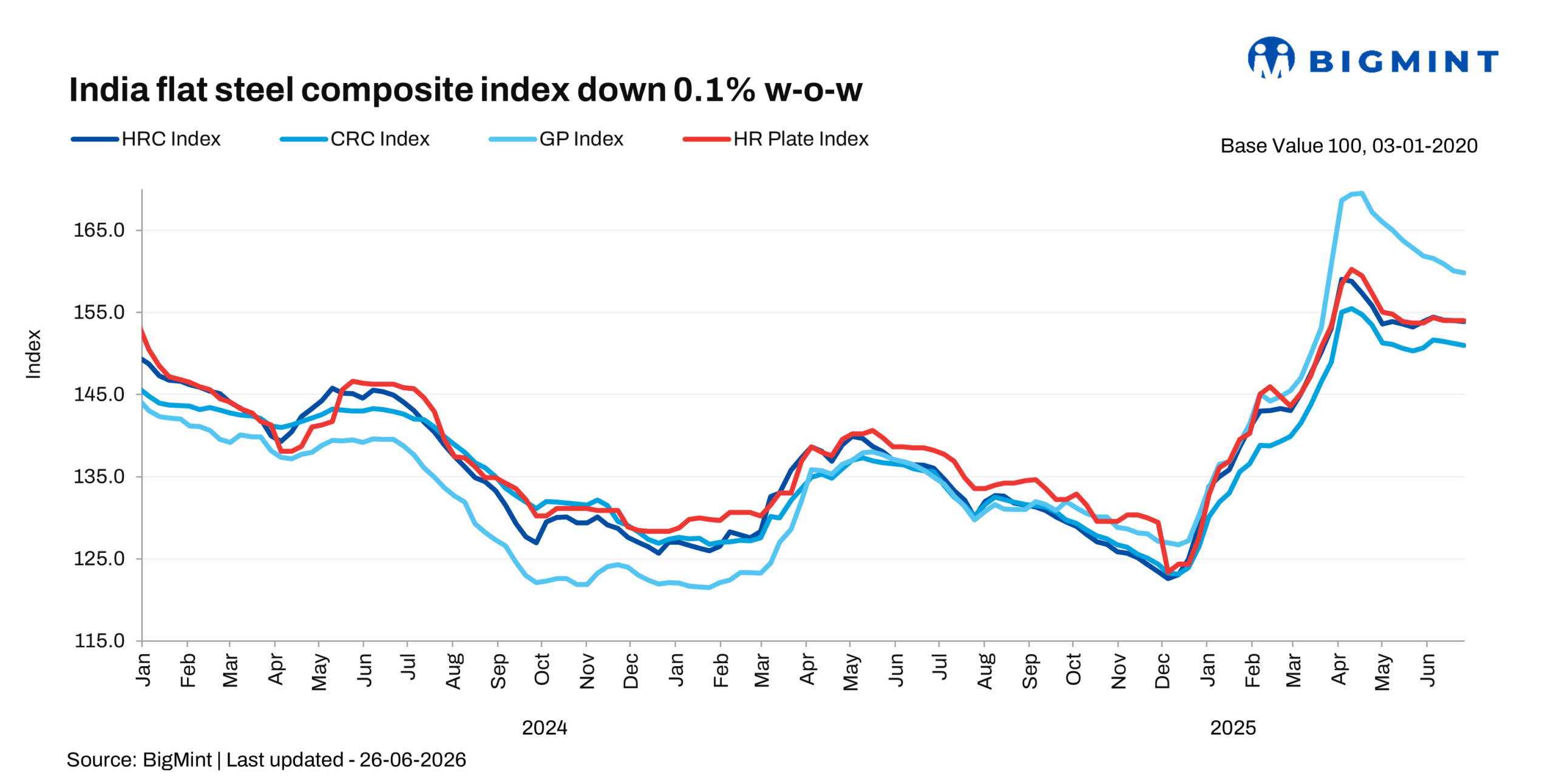

The composite index dropped 1.8 percentage points in June, while the HRC sub-index declined just 0.3 percentage points. In comparison, the rebar index dropped over 3.5 percentage points during the month highlighting the fact that pressure on longs prices are severe while flat steel continues to remain largely stable. This is due to weak construction sentiment, higher imports of bulk HRCs during April and May, and some exports recorded by the domestic mills which propped up HRC market sentiment.

With India launching an antidumping investigation on hot-rolled flat product imports from China, Japan and Russia, and also a separate AD probe into electrical steel imports, policy-led support is expected to boost the domestic HRC market for the time being. However, longs prices lack any such immediate prop and may continue to decline faster.

Highlights of price movements

Rebar prices decline: BigMint's benchmark assessment (bi-weekly) for rebar (IS 1786 Fe 550D, 1232 mm, BF route) was assessed at INR 51,000/t as of 26 June, down INR 700/t from INR 51,700/t recorded on 19 June. Prices are ex-Mumbai for the distributor-to-dealer segment and exclude 18% GST.

Prices reached their lowest level in over six months, reflecting weak buying interest and high inventory across the supply chain. Market sentiment remained cautious as distributors continued to hold inventories exceeding 35-40 days, compared to around 30 days in the previous week, while buyers restricted purchases to immediate requirements amid subdued construction activity.

In June, Mumbai BF-route rebar prices declined by INR 4,800/t month-to-date on monsoon-induced slowdown in construction activity. Chennai and Bengaluru witnessed subdued construction activity due to heavy rainfall. However, supply problems at a major BF-route steel producer limited material availability, resulting in slower pace of price correction compared with other regions.

In the project segment, buyers leveraged sluggish demand to negotiate lower prices. Limited execution and slow fund flows further restrained procurement activity.

IF-route rebar prices fell by INR 100-800/t w-o-w across markets last week. Trade volumes were limited across regions. Inventory levels were reported at around 10-15 days. The BF-IF rebar price spread in Mumbai remained stable w-o-w at INR 6,000/t ($63/t). The differential, which was close to INR 10,000/t ($106/t) in the beginning of June, has compressed sharply.

HRC domestic market remains stable: BigMint's bi-weekly assessment for HRC (IS 2062, Gr E250, 2.58 mm/CTL) remained stable at INR 58,200/t ($611/t) as of 26 June. Meanwhile, the benchmark assessment for CRC (IS 513, Gr O, 0.9 mm/CTL) also remained unchanged at INR 65,200/t. These assessments are ex-Mumbai for the distributor-to-dealer segment and exclude 18% GST.

HRC trade prices continued to remain largely stable while buyers focused on need-based deals. India's private sector growth weakened in June while export orders also showed weak growth. The HSBC composite PMI dropped in June compared to May. However, manufacturing demand remained moderate-to-stable. Market sources said the onset of monsoons will weigh on trade activity. Market sentiment continued to remain cautious, with buyers avoiding inventory build-up and focusing primarily on fulfilling immediate needs.

HRC export offers edge down: HRC export offers to the EU and Southeast Asia declined by around $5/t w-o-w. In the EU, buyers remained cautious amid uncertainty over country-specific quota allocations under the EU's revised steel trade defence framework. On the other hand, lower offers to the Middle East and Vietnam was due to subdued buying interest and increased competitive pressure.

Antidumping probes: The Directorate General of Trade Remedies (DGTR) under India's Ministry of Commerce has opened an anti-dumping (AD) investigation into hot-rolled flat steel products originating in or exported from China, Japan and Russia. The investigation involves hot-rolled flat products of alloy or non-alloy steel, not clad, plated or coated, of a thickness up to 25 mm and width up to 2100 mm.

The DGTR has also launched an anti-dumping investigation into imports of cold-rolled grain-oriented (CRGO) electrical steel and amorphous metal from China, Japan, South Korea, and Russia. The investigation follows a petition by JSW JFE Electrical Steel Nashik, which alleged that dumped imports from the four countries have caused material injury to the domestic industry.

Under the safeguard mechanism domestic prices continue to remain well below landed imports, as per BigMint calculation. The possibility of clampdown of AD duty on HRC will provide support to domestic HRC prices, BigMint understands. Industry sources told BigMint that because of high tariffs in major importing geographies such as the EU and the US, and because of the low 11.5% safeguard duty in India, major suppliers are channelling material towards India at a time of strong consumption in the country compared with other major nations. This is the rationale behind the AD probes.

Data show that India's bulk HRC import volumes have dropped sharply in June from May levels. HRC imports dropped 35% in FY'26.

Outlook

Seasonal disruptions, labour shortages and input cost volatility is expected to weigh on commercial construction activity as the outlook during monsoon remains cautiously optimistic. Rebar prices are expected to remain under pressure in the coming couple of months due to elevated inventories. Coking coal prices remain firm, especially the prime grades, while iron ore remains stable.

HRC prices, however, may remain relatively stable on robust manufacturing demand and policy support, plus differential with import prices. But uncertainty prevailing in key export markets such as the EU will adversely impact export prospects. The domestic market is awaiting list price announcements of the major mills for July.